Fannie Mae has lowered its forecast for first quarter 2018 growth from 2.9 to 2.8 percent due to "lackluster consumer spending and nonresidential and residential investment. The second report of 4th Q GDP downgraded real growth by one-tenth to 2.5 percent annualized. Incoming data has shown weaker domestic demand, with real consumer spending down 0.1 percent in January, the biggest monthly drop in a year. Based on this, Fannie also lowered its real consumer spending growth forecast for the first quarter to 2.2 percent annualized from 2.7 percent in the February forecast.

FY 2019 looks brighter, and the company's economists have raised their full-year 2019 GDP forecast to 2.5 percent and lowered their outlook for unemployment to 3.6 percent. They stress that more rapid wage and inflationary pressure might lead the Fed to more aggressively tighten monetary policy which would pose downside risks for their projections.

Their view of housing reflects the mixed start to the year. January's single-family construction starts partially recovered from their double-digit dive in December and multifamily starts, at 500 units, surprised everyone. It was the highest level for those starts since the end of 2016. Multifamily permits were up for the first time in three months.

Existing home sales, on the other hand, kicked off the year with their second consecutive decline. While demand is solid, inventories are continuing to shrink. Pending home sales, a leading indicator, also fell sharply in January, portending more slowing in existing home sales ahead. New home sales were down as well, but upward revisions to earlier months tempered that news.

One reason for projecting a decline in the residential investment sector of the GDP mentioned above can be seen in the housing inventory numbers. The shortage of both new and existing home listings are constricting sales (and thus brokerage fees, a component of residential investment) and the new home inventory, while better than that for existing homes, continues to show the depressed level of construction activity.

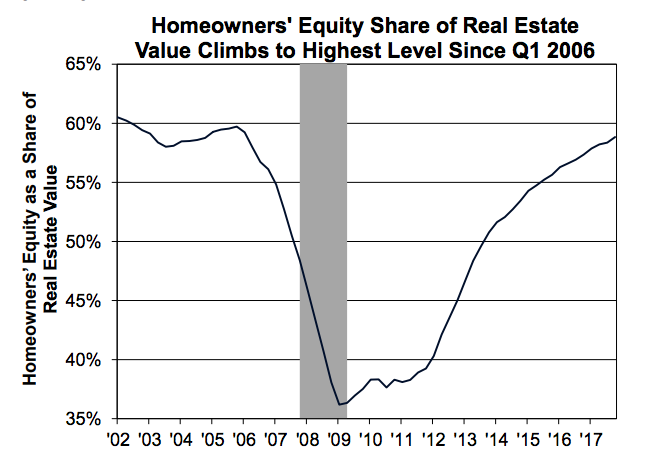

The pace of home price appreciation remained strong at the end of the year with most indices reporting more than 6 percent in year-over-year gains in December. While this appreciation hurts both sales and affordability, it helps boost homeowner equity. During the fourth quarter of 2017, that equity, expressed as a share of real estate value, reached its highest level in nearly 12 years.

The company's forecasts for housing activity and mortgage interest rates have not changed over the last month. The economists project that purchase mortgage originations will rise about 5 percent from 2017 to $1.19 trillion this year, while refinance originations will drop about 30 percent to $498 billion. Single-family mortgage debt outstanding grew 2.8 percent annualized during the fourth quarter, the slowest pace in three quarters, but for all of 2017, it increased 3.0 percent, the biggest annual gain since 2007.

Returning to the economy as a whole, Fannie Mae says a key downside risk for its forecast is a loss in business and consumer confidence if U.S. trade policy becomes more assertive and our trading partners retaliate. There are several occasions upcoming where this could happen, including the ongoing NAFTA negotiations and the August deadline for the investigation into China's intellectual property policies. There have already been tariffs imposed on steel and aluminum, lumber, solar panels, and washing machines, and the Trans-Pacific Partnership is launching without the U.S. on board.

The Bureau of Economic Analysis (BEA) added an adjustment to wage and salary income to reflect one-time bonuses awarded to some employees as a business response to the recent corporate tax cuts. The BEA also estimated a decline in personal taxes of 3.3 percent (regardless of whether employees adjusted their withholding schedules), the biggest drop since the recession. This will boost disposable personal income by the largest amount in a year, however Fannie Mae expects the lion's share of the income gains will be saved rather than consumed.