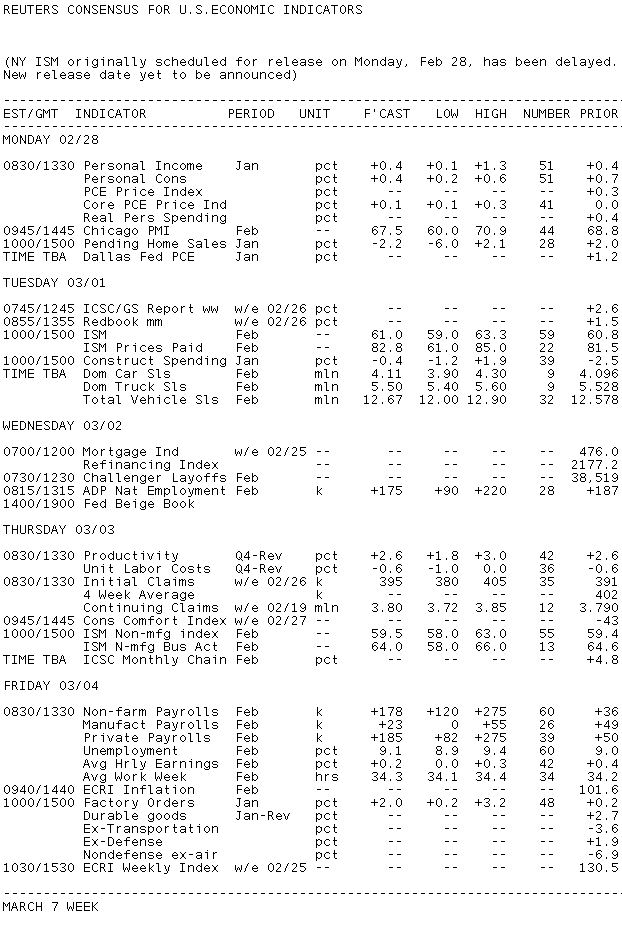

It's a busy week in terms of new economic data and events. Fed Chairman Bernanke will share his semi-annual update on the status of the economy and monetary policy. Markets remain responsive to increasing levels of unrest in the Middle East. Here at home, the White House and Congress have until the end of this week to reach agreement on a federal spending-cut bill for the rest of this fiscal year... or face a partial shutdown of the U.S. government.. Finally, the most important economic data of the week hits Friday morning in the form of the Employment Situation Report.

The February Employment Situation Report is the big ticket item on the data calendar. After three months of below expectations payroll growth, economists once again expect a healthy gain in the Establishment Survey side of the Employment Situation Report. Forecasters are calling for a 178,000 expansion in Non-Farm Payrolls. This would be the largest monthly improvement since April 2010. The other side of the report, the Household Survey, is anticipated to indicate a modest 0.1 percent jump in the Unemployment Rate from 9.0 percent to 9.1 percent. When digesting this data the market will be forced to weigh the impact of weather-related asterisks and fluctuations in the labor force participation rate against any number that comes in outside consensus estimates. Look for the markets to potentially adjust their Employment Situation Report outlooks on Wednesday after the ADP Employment Report is released. Although this data does not include government hiring and firing, it does provide a forward looking gauge of private payrolls growth. Economists see ADP registering 175,000 more private industry jobs in February.

READ MORE ABOUT THE TWO HEADED LABOR MARKET

Coming in a close 2nd behind Employment Data will be several Federal Reserve speakers with Chairman Ben Bernanke's Semi-Annual Humphrey Hawkins testimony being the market's main focus. Bernanke will update both the Congress and the Senate on the status of the economy and the expected impact of the Fed's expansionary monetary policy efforts, including QEII. Ben is not expected to shift far from recent rhetoric. The economy is growing but not at a pace fast enough to reduce the unemployment rate on a consistent basis. He will likely point toward rising commodity prices as a source of short-term inflationary pressures but continue to say that core nflationary expectations remain well-grounded in the U.S. because of weak wage growth, a stagnate housing market, and insufficient job creation. It is unlikely that Bernanke will hint at an early end to the Fed's latest Quantitative Easing efforts. READ MORE ABOUT THE FED'S OUTLOOK

Chairman Bernanke isn't the only member of the Fed to share insight in the week ahead though. We have speakers scheduled to share perspective every day this week. Furthermore, the Fed will release the Beige Book which is a compilation of anecdotal information and data on current economic conditions across the country. They call it the Beige Book because its Beige. The findings are NOT THE VIEWS OF FEDERAL RESERVE OFFICIALS...instead, each Federal Reserve bank interviews key business contacts, economists, market experts, and other sources in their specific district. This report is published eight times a year.

