I have some unexpected good news

Amidst an atmosphere of major market uncertainty, consumer borrowing costs improved significantly today. Enough to push BestExecution quotes a notch lower.

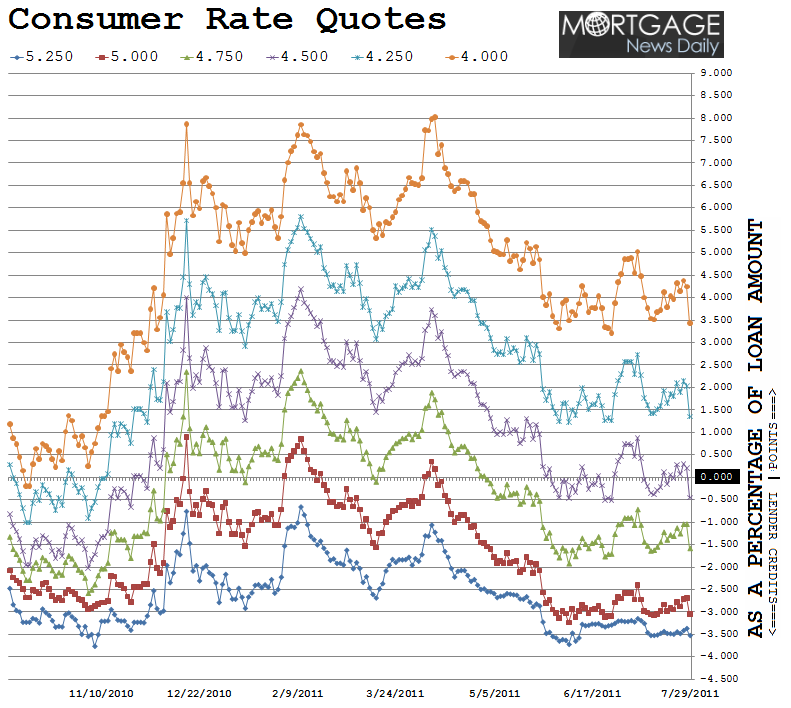

In the chart of Consumer Rate Quotes below, if the line is moving up, closing costs are on the rise. If the line is moving down, costs are on the decline. More recently consumer borrowing costs have crept higher, that is until today when costs dipped following a poor read on 2nd quarter GDP. Mortgage rates are once again just above their best levels of the year....

The chart above compares the average origination costs (as a percentage of loan amount) for several available mortgage note rates as quoted by the five major lenders. Each line represents a different 30 year fixed mortgage note rate. The numbers on the right vertical axis are the origination closing costs, as a percentage of your loan amount, that a borrower would be required to pay in order to close on that note rate. If the note rate graph line is below the 0.00% marker, the consumer may potentially receive closing cost help from their lender in the form of a lender credits. If the note rate line is above the 0.00% marker, the consumer should expect to pay additional points at the closing table to cover permanent buydown costs and origination fees. PLEASE SEE OUR MORTGAGE RATE DISCLAIMER BELOW

IMPROVED CURRENT MARKET*: The BestExecution conventional 30-year fixed mortgage rate has improved to 4.50%. On FHA/VA 30 year fixed BestExecution is now 4.375%. 15 year fixed conventional loans are best priced at 3.75%. Five year ARMs are best priced at 3.25% but the ARM market is more stratified and there is more variation in what will be BestExecution depending on your individual scenario.

ONGOING GUIDANCE: Floating in this environment is a crapshoot. Both stocks and bonds are maneuvering through major market uncertainties. Investors are focused on news headlines regarding U.S. budget issues, EU debt contagion concerns, economic data, and quarterly earnings. That puts the direction of mortgage rates at the mercy of factors that don't exactly adhere to schedules or expectations. While we still view underlying economic fundamentals as being supportive of lower mortgage rates in the future, the short-term risks associated with a potential U.S. debt default leave us more inclined to advise locking, especially deals that must be ready to close in the next 10-15 days. This provides protection from rising rates and still gives your lender a chance to negotiate if rates decline.

