In its latest Mortgage Monitor, Black Knight analyzes the impact the elimination of the 50 basis point adverse market fee from the cost of Fannie Mae and Freddie Mac (the GSEs) refinances. The Federal Housing Finance Agency (FHFA) removed the fee, originally scheduled to go into effect on September 1, 2020 to cover some of the anticipated costs from pandemic relief measures, in mid-July. While the implementation was later delayed until December 1, the company says the September announcement began to immediately trigger increases in rate offers.

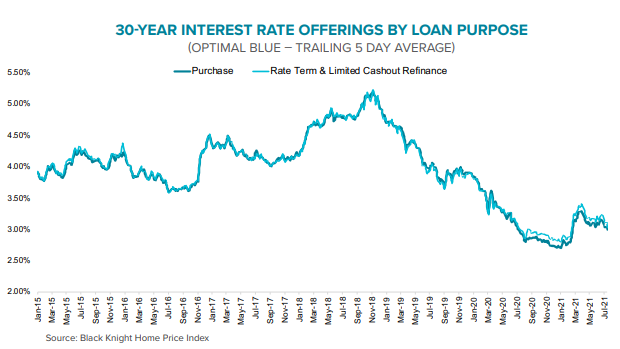

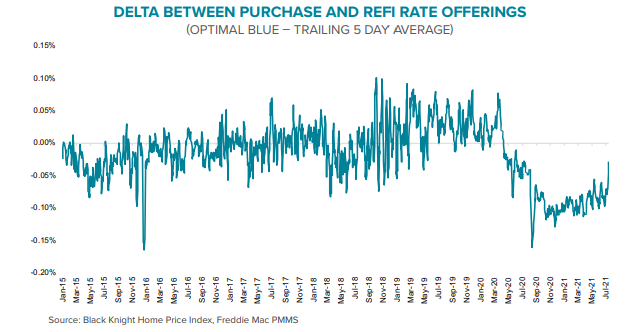

From November 2020 through May 2021 refinance rate offers were nearly a full 1/8th of a point higher on average than those for similar purchase loans. However, within a week of the FHFA's July 16 announcement that the fee was disappearing, the delta between the two types of loans was all but gone. By July 19, offerings on purchase and refinance loans were nearly identical and on July 20 refi offerings were 4 basis points below those for purchases for the first time since June of last year.

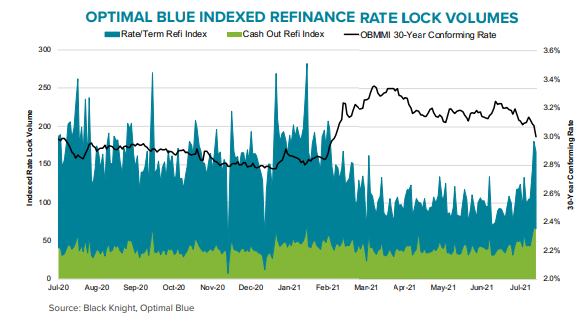

The combination of the fee removal and a return of a declining 10-year Treasury yield has returned 30-year rates back to mid-February lows. This has led to an increase in refinancing incentive and a corresponding surge in refinancing rate locks. As of July 22, there were 15.1 million high quality refi candidates in the market, an increase of 10 percent from the prior week and 25 percent from late June. Those candidates could save an aggregate of $4.5 billion each month by refinancing.

Black Knight says homeowners are starting to respond to the incentive. Refi rate locks increased 23 percent during the week ended July 21 and rate/term refinances rose 31 percent during that period, to the highest levels since early March.