Monday

8:30 - Federal Reserve Bank of New York President William Dudley speaks on "The Economic Outlook for 2011-12" at an event hosted by the New York University Stern School of Business. Audience Q&A expected.

8:45 - Federal Reserve Bank of Boston President Eric Rosengren participates in "Lessons Learned from the Global Meltdown" panel. Audience Q&A expected. Media Q&A unlikely.

Tuesday

10:00 - Federal Reserve Chairman Ben Bernanke delivers semiannual monetary policy testimony before the Senate Banking Committee

Wednesday

8:00 - Federal Reserve Bank of Kansas City President Thomas Hoenig speaks before the Council on Foreign Relations. Q&A TBA.

10:00 - Federal Reserve Chairman Ben Bernanke delivers semiannual monetary policy testimony before the House Financial Services Committee.

2:15 - Federal Reserve Bank of Atlanta President Dennis Lockhart participates in a question-and-answer session on the economy and monetary policy with Allan Maurer, editor of Tech Journal South, before the Southeast Venture Conference. Audience Q&A expected. No media Q&A.

8:00pm - Federal Reserve Chairman Ben Bernanke speaks on "Challenges for State and Local Governments" before the Citizens Budget Commission Annual Dinner. No Q&A.

Thursday

10:00 - Federal Reserve Bank of Minneapolis President Narayana Kocherlakota speaks on "Labor Markets and Monetary Policy" before the St. Cloud State University Winter Institute. Audience Q&A, slides expected. Media Q&A follow.

12:15 - Federal Reserve Bank of Atlanta President Dennis Lockhart speaks on "The Economy and Labor" before the Economic Club of Florida. Audience and media Q&As expected.

Friday

10:00 -Federal Reserve Vice Chair Janet Yellen participates in "Improving the International Monetary and Financial System" panel before the International Symposium of the Banque de France. Audience Q&A expected.

Here is a more detailed look at the economic calendar in the day's ahead....

In terms of the bond market and mortgages. This is the guidance we offered on Friday.

MBS Directional Update: Compelling Cases Presented

Last Tuesday we issued a directional MBS alert because the bond market seemed to be in the midst of shift in its underlying technical bias, from bearish to bullish.

We

cited several different motivations for the recent turn around in

benchmark Treasury yields, production MBS coupon prices, and mortgage

rates, but the headline grabbing explanation for the move was the actual

headlines themselves. We explained it to consumers as so....

"Conflict in Libya and the potential for a spill over into other oil

producing countries has energy traders nervous about shrinking oil

inventories. The chance for a supply/demand driven spike in energy

prices is seen as a threat to the already sensitive U.S. economic

recovery. Many economists believe rising energy costs would squeeze

disposable income on Main Street and hurt consumer spending, which would

slow the economic recovery. This 'headline risk' had led stock prices

lower and pushed money into safe haven assets like U.S. Treasuries."

To

another audience, we might say the "flight to safety" caught a nervous

short-base off-guard, which ultimately led to a momentum driven short

squeeze aka a hint of "snowball buying" and a very modest shift in the

real$ investor's par coupon /duration bias. Remember coupon rate

dictates par price in the bond market, at a specific spot on the yield

curve. The par coupon rate in 10s right now is 3.625%. 10 year yields

are below 3.625%, so on the run Treasuries are trading at a premium

(101-24).

Looking past the technicalities of the secondary mortgage market, the

obvious explanation for this week's rally was a "flight to safety" into

government bonds. And everyone wants to know if it's gonna continue.

