Most folks would scoff at us if we said mortgages gave a strong performance last week. It doesn't seem possible when the Fannie Mae 4.0 MBS coupon dropped 46/32 in price.

Well scoff away because here we are telling you that MBS buyers we're "waving 'em in" into lower price levels last week. That means we saw bargain buying, a push-back against quarter-end profit taking (position squaring) as MBS became less callable. That buying did little to stop steep price declines though. Rate sheets shed over 100bps when all was said and done. You can blame benchmark Treasuries for that, they led the way lower as risk-assets rallied. The 10-yr note yield jumped nearly 32bps over the course of the week.

WHY?

A multitude of factors including but not limited to: rally exhaustion (overbought technicals in bonds. oversold techs in stocks), Greece avoiding default (for now), the end of the Fed's QEII bond buying program, the end of the second quarter, and "not as bad as expected" June econ data.

NOW WHAT?

Well with Greece seemingly saved for the summer and the Fed out of the market, new economic data, the debt-ceiling debate, and trading technicals will take the lead in providing directional guidance for interest rates. Economists have already cut forecasts considerably for 2011, but did they over-do the downgrades? Leaving too much room for upside surprises. This is a concern of ours. We still think the economic recovery is lacking core ingredients like wage-growth, consist payroll expansion over 200,00 jobs a month, and a bottom in housing, but the market is used to that by now. That's where trading technicals come into play....

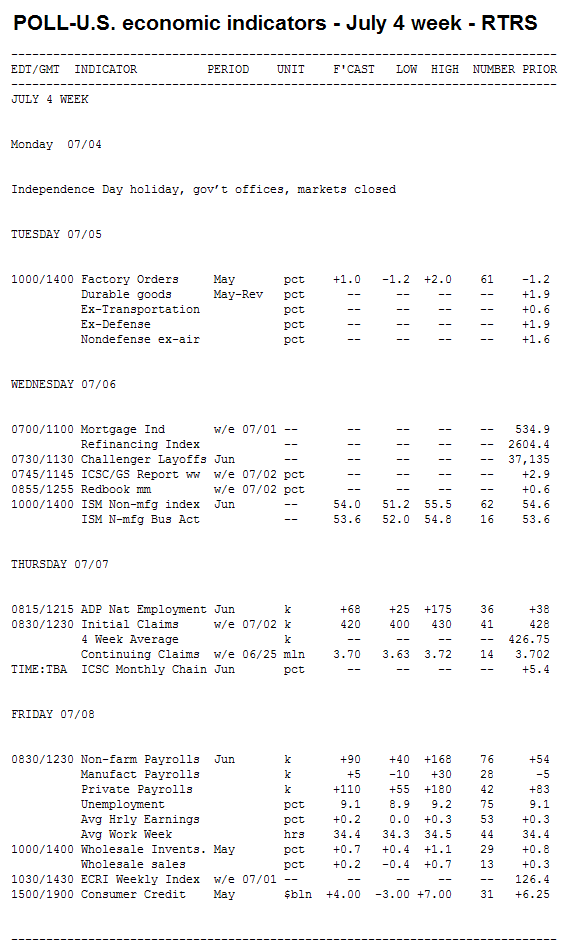

The main event in the week ahead will be the June "Employment Situation Report”. Economists surveyed by Reuters believe 88,000 jobs were added to non-farm payrolls in June. The unemployment rate is expected to have risen from 8.9% to 9.1%. While anything below 200,000 new jobs a month is a drag on the economy, as evidenced by the expected uptick in the UE rate, a headline payrolls number that beats economist expectations would likely have a negative impact on interest rates.

A bit of caution has already returned to the market though. After five straight sessions of stock gains in the final days of the second-quarter led to the best week over week rally in nearly two years, Treasuries are slightly firmer Monday morning and equities are mixed.

The 10-year Treasury yield is 3bps firmer at 3.153% and the two-year yield is 2.4bps lower at 0.450% while the Fannie Mae 4.0 MBS coupon is back over par, +8/32 at 100-01. The curve is steeper from the belly on out. The 5s/30s spread is 3bps wider at 263bps.

While Greece seems to have avoided default for now, global investors are already questioning how successful the initiatives to save

Greece from default will be. One question is whether a voluntary

rollover of Greek debt would be considered a default; if so, the

European Central Bank might not be obliged to buy it.

Elsewhere,

Moody's Investors Service said it reviewed China's local government debt

and found the figures were much larger than previously anticipated. The

rating agency said the report could lead to a ratings cut.

"Moody's

notes that non-performing loans could be higher than anticipated," said

economists at BMO Capital Markets. "Even if Moody's worst case scenario

were to unfold, it's important to remember China holds $3 trillion in

FX reserves which could be tapped to bail out the banking system."

S&P 500 futures are -2.50 at 1332.25 while the Dow is just 4 points higher at 12,516. Commodity

prices are generally higher: light crude oil rose 0.74% overnight to

$95.65, while gold prices jumped 1.42% to $1,503.60.

Key Events This Week:

Tuesday:

No significant events.

Wednesday:

10:00 - The ISM Non-Manufacturing Index is

anticipated to report growth for the 19th consecutive month in June.

The consensus forecast expects the index to come in four points above

the break-even level, at 54, representing some modest slowdown from

May's 54 level, but a better pace than April's 52.8.

