The holiday-shortened work week that just past stands in stark contrast to the week ahead which offers a robust calendar of events and economic data. The market's main focus is definitely the FOMC meeting announcement on Wednesday followed by the first ever post-meeting press conference where Fed Chairman Ben Bernanke will share the Board's updated Summary of Economic Projections.

The FOMC Statement is likely to show an unchanged monetary policy, but many questions remain unanswered: Is QE2 ending this summer as scheduled? Is the Fed increasingly concerned with inflation risks? How does the Fed view the ongoing recovery? Is commodity-price driven inflation still "transitory"? Below is an excerpt from the March 15, 2011 FOMC Statement:

"Commodity prices have risen significantly since the summer, and concerns about global supplies of crude oil have contributed to a sharp run-up in oil prices in recent weeks. Nonetheless, longer-term inflation expectations have remained stable, and measures of underlying inflation have been subdued....The recent increases in the prices of energy and other commodities are currently putting upward pressure on inflation. The Committee expects these effects to be transitory, but it will pay close attention to the evolution of inflation and inflation expectations."

FOMC headlines will be flanked by a nearly as potent Treasury auction cycle of $99-billion 2's, 5's, and 7's on Tuesday, Wednesday, and Thursday respectively. Bond investors have demonstrated hesitancy to rally beyond technical resitance levels. With the FOMC meeting hanging over the market's head on Tuesday and Wednesday morning, the 2 and 5-year auctions could get sloppy as traders remain defensively flat before the Fed offers its updated outlook. Thursday's $29-billion 7-year note auction will likely be dictated by the market's reaction to the Fed Statement/Updated Economic Projections on Wednesday.

We see the week ahead as an opportunity to either reverse or accelerate the positive trends that began on April 11th. This is one of those "crossroads" weeks.....

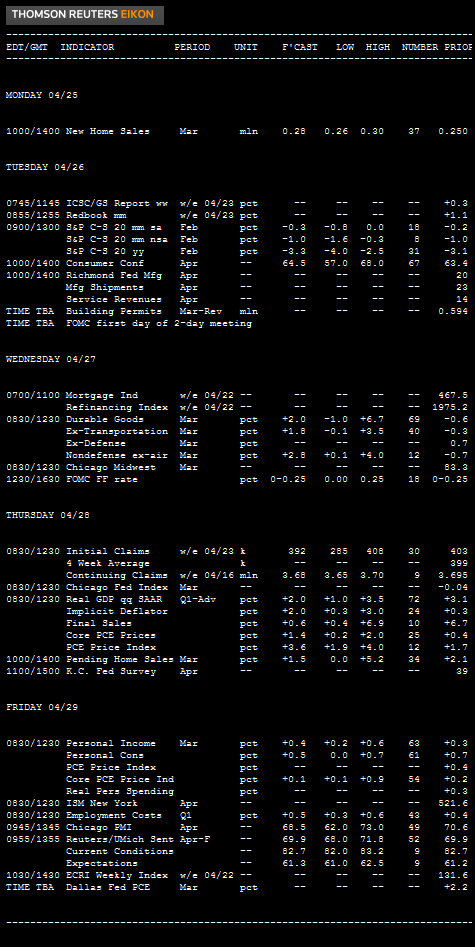

KEY EVENTS IN THE WEEK AHEAD

Monday:

10:00 ― The annual pace of New Home Sales is anticipated to jump to 280k in March from 250k a month before. The uptick would follow back-to-back declines including a 16.9% decline in February, which pushed the pace of a sales to a record low. Prices should help demand: the median rate was 8.9% lower than the same period in 2010

“Because new home sales are counted at contract-signing rather than at closing, this series tends to react quickly to changes in mortgage rates,” said economists at Nomura Global Economics, who predict a 16% climb. “So the slightly lower mortgage rates relative to the previous month probably helped boost new home sales.”

Economists at IHS Global Insight point out that new home sales were bouncing about the 300,000 mark for six months before February, so a sizable climb in March would mean little.

Tuesday:

9:00 ― The S&P Case-Shiller Home Price Index is expected to show prices were 4% lower than the same period one year ago. The index measures home prices in 20 key metropolitan areas across the country. It’s the most respected measure of prices available.

10:00 ― Consumer Confidence is anticipated to tick up to 65.0 in April from 63.4 last month. The index fell in the prior two months as oil prices soar and consumers fret about the war in Libya and the tsunami in Japan. The modest climb expected this month compares with an 8.6 point drop in the prior month.

“Even though gasoline prices have moved higher still in April, other indicators of sentiment have improved, probably driven by a strengthening labor market,” said economists at IHS Global Insight.

One key reason for the expected improvement in the preliminary survey from the University of Michigan: it beat forecasts by rising to 69.6 in early April, from 67.5.

1:00 ― Treasury auctions $35,000,000 2-year notes

Wednesday:

8:30 ― Economists look for Durable Goods Orders to jump 1.9% in March following a 0.6% cutback in February. Forecasts are diverse, ranging from 0.5% to 3%. Orders are expected to rebound following sharp reductions in machinery orders a month before.