We can spin it however you want to hear it.

Emerging economies

are using our established production resources to build their own. U.S.

businesses are investing in innovation that improves productivity.

Global manufacturing has rebounded quickly and boosted the domestic

economic recovery in the process. Payrolls are growing steadily and

jobless claims continue to fall. Adding fuel to the fire, stocks

haven't stopped rallying since September and Consumer Confidence

reports reflect it.

But then we come to Main Street. One might

say the misery index is high on Main Street. Many folks are still

battling suffocating debt payments. Some are working two jobs just to

stay afloat. Others can't even find one. Fuel prices are getting more

expensive and the cost to heat a home is rising . All the while, wage

growth is lacking and demand pull inflation is missing. It's one big

margin squeeze for the average American. But the wealthy seem to be

doing dandy. (They've even begun dabbling in the housing market.)

Notice

I didn't even mention the mess that has become the U.S. housing

market... It's stagnating in a pool of its own filth. No one person in

this industry knows what's coming next. We're a mess. Originators are

totally focused on interpreting the 500 or so variations of new

compensation reforms, but are totally missing the risk retention issue.

This change will most likely push consumer borrowing costs higher more

than any other pending reform, including whatever pain is inflicted by

the GSEs and the updated loan servicing model. Making matters worse,

there is no unified voice of common sense coming from the trenches. MBA,

NAMB, NAIHP. All sending different messages to industry regulators.

Loan producers, processors, underwriters, closers, shippers, secondary,

appraisers....all need one unified voice! We're living in a reactive

world, being proactive is like playing pin the tail on the donkey.

See. We can paint two very compelling pictures here. That means the best we can do is view the situation in its present form. We're still in the midst of a flight to safety. The yield curve has flattened. Technical momentum is leaning in our favor. And we're ending the week just below our 3.42% target in 10s and 101-28 target in FNCL 4.5s. Plus it doesn't sound like conflict is close to being resolved in Libya. Tensions are mounting across the Middle Eastern Arab Nations. This investing environment reminds me more and more of the first few months of 2010. It's like we're repeating history...

All signs of encouragement for an extension of the recent rally. But there is something more important that must be called to attention: The Best Execution 30 year fixed mortgage rate has hit a short-term floor.

On Thursday we announced that the "Best Execution" 30 year fixed mortgage rate had fallen to 4.875%. This takes us back to where we spent most of January. Remember the range? If you remember the range you should also remember the steep drop-off in loan pricing between 4.875% and 4.75%. There were a few days where the 4.75 float down made sense but for the most part, 4.875% at 0+0 was the best quote on C30 rate sheets. We've re-entered that range again. And it's going to take another 20-30bps move lower in benchmark 10yr yields before 4.625% is an attractive buydown again. We'll need to see FNCL/GNMA 4.0s trading over 100-15. Do you have the time to wait for it? LOAN PRICING EXAMPLE

Our guidance does not change. Same as Tuesday...

Plain and Simple: We are cautiously optimistic about lower mortgage

rates in the months ahead but remain quite defensive of the modest loan

pricing improvements that have been awarded since last Friday. This is

only a directional alert. We are in the midst of a potential reversal,

the move is still immature. More positive progress is needed to confirm a

shift in technical bias.

Over the next week you are floating for rebate improvements. We do not

expect another move lower in the Best Execution 30 year fixed mortgage

rate by the end of this week. In fact we wouldn't be surprised to see some push back against the recent rally in the bond market.

Short sellers and profit takers will not give us easily. If losing a

4.875% BestEx quote is not something you're prepared to deal with...GUTFLOP GUTFLOP GUTFLOP

CHECK OUT OUR TECHNICAL TARGETS IN THIS POST <----MUST READ. FOLLOW THE EMBEDDED LINKS

ps....CAN YOU IMAGINE IF IRAQ TAKES A TURN FOR THE WORSE? WOULD WE RE-DEPLOY TROOPS OR LET ALL THAT HARD WORK UNFOLD? Budget builders won't be too excited about more war.

pps...just reading the Plain and Simple doesn't provide the proper prospective!