In the S&P/Case-Shiller home price indices report for April David M. Blitzer, Managing Director and Chairman of the Index Committee at S&P Dow Jones Indices notes that, "Sales of new and existing homes are rising in recent reports and construction of new homes enjoyed strong gains in May. At the same time, the proportion of new construction that is apartments rather than single family homes remains high." Over the last year, he says, 34 percent of housing starts were apartments compared to an average of 22 percent over the years since 1975. He points out that one aspect of this could be an increase in condominium construction and that in all five of the cities in which Case-Shiller tracks condos, their prices are rising faster than single family homes.

In the June edition of RealtyTrac's HousingNewsReport Blitzer expands on that statement, saying that "The U.S is witnessing a shift from single family homes to apartments and condominiums." This is evidenced not only in the multifamily share of housing starts, which rose from 19.8 percent during the period of 2000 to 2004 to 35.2 percent in the 15 months that ended this past March, but also in the decline in homeownership. These indicate both a move from owning to renting and a move from single to multi-family housing.

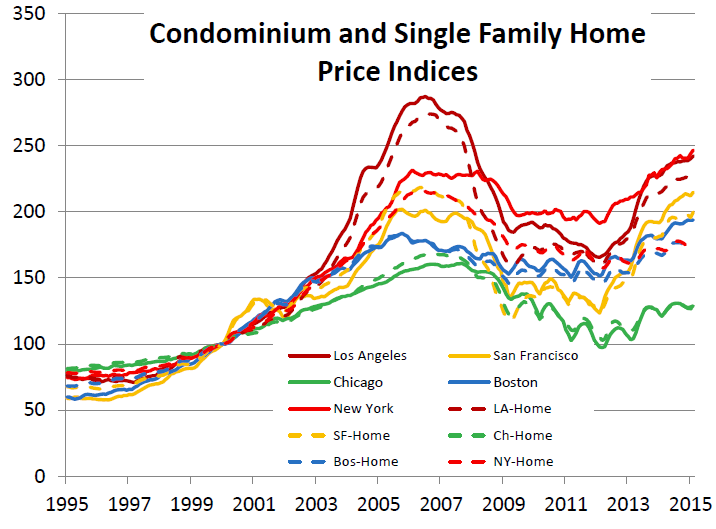

He points out that there are relatively few analyses that focus on the condominium sector during the housing boom and its aftermath so he uses the Case-Shiller price information on Los Angeles, San Francisco, Chicago, Boston and New York and compares it to the corresponding single-family Case-Shiller data for those cities. The data covers the entire metropolitan area in each case, not just the central cities.

Blitzer says that condo prices have recovered from the housing bust more quickly than single-family houses. New condo price peaks have been set since the recession in San Francisco, Boston, and New York. Only two cities among the 20 in which Case-Shiller tracks single-family home prices, Denver and Dallas, have set new highs, it seems to be condos in dense urban areas that are staging strong recoveries.

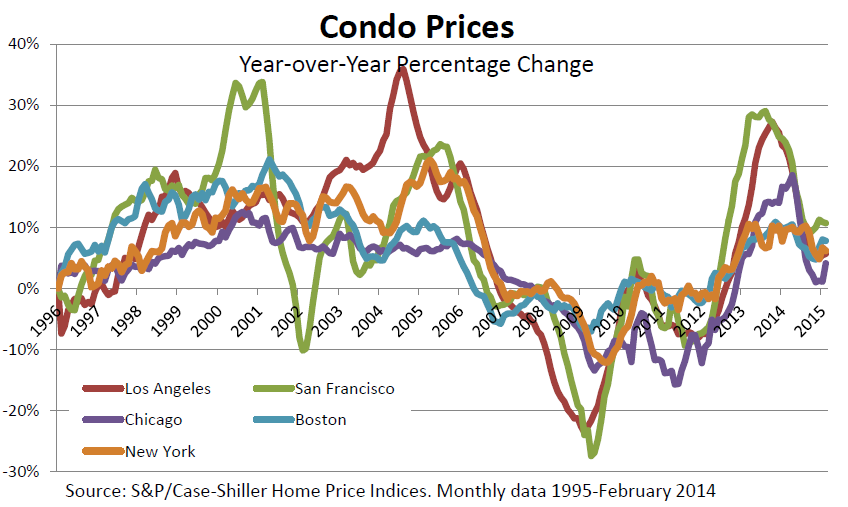

The figure below shows how condo prices changed on an annual basis in each of the five cities between January 1996 and February 2015 and illustrate the individual ways each city reacted to economic events. The tech boom in the late 1990s and bust in 2000 to 2001 are clear in the San Francisco data. Although the tech bust affected Wall Street as much as it did Silicon Valley prices in New York continued to show solid gains through both boom and bust and then accelerated after the 2001 recession through 2006 with condo prices peaking in March 2005 with a 20 percent annual gain.

In Los Angles condo prices gained 35 percent in the 12 months ending in August 2004. This reflected a response to gains in the national economy between 2002 and 2004 by a city with a diversified economy and a strong reliance on tourism as well as a spike in its population growth in the nine year that preceded the price surge. However Blitzer says there is no major development that can be easily identified in L.A. like the tech boom in San Francisco.

Chicago and Boston saw condo prices follow the other cities but without as sharp a pattern of peaks and troughs; a pattern more like that of their single family home prices. In each of the five cities the peak in condo prices occurred roughly at the same time as the peak in it single family house prices and the levels in condo prices and single family houses are similar - with no pattern among the cities as to which type housing had the higher peak.

When the housing crisis arrived both condo and single family prices collapsed and the peak to trough declines were very similar for each in Los Angeles and Chicago. In the other three cities the condo swing was slightly smaller. Condo prices hit bottom in all five cities in either February or March of 2012, the same time frame generally given for the trough in single family home prices.

Blitzer says the data for the five cities shows generally similar price patters with some indication that condo prices may be slightly less volatile and gives no support to ideas that ownership in condos follows a different pattern than in single family homes or is more transitive. He concludes that "While the shift in consumer preferences for condos versus single family homes seen in the housing starts data may be a change in people's housing preferences or housing affordability, it does not appear to be changing the patterns of price movement. Moreover, the shift to condominiums isn't likely to make home prices more or less volatile than in the past. It certainly won't reduce the risk of another housing boom-bust cycle in the future.