“The advance report from durable goods manufacturers should confirm the strong new orders index readings from the ISM manufacturing index and regional Fed surveys,” said economists at Nomura, who expect a large increase in aircraft orders, paired with gains in electrical equipment and computers.

“The boost in orders would lead to more shipments and stronger GDP growth in the second quarter of 2011, which we currently expect to rise by a 3.3%,” they added.

10:00 - New Residential Vacancies and Homeownership data for the first quarter 2011 will be released. In the fourth quarter of 2010, the homeownership rate of 66.5 percent was 0.7 percentage points (+/-0.4%) lower than the fourth quarter 2009 rate (67.2 percent) and 0.4 percentage points (+/-0.4%) lower than the rate in the third quarter (66.9 percent). Homeowner Vacancy and Rental Vacancy statistics are from the Housing Vacancy Survey, which is a supplement to the Current Population Survey. The homeowner vacancy rate is the proportion of the homeowner inventory which is vacant for sale. The rental vacancy rate is the proportion of the rental inventory which is vacant for rent. A housing unit is vacant if no one is living in it at the time of the interview, unless its occupants are only temporarily absent. In addition, a vacant unit may be one which is entirely occupied by persons who have a usual residence elsewhere.

11:30 ― Treasury auctions $35,000,000 5-year notes. Competitive bids are cut-off at 11:30 instead of 1:00 to give investors a chance to prepare for the early release of the FOMC statement and the first ever post-meeting press conference with Fed Chairman Ben Bernanke.

12:30 ― The FOMC Statement is released. The announcement is likely to show an unchanged monetary policy, but many questions remain: Is QE2 ending this summer as scheduled? Is the Fed increasingly concerned with inflation risks? How does the Fed view the ongoing recovery? Is commodity-price driven inflation still "transitory"?.

Economists at Nomura expect the conference with Bernanke to provide some insight on the FOMC's economic outlook, “which has been lacking in the traditional press releases.”

2:15 - Chairman Ben S. Bernanke will hold the first ever press briefing on the Federal Open Market Committee's current economic projections to provide additional context for the FOMC's policy decisions. The introduction of regular press briefings is intended to further enhance the clarity and timeliness of the Federal Reserve's monetary policy communication. The Federal Reserve will continue to review its communications practices in the interest of ensuring accountability and increasing public understanding.

Thursday:

8:30 ― The first estimate of Q1 GDP isn’t expected to be pretty. Economists expect the growth rate at just 2%, versus a 3.1% pace to end 2010, even though manufacturing had a robust quarter.

“The combined effect of weak private service consumption, a decline in non-residential construction and a wider trade deficit likely lowered growth in the quarter,” said economists at Nomura.

8:30 ― Initial Jobless Claims have come in above 400k for two consecutive weeks now, but economists hope to see a decline to 390k in the week ending April 23. The average so far in April is 401k claims per week, versus 395k in March.

8:30 ― Federal Reserve Bank of San Francisco President John Williams and Federal Reserve Board Governor Elizabeth Duke give welcome/opening remarks before the Federal Reserve Bank of San Francisco's "The Changing Landscape of Community Development Linking Research with Policy and Practice in Low-Income Communities" 2011 Community Affairs Research Conference. No Q&A.

10:00 ― The Pending Home Sales Index is expected to show modest gains in March, as mortgage rates improve and springtime weather induces people to look for homes.

1:00 ― Treasury auctions $29,000,0000 7-Near Notes

Friday:

8:30 ― The Personal Income & Outlays survey is expected to show that income rose 0.3% for the second straight month, while spending should rise 0.5% following a 0.7% gain the month before. Core prices are to inch forward 0.1%, versus a 0.2% gain a month before. The survey won’t necessarily get too much attention, as much of the data will already be known from the GDP report a day before.

“Rising employment is supporting incomes, but incomes are not keeping pace with price inflation,” said economists at IHS Global Insight. “Consumer spending is expected to increase 0.5%, but after adjusting for inflation that should translate into only a 0.1% real increase.”

They added that much of the nominal spending “will be swallowed up by higher energy and food prices.”

8:30 - Federal Reserve Bank of St. Louis President James Bullard gives morning remarks before the Federal Reserve Bank of San Francisco's "The Changing Landscape of Community Development Linking Research with Policy and Practice in Low-Income Communities" 2011 Community Affairs Research Conference.

9:45 ― The Chicago Business Barometer is anticipated at a robust 68 in April, marking a slight dip from the 70.6 reported in March and the multi-decade high of 71.2 the month before.

“Respondents of the [March] survey claimed that higher commodity prices could hurt their future profits,” said economists at Nomura. “We expect this sentiment to be reflected in the moderate decline in the index, albeit a high level by historical standards.”

9:55 ― The final Consumer Sentiment survey for the month is expected to remain at 69.6 after gaining a moderate 2.1 points in the preliminary reading two weeks ago. The expected gain would be a turn in the right direction, but at near-six month lows it’s not much to be excited about.

12:30 ― Federal Reserve Chairman Ben Bernanke speaks on

"Community Development in Challenging Times" before Federal Reserve Bank

of San Francisco "The Changing Landscape of Community Development

Linking Research with Policy and Practice in Low-Income Communities"

2011 Community Affairs Research Conference. No

Q&A