Fannie Mae's Economic Summary for March reports an improvement in financial market conditions and reduced concerns about an imminent risk of recession but did not materially change the company's outlook since its February forecast. Its economists still expect the economy to grow by 2.0 percent this year and say that the full impact of the earlier rise in the dollar and the plunge in oil prices have not fully passed through the system. Weakness in net exports and nonresidential fixed investments in equipment and structures related to energy exploration and development will continue to weigh on growth.

Job growth continues strong and is more than sufficient to keep up with growth in the working age population. Average hourly earnings and the average work week both fell after encouraging improvements in January.

The report says the Fed can afford to be patient when it comes to the next rate hike. In addition to the strong job numbers, the core PCE deflation rose 1.7 percent year-over-year, the biggest gain since July 2014. Fannie Mae forecasts it will stay below the Fed's target of 2.0 percent for some time and that the Federal Open Market Committee will raise the fed fund rate by 25 basis points in both June and December.

As to housing, Fannie Mae says activity started out the year on a soft note. Existing home sales in January posted only a small gain in January after a strong surge in December (and this week's report from the National Association of Realtors says February saw a sharp decline. New home sales also were down significantly in January. Housing starts, both single and multi-family pulled back but still the economists expect real residential investment this year to contribute around the same 0.3 percentage points to growth that it did in 2015.

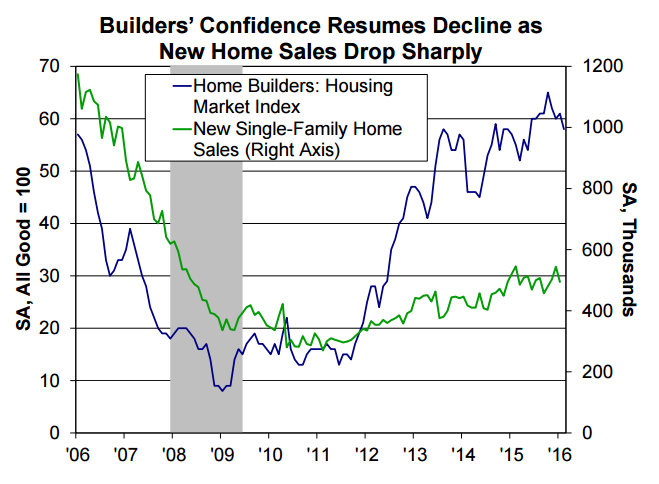

The National Association of Home Builders' (NAHB) Housing Market Index (HMI) a measure of builder confidence in the new home market, slipped to its lowest reading in February since May 2015 (and remained there in March). Pending home sales experienced the fourth decline in the last six months including in both January and February.

Those pesky existing home inventories continued to be just that, falling on a year over year basis for the eighth straight month in January. The inventory - based on both available homes and the rate of sales but not seasonally adjusted - remains at 4.0 months, down from 4.5 months a year earlier. This under-supply continues to put upward pressure on home sales and all three major home price indices - S&P Case-Shiller, FHFA, and CoreLogic - showed annual increases nationally of between 5.0 and 6.0 percent in December.

Prices did weaken in some states, both Louisiana and Mississippi posted annual declines, and price increases slowed in two of the big energy states, Texas and Oklahoma and in Midland, Texas, the metro with the highest concentration of oil employment in the country, the gains dropped to less than half the rate of a year earlier.

New home inventories have improved over the last year but still remain below traditional levels. Builders continue to report labor shortages as well as few available building lots. Seventy-one percent of builders surveyed by NAHB reported that cost and availability of labor was a problem and 76 percent expected that to continue in 2016 while 58 percent said a shortage of lots was an issue last year and about the same percentage expected it to remain so this year. The economists said they do expect single family home starts to rise this year but those labor and land shortages will remain a constraint and present a downside risk to that forecast.

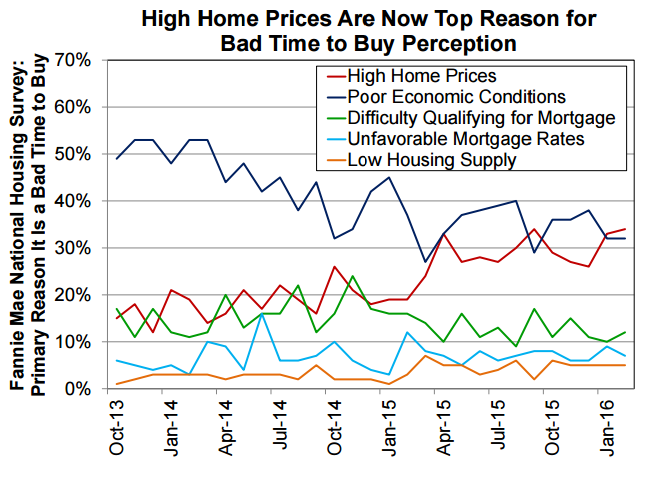

The economists forecast that home price appreciation will continue to outpace income growth and further erode home affordability, especially for first time buyers. Repeat buyers however could realize higher capital gains from selling their homes and use that to enable a new purchase and those buyers are less likely to be deterred by rising prices. Fannie Mae's Home Purchase Sentiment Index which distills consumer responses to key questions from its National Housing Survey into a single number representing housing attitudes toward the upcoming 12 months, ticked up in February. Consumers who think it is a bad time to buy generally indicate that high home prices are a factor in that opinion.

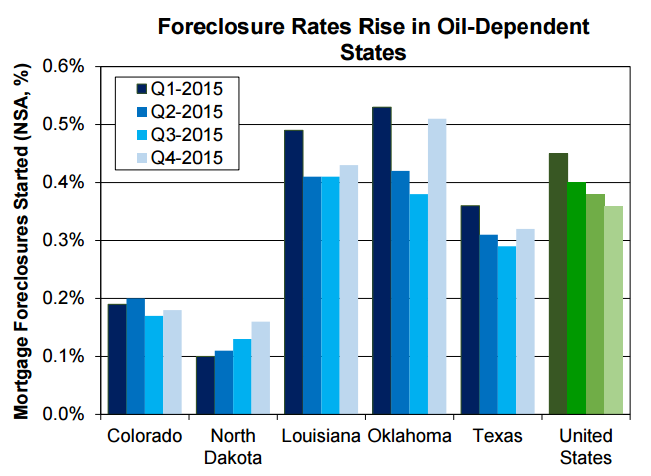

That price appreciation coupled with the improved job's picture has helped improve mortgage performance. The foreclosure start's rate declined to 0.36 percent in the fourth quarter of 2015. Twelve states did post an increase in foreclosure starts and five of these have oil dependent economies.

Fannie Mae says that the continuing low interest rates should help support an ongoing increase in home sales this year. The company's forecast for mortgages rates has been revised down by about 10 basis points for the year to an average of 3.7 percent during the fourth quarter of 2016. Other forecasts are unchanged with housing starts expected to rise 10.9 percent and home sales by 3.3 percent. Purchase mortgage originations should rise about 4.0 percent to $951 billion and refinance originations have been upgraded by $50 billion to $609 billion. The refinancing share of originations will be down an estimated 7.0 percentage points to 39 percent.