Fannie Mae has again downgraded expectations for economic growth in 2016. Doug Duncan, senior vice president and chief economist and the ESR Macroeconomic Forecast Team said on Tuesday that the 0.5 percent annualized growth in the first quarter GDP was the weakest in two years, well below the company's expectations at 1.2 percent. It was the third year in a row that first quarter growth was below 1.0 percent although in the previous two there was a bounce back in the second quarter.

The economic team had originally projected 2.2 percent annual growth this year but downgraded that in its April forecast to 1.9 percent. The Economic Summary for May now projects growth of 1.7 percent.

The slowdown was broad-based but the one bright spot was residential investment which added 0.5 percentage points to growth, the largest contribution since the fourth quarter of 2012. There was also what the economists called modest stimulus from the recent federal budget deal. They expect both housing and government to contribute to growth for the remainder of the year.

The possibility of a rate hike at the June 2016 Federal Open Market Committee (FOMC) meeting remains on the table and Fannie Mae notes that the post-meeting statement from April suggests that the Fed is less worried about financial turmoil abroad. Still, Fannie Mae is sticking with its earlier projection of only one 2016 rate hike, probably in the second half of the year. (Who knows how this view might change following this week's FOMC Minutes...)

Home sales in the first quarter of 2016 were moderately better than in the last quarter of 2015 although month-to-month changes have been "lackluster." New home sales have fallen for three straight months while existing home sales partially rebounded in March from a February slump. Leading indicators suggest a pickup in home sales going into spring. Pending home sales rose in both February and March and the average purchase mortgage application index rose in March and April while mortgage rates continued to edge lower.

Homebuilding activity continued to disappoint although the decline in both permits and housing starts were largely due to the volatility of the multi-family sector. One of the main headwinds for multi-family construction is an excess supply of high-end apartment buildings in ten of the largest cities although there is still plenty of demand for affordable rentals. The financing environment for new multifamily construction has become more difficult. The Federal Reserve's Senior Loan Officer Opinion Survey shows a net percentage of banks are tightening standards for commercial real estate loans.

Single-family construction is more positive. Starts are up 22 percent from the same period last year, but that gain is still off of depressed levels.

The leading home price indices - Case-Shiller, FHFA, and CoreLogic - show strong annual appreciation ranging from 5.3 to 6.0 percent during the first two months of the year. Lean inventory and fewer distressed sales continue to support price gains.

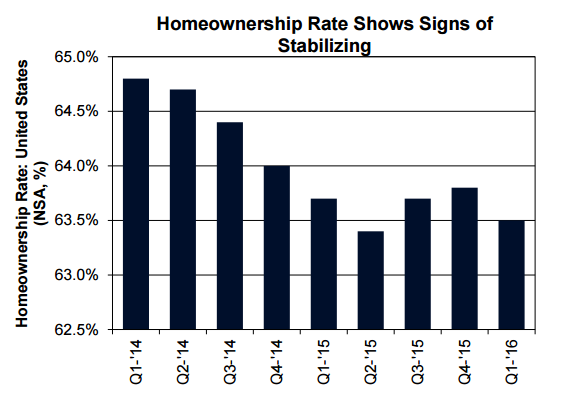

Homeownership appears to be stabilizing. The Census Bureau's Housing Vacancy Survey for the first quarter shows the rate down 0.3 percent from the previous quarter and 0.2 points from a year earlier to 63.5 percent which Fannie Mae says is the level around which it has hovered for the last four quarters. That the Baby Boom generation is still maintaining high rates has helped offset the low homeownership so far among the even larger Millennial generation.

The company still expects the 30-year fixed rate mortgage to be at 3.7 percent in the fourth quarter but has raised its total home sales forecast for the year to 6.02 million as the upward revision in existing home sales outweighed the downward revision in new home sales.

Incoming data suggestions that mortgage originations for both purchase and refinance have been stronger than anticipated so the company has upgraded its estimates for the first quarter and the entire year. "For purchase originations, we lowered our assumed share of home sales using cash through the first quarter of 2017. For all of 2016, we expect total mortgage originations to decline 3.7 percent from 2015 to $1.65 trillion, as the 18.8 percent drop in refinance originations outpaces the 9.4 percent rise in purchase originations. The refinance share should decline to 39 percent in 2016 from 46 percent in 2015. Total originations should decline further in 2017, as a drop in refinance originations continues to outweigh an increase in purchase originations. We project total production volume to be $1.45 trillion in 2017, with the refinance share sliding further to 30 percent," the report says.