A little added perspective is necessary after the unexpected rally we experienced today...

The bond market and mortgage rates have yet to show fear over the potential for a U.S. credit rating downgrade or even worse, a default. Clearly this is surprising as politicians seem nowhere near a deal on the debt ceiling, which implies lawmakers are ready to play chicken with global financial markets. From that view, eventhough rates rallied pretty heavily today, we're still dealing with an "anything can happen" environment where volatility reigns supreme. If you're nervous like we are about what might happen on August 2nd, it makes sense to lock right now, especially with loan pricing near the best levels of the year. If you've got time to float or have no problem gambling with your rate quote, there is a chance that rates continue to rally next week on a "flight to safety" (no default = no reason to sell Treasuries). This is a highly-speculative decision though, a real crapshoot.

GUT FEELING: Default would be political suicide for all parties involved, making it a highly unlikely event. But if we were to default on a debt coupon payment, there would be a huge margin call followed by massive deleveraging in the short-end of the Treasury yield curve and a major repricing across the credit spectrum (which would be intensified by MBS duration shedding aka "snowball selling" <--- bad news for mortgage rates). In our opinion the more probable scenario is Congress fails to come to an agreement by August 2nd, forcing Treasury into so called “prioritization payment mode” to avoid default, which would be followed soon thereafter by another band-aid bill to raise the debt ceiling by just enough to get us into 2012 where Republicans would proceed to relentlessly hammer Obama’s tardiness on fiscals issues, just in time for the next election. If that scenario were to play out we wouldn’t necessarily be looking at a credit downgrade though. It’s still 50/50 at that point, totally dependent on the credibility of whatever plan is being debated at the time and how quickly Congress acts to raise the debt ceiling (Congress would need to act quickly though because Treasury makes around 3 million payments per day and does not have the systems to "prioritize" payments). Even if our credit rating was downgraded we wouldn't expect panic in the bond market. It would likely lead rates higher temporarily, especially once investors refocus on weak U.S. economic fundamentals.

----------------------------

*BestExecution is the most cost efficient combination of note rate

offered and points paid at closing. This note rate is determined based on the

time it takes to recover the points you paid at closing (discount) vs. the

monthly savings of permanently buying down your mortgage rate by 0.125%.

When deciding on whether or not to pay points, the borrower must have an idea of

how long they intend to keep their mortgage. For more info, ask you originator

to explain the findings of their "breakeven analysis" on your

permanent rate buy down costs.

*Important Mortgage Rate Disclaimer: The BestExecution loan

pricing quotes shared above are generally seen as the more aggressive side of

the primary mortgage market. Loan originators will only be able to offer these

rates on conforming loan amounts to very well-qualified borrowers who have a

middle FICO score over 740 and enough equity in their home to qualify for a

refinance or a large enough savings to cover their down payment and closing

costs. If the terms of your loan trigger any risk-based loan level pricing

adjustments (LLPAs), your rate quote will be higher. If you do not fall into

the "perfect borrower" category, make sure you ask your loan

originator for an explanation of the characteristics that make your loan more

expensive. "No point" loan doesn't mean "no cost" loan. The

best 30 year fixed conventional/FHA/VA mortgage rates still include closing

costs such as: third party fees + title charges + transfer and recording. Don't

forget the fiscal frisking that comes along with the underwriting process.

CAUTION: MND guidance is speculative in nature. We don't have a

crystal ball, we can't predict the future, we can only share our outlook.

Making the following considerations extra important........................

What MUST be considered BEFORE one thinks about capitalizing on a rates rally?

1. WHAT DO YOU NEED? Rates might not rally as much as you

want/need.

2. WHEN DO YOU NEED IT BY? Rates might not rally as fast as you

want/need.

3. HOW DO YOU HANDLE STRESS? Are you ready to make tough

decisions?