Much has been made lately over the propensity of so-called millennials, the demographic cohort which is now between 18 and 34 years of age, to forgo homeownership. In its September Public Outlook Freddie Mac points out that this is not without an upside.

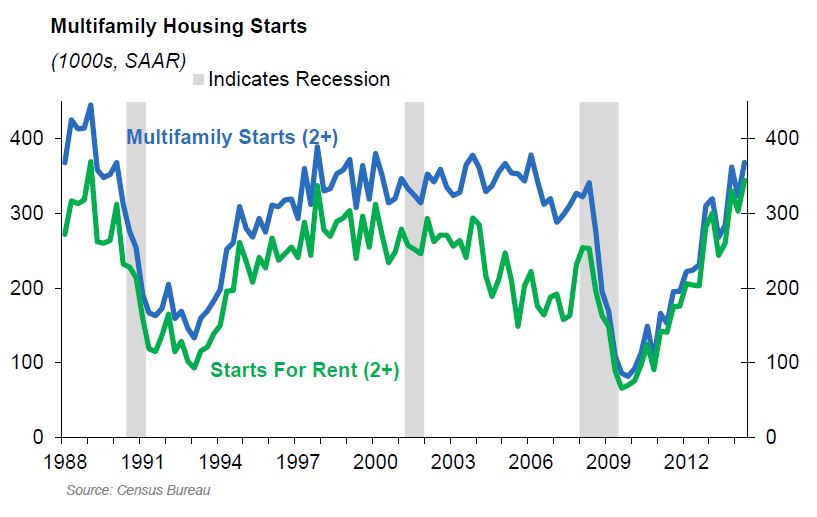

The monthly report, written by Freddie Mac's Chief Economist Frank E. Nothaft and Deputy Chief Leonard Kiefer, concedes that the recovery from the Great Recession has been "extraordinarily slow" but it has picked up over the last couple of years and that increasing recovery has been led by the multifamily sector, especially the development of rental apartments.

In July, housing starts rose to a seasonally adjusted annual rate of 1.09 million units and on an unadjusted basis was the highest monthly start rate in more than six years, 101,000 units. Construction of buildings with at least five units hit the highest monthly construction pace since early 2006, but today, unlike then, condominium complexes are not the driving force.

A demand for rental units, especially by younger households, has created a boom in the construction of rental apartments and in 2014 that construction has been running at the highest level in a quarter century. Outlook quotes the National Multifamily Housing Council's report that the apartment market had tightened even further over the prior three months as of mid-July.

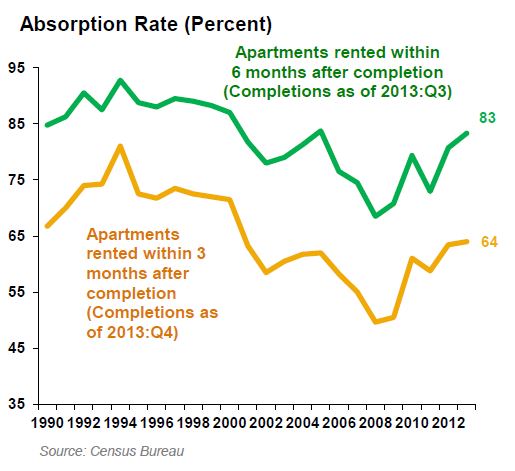

The tightened market means that the absorption rate of rental units has also picked up and the most recent figures for newly built, unfurnished, unsubsidized apartments puts rentals at the fastest pace in a decade. The Census Bureau puts the most recent 3- and 6-month absorption rates at 64 percent and 83 percent respectively showing, the economists say, that the demand is there to absorb the new supply.

The increased demand is, of course, a reciprocal of the decline in overall homeownership in the U.S. which fell to 64.7 percent in the second quarter, the lowest rate since 1995. Indeed, over the past four quarters all growth in household formation has belonged to renters.

The decline in homeownership has been primarily concentrated among younger households. Among households under age 35 it has fallen from 43.6 percent in the second quarter of 2004 to 35.9 percent ten years later.