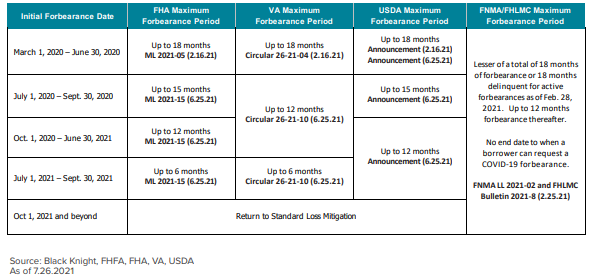

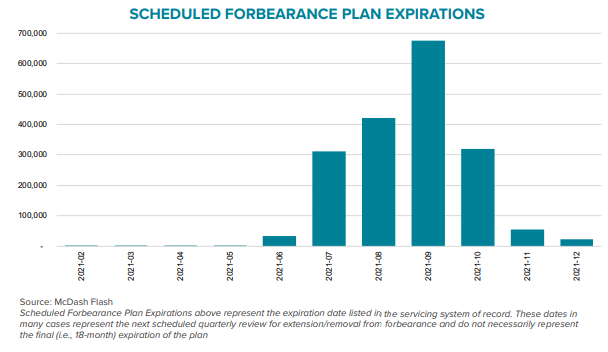

The Monitor also looks at what may be coming as the 18 months of forbearance protection for U.S. homeowners rolls to a close. The company says that servicers are facing a monumental task going into the fall, perhaps needing to process up to 18,000 expiring forbearance plans per business day. This dauting prospect is further complicated by new expiration timeless for loans backed by FHA, VA, and USDA and complex loss mitigation waterfalls.

The new timelines resulted in the matrix below, of which Black Knight Data & Analytics president Ben Graboske says, "The operational challenge this represents is staggering, even before noting the oversized share of FHA and VA loans." Those loans at present make up over 40 percent of the forbearance program's total participants. FHA loans in the program are more than threefold those serviced for the GSEs.

Attempts to mitigate expiration problems appear to be a prime example of unintended consequences. Graboske explains: "Prior to the agencies issuing clarifying guidance on allowable forbearance periods, some 950,000 plans were set to expire over the final six months of the year - representing about half of all loans in forbearance. That estimate assumed a blanket 18-month maximum allowable forbearance period. However, now we have detailed matrices of differing forbearance periods across the various agencies. Depending upon the specific agency and when forbearance was initially requested by the homeowner, a plan can have a 6-, 12-, 15- or 18-month limit. Assuming borrowers stay in for the maximum allowable term, this means plans that started as much as seven months apart are now scheduled to expire simultaneously, frontloading expirations of forbearance plans sooner than estimated.

"As a result, 65 percent of active plans - representing approximately 1.2 million homeowners - are now set to expire over the rest of 2021, including nearly 80 percent of all FHA and VA loans in forbearance. Nearly three quarters of a million plans would expire in September and October alone. Given the heightened challenges those [FHA, VA, and USDA] borrowers may face in returning to making mortgage payments as compared to those in GSE loans, effective loss mitigation efforts and automated processes become even more critically important."

Strong declines around the 4th of July holiday, driven by review activity of early forbearance entrants reaching the 15th month of their plans, pushed active plan volumes to their lowest levels since early April 2020, but about 1.86 million loans remain, 3.5 percent of all mortgages. There are still opportunities for further reductions over the next two months, before a tidal wave of 18-month expirations hits servicers in September.

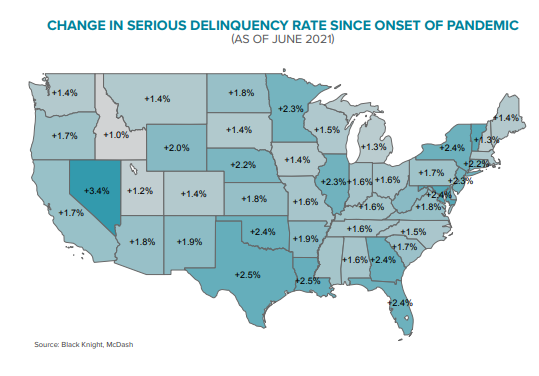

As Black Knight reported in its "first look" at June data last month, the number of non-current loans did decline during the month, but there are still more than 1.1 million more seriously delinquent mortgages than before the pandemic. This means that about 2 percent of all loans are more than 90 days past due because of the COVID virus. Every state has seen an increase in its serious delinquency rate of at least 1 percent with Hawaii and Nevada, both heavily dependent on a tourist economy, up by 3.4 percent.

The company estimates that past due mortgage payments, while beginning to edge lower, total $64 billion (including about $14 billion in past due taxes.) This is about double the amount owed pre-pandemic. The American Rescue Plan allocated $9 billion as homeowner assistance funds (a bit of a misnomer as part of it is designated for helping renters) with a minimum of $50 million going to each state. If all those funds were provided to homeowners, it would bring current all loans in some states, but in others it will cover only a fraction, for example around 10 percent in New York and Hawaii. This leaves a huge deficit to be resolved through post-forbearance deferral programs, loan modifications, and economic expansion.