We are seeing current coupon MBS yield spreads tighten as benchmark TSYs approach their best levels of the day.

"Higher and Tighter" is not normal behavior for production MBS coupons and it suggests focused demand is giving "rate sheet influential" MBS an extra boost. Based on recent price action and the generally unchanged shape of the yield curve, we'd assume this additional strength is coming from fast money day traders as opposed to duration sensitive real money buyers.

Loan originators probably just read that as "blah blah blah TSYs best level of day yada yada yada MBS focused strength" and wondered what it meant for loan pricing. It means MBS and TSYs are near their best levels of the day and reprices for the better have been widely reported. The stock lever can be cited as a source of strength in the meandering move lower made by benchmarks in the lunchtime hours.

Don't get too excited though. Reprices for the better have restored 10-15bps in rebate, but loan pricing is still 15.8bps worse than it was yesterday, on average.

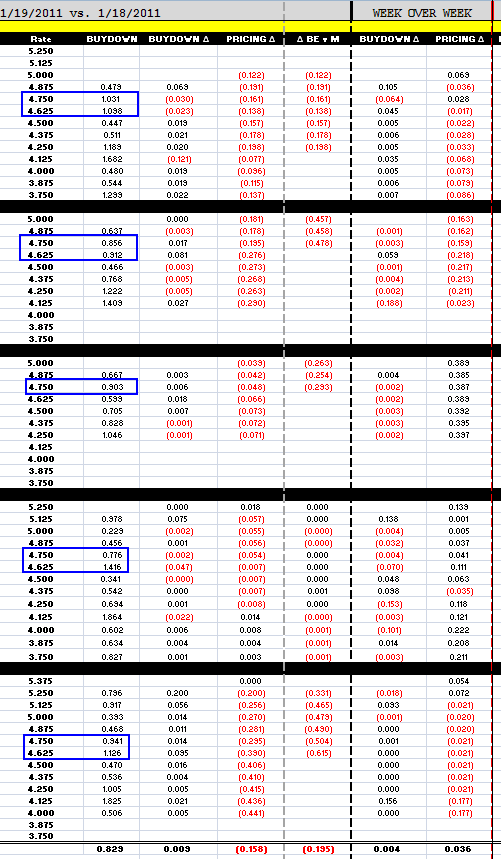

Since we're on the topic of loan pricing, check out the permanent buydown costs from 4.875 to 4.75% to 4.625%. I'm sure you've noticed this already and wondered why the buydown was so expensive. Well it is a function of liquidity in the TBA MBS market. 4.0 coupons are not trading! And until lenders start hedging with 4.0 coupons, there will be a clear line of demarcation between 4.75% and 4.875%. Why? Well because 4.00 trades are generally filled with 4.375% to 4.75% paper. 4.50 MBS coupons are generally filled with 4.875% to 5.25% note rates.

4.50s are the production coupon of choice for hedgers at the moment and 4.0s are still illiquid, making 4.75% quotes generally expensive to borrowers who do not intend to hold their mortgage for at least 10 years.

Trading volumes in the belly of curve are below average and there is a general feeling of apathy directing traffic. The stock lever has been a source of strength today, thus we must assume it might also become a source of weakness. BEWARE OF A BOUNCE IN EQUITIES.