Inflation is always and everywhere a monetary phenomenon" - Milton Friedman

Milton Friedman's statement theorizes that the source of all inflation is a sustained period of high growth rates in the money supply. Appropriately, Friedman's hypothesis implies inflation can be prevented by consistently reducing the growth rate of money supply. The key assumption in this theory is SUSTAINED periods of high money supply growth rates. Meaning high levels of inflation can only occur if money supply is being continually increased. This theory carries weight no matter the school of economic thought you subscribe to...

Plain and Simple: The Fed has drastically increased money supply in the banking system. This expansionary policy, if continued, will ultimately lead to high levels of inflation.

This is the argument of inflation hawks and anti-Fed folk. It's hard to debate. But it makes some assumptions that tend to distort rational inflation expectations. For the most part, inflation hawks are also bullish on the economy. They assume banks will have a reason to lend money to small-businesses and consumers. They expect jobs to be created on a consistent basis, wages to rise, and household wealth to improve. They expect credit to flow.

To address the inflation hawk's bullish argument upfront. Yes we are seeing economic improvement. U.S. businesses are investing in innovation that improves productivity. Global manufacturing has rebounded quickly and boosted the domestic economic recovery in the process. Payrolls are growing steadily and jobless claims continue to fall. Measures of firms' hiring plans--have brightened a bit, raising the prospect that a pickup in the pace of hiring may be in the process. Adding fuel to the fire, stocks haven't stopped rallying since September and Consumer Confidence reports reflect it.

So the Fed's expansionary efforts must be filtering through the banking system all the way down to Main Streeters right? Not so much....

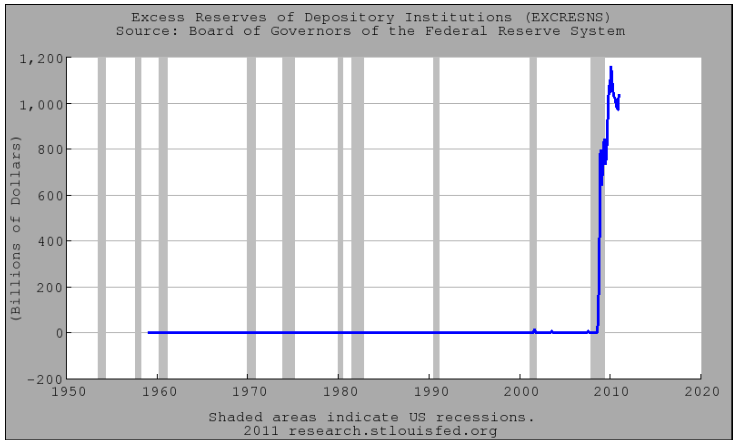

The Fed can increase the monetary base, but banks don't have to create money with new excess reserves. Banks must lend in order to create money, if they don't, Main Street doesn't benefit from the Fed's expansionary policies. As you can see in the chart below, depository institutions are holding onto a ton of excess reserves. This money is not reaching Main Street.

Money isn't being created!

Once again, perspectives of economic reality seem to be distorted.

Emerging economies are using our established production resources to build their own to compete against us. In December and January, the jobless rate was reported to have declined noticeably. That improvement wasn't organic growth. It was a factor of a falling labor participation rate. READ MORE. Still, the level of the unemployment rate remains very elevated, and the long-term unemployed continue to account for a historically large fraction of overall joblessness. Ben Bernanke threw a little more cold water on inflation hawks we he commented on the performance of the labor market in his semi-annual update to Congress this week. "The continued recovery in economic activity has been accompanied by only a slow improvement in labor market conditions. Private payroll employment has moved up at a relatively tepid rate--about 115,000 per month, on average, since the February 2010 trough in employment--recouping only a small portion of the 8-3/4 million jobs lost during 2008 and 2009. Over most of this period, the pace of hiring was insufficient to substantially reduce the unemployment rate."

What about wage growth? Here is the latest update: "Wage pressures remained minimal across all Districts; although Philadelphia, Dallas, and San Francisco noted that most wage increases were for workers with specialized skills." - Beige Book

That explains why Ben Bernanke keeps saying things like, "Consumer price inflation trended down during 2010 as slack in resource utilization restrained cost pressures while longer-term inflation expectations remained stable. Although the prices of crude oil and many industrial and agricultural commodities rose rapidly in the latter half of 2010 and the early part of 2011, overall personal consumption expenditures (PCE) prices increased at an annual rate of just 1-1/4 percent over the 12 months ending in January, which compares with a 2-1/2 percent rise during the preceding 12 months. Core PCE prices--which exclude prices for food and energy--rose 3/4 percent in the 12 months ending in January."

Government expenditures and Federal Reserve rescues supported price stability as the economy contracted. This protected us from a deflationary downspiral. But the effects of those policies are temporary. So too are tax cuts. At some point we'll need sufficient private industry job creation and wage growth to be taken off life support. Otherwise a glut of non-skilled workers will weigh on our recovery and future generations will forced to carry the socialized loss. The analogy we've used in the past is: "Like a Ford Festiva dragging a piano up a mountain ".

Main Street needs spending money. Main Street needs jobs. Main Street needs wage growth. Main Street needs banks to have a reason to lend. Main Street needs liquidity. All we're getting right now is rising commodities prices and more expensive survival costs. Wage growth is missing and job creation hasn't been sufficient enough to lower the unemployment rate. Add in high levels of productivity and one has to wonder where inflationary pressures will come from besides Wall Street and emerging economies.

Right now inflation isn't a problem. The problem is people who think inflation is the problem. That's putting the cart before the horse.....watch out for false starts. It's going to be a long, slow recovery.....

Productivity Gains Darken Hiring Outlook

Margin Squeeze Concerns Deepen as Manufacturing Sector Expands

MBS Directional Update: Compelling Cases Presented