Does anyone really believe Donald Trump is planning to announce his candidacy for U.S. President?

Most folks including me see it as a ploy aimed at attracting attention to the Trump brand. What's funny is he's actually pulled off this stunt in the past...more than once. Is Trump playing us for suckers?

The bond market faced a similar dilemma yesterday when Standard and Poor's assigned a negative outlook on the U.S. credit rating. In its report, S&P analysts based the decision on the inability of lawmakers to develop a consensus plan to "reverse recent fiscal deterioration or address longer-term fiscal pressures." Are politicians just playing us here? Is S&P just a pawn in the bigger budget game?

Republicans certainly sharpened their axes when the news flashed. The L.A. Times reports that House Majority Leader Eric Cantor (R-Va.) called the decision "a wake-up call" that supports the party's case for including further budget cuts as part of any move to raise the nation's debt limit.

The Administration was quick to respond with this quote, "As the President said last week, addressing the current fiscal situation is well within our capacity as a country. He has initiated a bipartisan process that will allow us to make progress on a balanced approach to restoring fiscal responsibility. The U.S. economy is strengthening as it emerges from the recent recession. Both political parties now agree that it is time to begin bringing down deficits as a share of GDP. S&P assumes that the U.S. will enact a comprehensive budgetary consolidation program – combined with meaningful steps toward implementation by 2013, but we believe S&P’s negative outlook underestimates the ability of America’s leaders to come together to address the difficult fiscal challenges facing the nation.”

Does anyone really believe S&P will actually strip the U.S. of its AAA credit rating?

Most folks including me see it as a ploy aimed at attracting attention to the politics of the issue. Maybe S&P should have been a bit more blunt in their guidance. Offering this Plain and Simple would have helped, "DEAR CAPITOL HILL, STOP ACTING LIKE CHILDREN, YOU DO NOT REALIZE THE IMPLICATIONS OF YOUR BEHAVIOR."

RED PERSPECTIVE: Republicans are operating under the assumption that failing to announce broad-based spending cuts will lead to a catastrophic investor exodus from U.S. Treasury debt and a spike in benchmark yields (U.S. government borrowing costs) that will result in an even bigger budget deficit.

BLUE POINT OF VIEW: Democrats believe cutting too much spending at once will lead to an economic slowdown and a loss of competitive superiority in the global marketplace and a corresponding contraction of confidence in our ability to repay government debt...which would cause a spike in benchmark yields and an even bigger budget deficit.

The solution seems to be FINDING MIDDLE GROUND and avoiding the worst-case scenario. At this point I wouldn't vote for either party...I'd have to write in Batman and Robin because they are the only candidates capable of policing Gotham City.

Market Reaction...

There was an unfriendly knee-jerk reaction, but it was quick to correct itself. Bond traders called S&P's bluff.

Benchmark 10s rose rapidly through a cluster of support between 3.40 and 3.42%, but as the day progressed and bond bears failed to mount an offensive, fast$ traders were forced to cover short positions as real money accounts added new longs (duration matching now longer liabilities on the balance sheet).

10s are currently bid at 3.369%. This is where the recent rally seems to have paused for consolidation and confirmation. If this key resistance level is broken we'd look for a test of 3.31. If 3.31% is broken we'd look for a run toward 3.25%. If 3.25% is broken and MBS don't lag too badly, you should see C30 4.75% BestEx on rate sheets. Until then, 4.875% is as good as it gets.

A bear steepener is when yields in the long end are rising faster than yields in the short end of the curve. For instance, if the 10yr note yield was rising faster than the 2yr note yield, then the difference between the 2yr note yield and the 10yr note yield would be increasing...the yield spread between the 2yr note and 10yr note would be getting higher, or wider. READ MORE: Explaining Yield Spreads and the Curve

The 2s/10s curve steepened significantly when S&P's downgrade tapebombed newswires yesterday morning. That weakness corrected before the day was done though. 2s/10s are currently bid at 271bps wide. A bull flattener is needed if C30 BestExecution is to break the 4.875% barrier. (FNCL 4.5/4 swap near 280bps would help!)

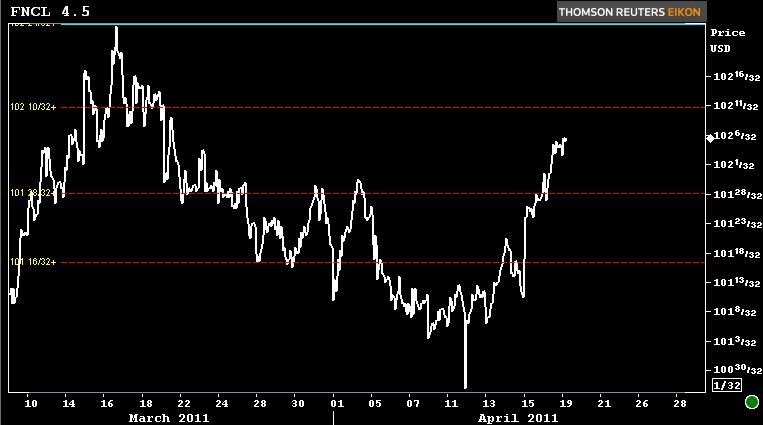

Production MBS coupons have seen little activity of late. It's been slow goings since Class A roll. Current coupon yield spread valuations have room to run in either direction. In terms of price ranges, the FNCL 4.5 faces firm overhead resistance not far ahead at 102-10. A move toward 102-25 coupled with the guidance offered above is what we need to see C30 Best Execution reach 4.75%.

Plain and Simple: The bond market shrugged off the ratings downgrade threat yesterday and continues to focus on technicals, which are shifting bullishly with today's modest rally. But investors remain wary of further ratings related tapebombs and continued political bickering. That makes the rates rally very sensitive to any reversal in technical bias! It's gonna take a strong push through the above outlined resistance levels for Best Execution mortgage rates to improve from current levels (broad-based break of 4.875% barrier). That means the incentive to float is limited at the moment....but the potential for a move lower in rates is definitely picking up some steam after yesterday's knee jerk sell-off reversal. Is it worth floating to you?

READ MORE: Budget Battle Looms. Bond Vigilantes Lurk