New orders,

the key forward-looking component, increased four points to 56.8 in

May, and employment ticked up to 54, so the fundamentals of this report

are looking good. In addition, last week's ISM manufacturing report

climbed unexpectedly by two points to 55.3, adding some hope that this

report - which looks at the services, construction, and financial

sectors - will also post an upside surprise.

"One source of

support for the ISM non-manufacturing for June is some degree of

optimism over the commodities price situation," said forecasters at

Janney Capital Markets. "Last month, survey respondents noted that not a

single of the two or so dozen commodities which serve as common inputs

declined in price, a trend which should change in June. Even though

economic conditions are clearly pointing towards a patch of weaker

aggregate demand, strong levels of corporate investment suggest that the

services sector could avoid an out-right contraction, though slower

expansion is a near certainty."

Economists at Nomura Global Economics are more pessimistic, anticipating a 51.2 score.

"We

expect weakness to emerge in this report as there have been hints of

demand destruction because of the softening in weekly retail sales and

lower consumer confidence," they said. "As always, we will pay close

attention to the employment index, which could be a timely indicator of

service sector hiring in June.

Economists at Citigroup say the important employment component "probably slipped a bit, after the surprising pickup in May."

Thursday:

8:15 - The ADP Employment Report is

anticipated to show the economy created 70,000 private jobs in June,

setting the stage for Friday's BLS nonfarm payrolls survey to show

110,000 new jobs in both the public and private sectors. In May, ADP

reported just 38,000 new jobs, the smallest gain since September. That

was followed by a BLS payrolls gain of 88,000 last month, the weakest in

eight months.

According to Thomson Reuters, economists believe

more than 150,000 total jobs must be created each month to hold the

unemployment report, which is currently at 9.1%.

8:30 - Jobless Claims have

been deeply uninspiring recently. New claims have so far averaged

426,000 per week in June, compared with 427,000 in May, as weekly claims

have remained above 400k for 11 straight weeks. This week's forecast is

420k, a figure that looks slightly optimistic next to the four-week

average of 426,750.

"The claims data suggest that May's

lackluster pace of job creation continued into June," said economists at

RDQ Economics. "The message of weaker labor market conditions in June

than what was seen earlier this year has been corroborated by consumers'

perceptions of the labor market and the employment component."

Economists

at Citigroup suggested there could be some upside risk to the consensus

forecast due to flooding and wildfires in the Midwest and Southwest,

coupled with seasonal issues as the school year ends.

"Continuing

jobless claims probably fell by 52,000," they said, noting that tally

fell fell 14k to 3.702 million last time. "But the drop was on account

of the larger seasonal factor, as unadjusted filings were virtually

static during the reference period."

11:00 - Treasury announces the details of 3-yr, 10-yr, and 30-yr debt supply to be sold in the following week

12:30 - Thomas Hoenig, president of the Kansas City Federal Reserve, speaks to the Chickasaw Nation Business and Community Leaders lunch in Ada, Oklahoma.

The June MBS prepayment report will be released on Thursday night.

Friday:

8:30 - The most closely watched economic indicator isn't expected to bring optimism to the markets. Nonfarm Payrolls are

anticipated to grow by 110,000 in June, following just 54,000 new jobs

in May. That figure is, of course, more than double the pace of growth

in May, but the six-month average is 179,000; with the unemployment rate

at 9.1%, 110k just isn't enough.

"U.S. firms are facing a number of

headwinds - higher gasoline prices, supply chain issues in

manufacturing, Europe's sovereign debt woes, and a generally more

downbeat outlook - prompting them to put off hiring for now," said

economists at BMO Capital Markets. "Some of those headwinds have started

to subside, suggesting payroll growth will rebound in the second half

of the year."

Economists at Janney Capital Markets note that

population growth adds about 75k - 90k new employees onto the markets in

an average month, so "May's job growth was actually negative in 'real'

terms."

"That deeply disappointing result marked the transition

of economic dead leaves from a likely transitory issue to a potentially

longer-lived one and heralded a sharp widening in credit spreads and

selloff in the equities sector," they said, suggesting June's numbers

thus take on added significance.

10:00 - Inventory growth in the Wholesale Trade report

is expected to continue expanding, but at a slower pace than May's 0.8%

advance. Over the prior 12 months, inventories jumped 13.8%.

"Inventories

tend to show weakness when commodity prices are declining and that does

present some downside risks to wholesale inventories in May and June,"

said economists at Nomura Global Economics.

3:00 - Consumer Credit is

expected to continue growing for the eighth consecutive month in May.

The consensus forecast looks for a $4 billion expansion, versus an

average of $4.8 billion over the past seven months. The April report

showed expansion of $6.3 billion, but as with previous reports the

improvement was lopsided with installment lending from the federal

government - mostly through student loans - playing a large role.

"Why

are we not seeing a more rapid expansion of consumer credit?" asked

economists at IHS Global Insight last month. "The answer lies in the

main drivers behind consumer spending. With the housing sector bouncing

along the bottom and employment making relatively slow progress, both

household wealth and incomes remain depressed. As such, consumers

continue to closely monitor their spending, and avoid unnecessary

purchases."

CURRENT GUIDANCE: After all the quarter-end "position squaring" that's occurred recently, bond traders are ready to make a move in either direction. Unfortunately the path of least resistance is likely higher until equities run out of steam. So, regardless of our weak econ recovery viewpoint, we’re defensive, especially when you add in the potential for political pandering in the debt-ceiling debate.