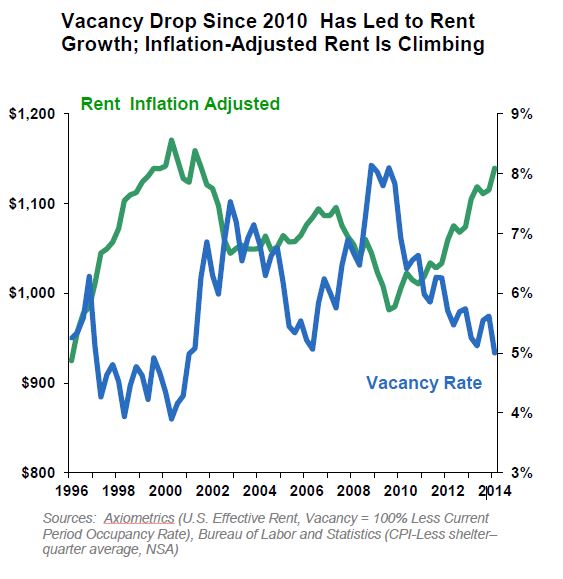

Vacancy rates have also tumbled to their lowest levels since 2000 which has place upward pressure on rents. On average, Freddie Mac says, inflation adjusted rents have returned to their peak levels of 14 years ago and the low vacancy rates appear to be positioning rent increases to outpace the growth in operating costs over the coming year.

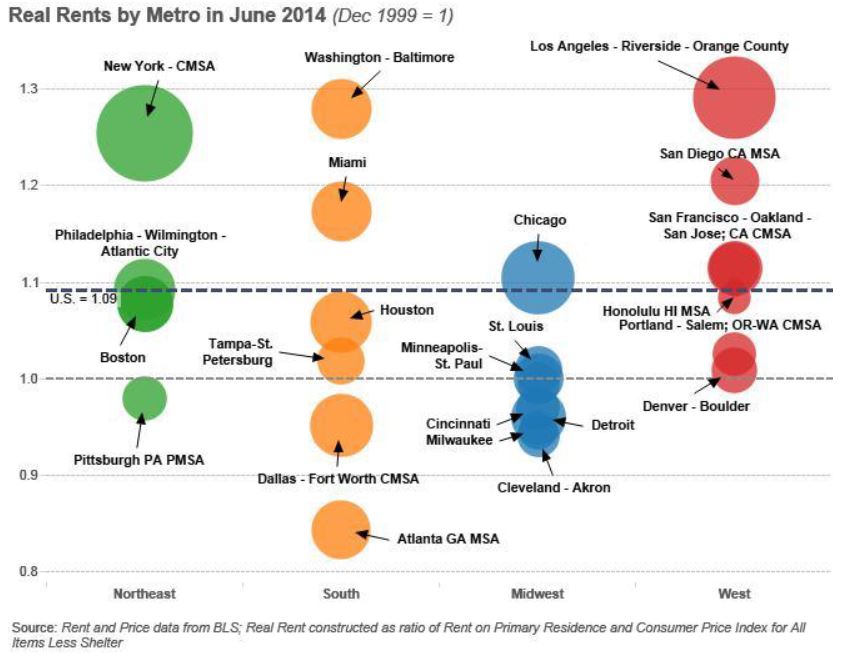

Comparing estimates of rents on a primary residence to consumer prices for non-shelter items gives a real (inflation adjusted) rent growth of 9 percent over the period from December 1999 to June 2014. This figure has varied across metropolitan areas with rent growth generally highest in large metros and those in the West or Northeast. In the south only Miami and the Washington-Baltimore area have had real rents exceeding the national average. In the Midwest Chicago is the only city to beat that average.

Nothaft and Kiefer see the multifamily sector continuing to be the bright spot in housing. Despite the relatively weak August jobs report they expect to see the labor market peak up steam in the coming month and with that improvement household formation should increase. This will translate into increased demand for apartments and other rental units.