For a third day in a row, intraday price volatility kept mortgage rate watchers on their toes and lenders defensive. The Fannie 4.0 MBS coupon bounced around an 11/32 range and even jumped from one end to the other, twice! While this forced us to issue multiple directional warnings, only scattered reprices for the better were reported... most of which were the usual quick trigger types like Provident and FAMC.

As the benchmark 10 year note shed gains and went negative on the session this afternoon (read why below), "rate sheet influential" MBS remained relatively well-bid. Mortgages outperformed benchmarks on what we might describe as a combination of bargain buying (price and spread) as well as a little speculative "strategery". The bad news is, MBS buying occurred in light volume. There just wasn't much conviction behind the move.

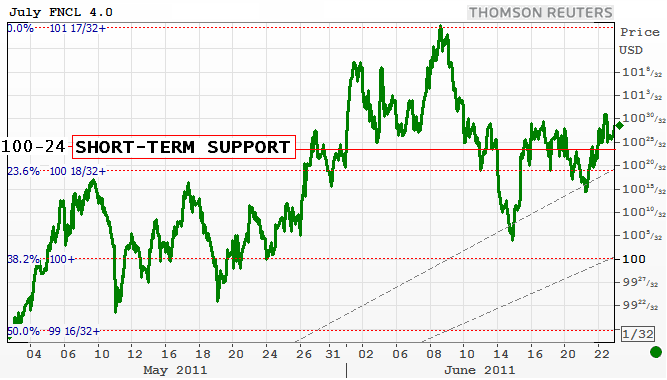

The FNCL 4.0 went out +7/32 at 100-28. Just above short-term support at 100-24...

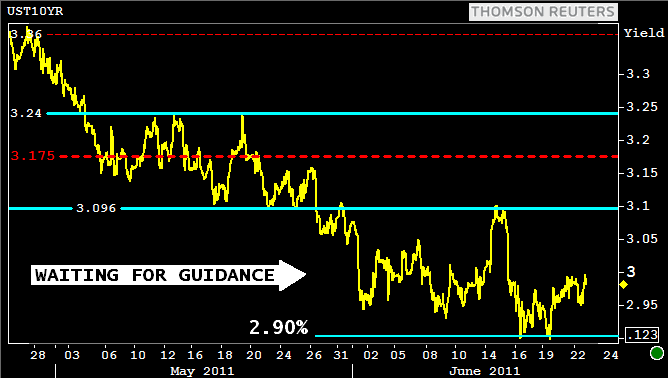

After surviving a test of 3.00% technical support, Benchmark 10s ended the day -2/32 at 101-06 yielding 2.985%. This puts us right smack in the middle of the recent trading range, where fluctuations are free to occur as long as indications remain within the confines of 2.90% and 3.10%.

While profit taking was seen today, 3.00% held up. This is encouraging....

Looking back at the past 24-hours, we've had to deal with several letdowns. The headlines we were expecting to make an impact on the markets, failed to do so.

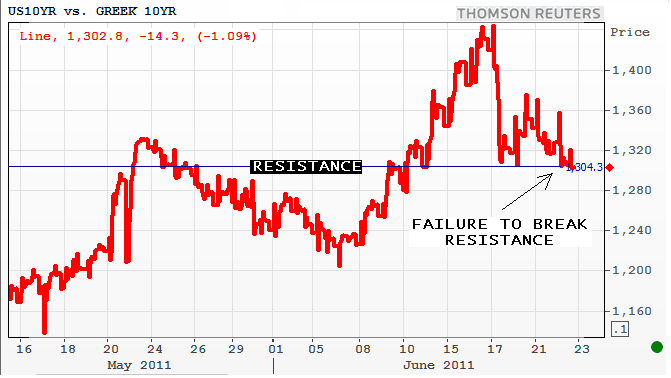

After a vote of confidence passed uneventfully last night, Greek lawmakers are now free to enact aggressive austerity measures. This should've given equity markets a boost and help tighten up European debt spreads, but it didn't. The market still believes Greece is likely to default on its debt. The spread rally between US 10yr yields and Greek 10yr yields stalled near a key resistance level. No follow through here...

Then came the FOMC today. The Fed helped confirm a slower than expected economic recovery and downgraded its forecast but also said we should anticipate a pick-up in growth during the second half of the year. The Committee continued to say rising inflationary pressures are short-term in nature and shared no hints on whether or not another Quantitative Easing package is in the works. More interestingly, Ben reminded us that the Fed is operating under a larger than normal amount of uncertainty, and that the Board will react appropriately as new developments are observed in economic data. In our view, this leaves the door wide open for anything and everything.

READ MORE: FOMC Summary Plus Bernanke Q&A Highlights

Both stock and bond markets reacted unfavorably as headline news failed to motivate new directional flows. This does not reflect a particular bias in the marketplace as much as it illustrates short-term strategery at time when the majority of investors are sitting on the sidelines waiting for new guidance (lack of liquidity). I might actually describe this behavior as investors pouting over the lack of directional guidance offered by high-profile headlines in the last 24 hours. Although there has been price volatility, it's all been contained within a range. At the end of the day it seems like we're putting up with all sorts of back and forth chopitility only to find ourselves back in the same position we started the day.

This is getting frustrating but...WE'RE STILL WAITING FOR GUIDANCE.