Today we got the "final" read on Q4 GDP. I say "final" because this report will be revised for years to come, it just won't be highly publicized. The market was expecting Q4 GDP to come in around +5.9%. This would have been no change from the "preliminary" GDP print (the first revision of the "advance" data).

The actual print: +5.6%. This was worse than anticipated

The increase in real GDP in the fourth quarter primarily reflected positive contributions from private inventory investment, exports, personal consumption expenditures (PCE), and nonresidential fixed investment. Imports, which are a subtraction in the calculation of GDP, increased.

The Federal Reserve's preferred gauge of inflation, the Core PCE Price Index (strips out food and energy), rose from an originally reported +1.6% to a final of +1.8%. This is above the Q3 read of +1.2%. The PCE Price Index, which includes the volatile commodity based food and energy indexes, rose by 2.5%. This is higher than the preliminary read of +2.3%.

Consumer spending was revised lower thanks to a small decline in durable goods and services. Demand for durable goods rose 0.4% vs. an initially reported +0.2%.

One of the categories I believe will help lead aggregate demand from anemic levels is Business Investments. Firms will look to reduce costs by increasing productivity and efficiency via investments in new technology (scary outlook for the labor market!). Unfortunately business investments were revised much lower, from the preliminary print of +6.5% down to +5.3%. While much less than first reported...this is still an improvement from the 5.9% contraction in Q3.

NOW FOR BUSINESS INVENTORIES.

When consumer demand is falling, like it has been over the course of the last two years, businesses cut back on production of goods to align their output of supply with consumer demand. This afffects the entire supply chain as purchase managers slow orders of the raw and intermediate materials necessary to complete their finished widget.

This affects consumers in a few ways, the most obvious being LESS JOBS. Why? When firms slow production, they need less labor to fill orders, so they stop hiring and cut hours and positions. The more businesses are cutting inventories, the worse it is for GDP. Once businesses stop reducing inventories and begin rebuilding inventories, it will be a big contributor to month over month percentage GDP gains.

Business Inventories shrunk by $19.7 billion in Q4 2009. This is higher than the originally reported decline of $16.9 billion but much better than the Q3 2009 reduction of 139.2 $billion. Remember...less contraction is good for GDP. So this is a modest step back. But then again...this data will be revised for years to come, so the small revision for the worse isnt that big of a deal in the big picture.

The change in real private inventories added 3.79 percentage points to the fourth-quarter change in real GDP, after adding 0.69 percentage point to the third-quarter change.

Also notice housing investment was revised for the worse as well. Just as I not all that worried about a lack of new home sales, I am not so concerned about a decline in housing investment. We need to get rid of current inventory (including shadow) before worrying about new building. Just another reason to believe the overall macroeconomic recovery will be slow...led by investments in technology and productive businesses (bad for human labor!).

Here is a table recapping the data:

Keep the 5.6% gain in perspective. The media will spin this as a great improvement, however I must point out the gains are coming off of record low levels. Example: going from 1 to 2 is a 100% uptick. Besides that, this data is backward looking and it wasn't all that different from the previous two (advance and preliminary) prints...SO IT HASNT BEEN MUCH OF A MARKET MOVER!

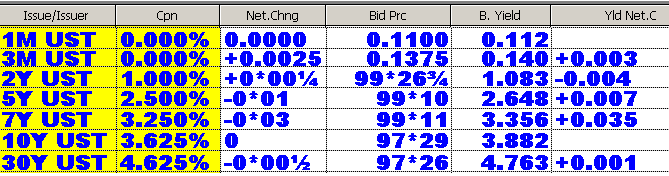

After high volume overnight bargain buying pushed 10s back down to the 3.85% pivot point, the 3.625% coupon bearing 10 year Treasury note is -0-01 at 97-28 yielding 3.888%.

Mortgages are faring better. The FN 4.5 is +0-03 at 100-07.

It was encouraging to see overnight bargain buying again, especially after three terrible turnouts from indirect bidders at this week's round of Treasury auctions. It is still possible that 10s test 4.00% s meaningful reversal in benchmark 10 year notes in seen. We are still acting as spectator vs. speculators at the moment. The abrupt spike in yields this week has us in a defensive posture....wait and see.

Stocks barely budged after GDP .Most markets are essentially flat at the moment. Rate sheets should reflect that....

UPDATED AT 10:00AM

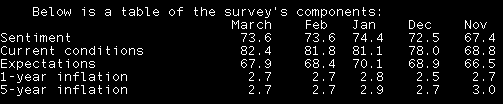

09:55 26Mar10 RTRS-REUTERS/U.OF MICH US CONSUMER SENTIMENT FINAL MARCH 73.6 (CONSENSUS 73.0) VS FINAL FEB 73.6

09:55 26Mar10 RTRS-REUTERS/UNIV OF MICH CURRENT CONDITIONS FINAL MARCH 82.4 (CONSENSUS 81.5) VS FINAL FEB 81.8

09:55 26Mar10 RTRS-REUTERS/U. MICH CONSUMER EXPECTATIONS FINAL MARCH 67.9 (CONSENSUS 67.6) VS FINAL FEB 68.4

09:55 26Mar10 RTRS-REUTERS/UNIV OF MICH 12-MONTH ECONOMIC OUTLOOK FINAL MARCH INDEX 78 VS FINAL FEB 80

09:55 26Mar10 RTRS-REUTERS/U. MICH FINAL MARCH 1-YR US INFLATION EXPECTATION MEDIAN 2.7 PCT VS FINAL FEB 2.7

09:55 26Mar10 RTRS-REUTERS/U. MICH FINAL MARCH 5-YR US INFLATION EXPECTATION MEDIAN 2.7 PCT VS FINAL FEB 2.7

09:55 26Mar10 RTRS-REUTERS/U. MICH FINAL MARCH CURRENT CONDITIONS INDEX AT HIGHEST SINCE MARCH 2008

The curve is still mostly unchanged after the data....

Come on real money bargain buying rally!

FIRST TARGET: 3.85%