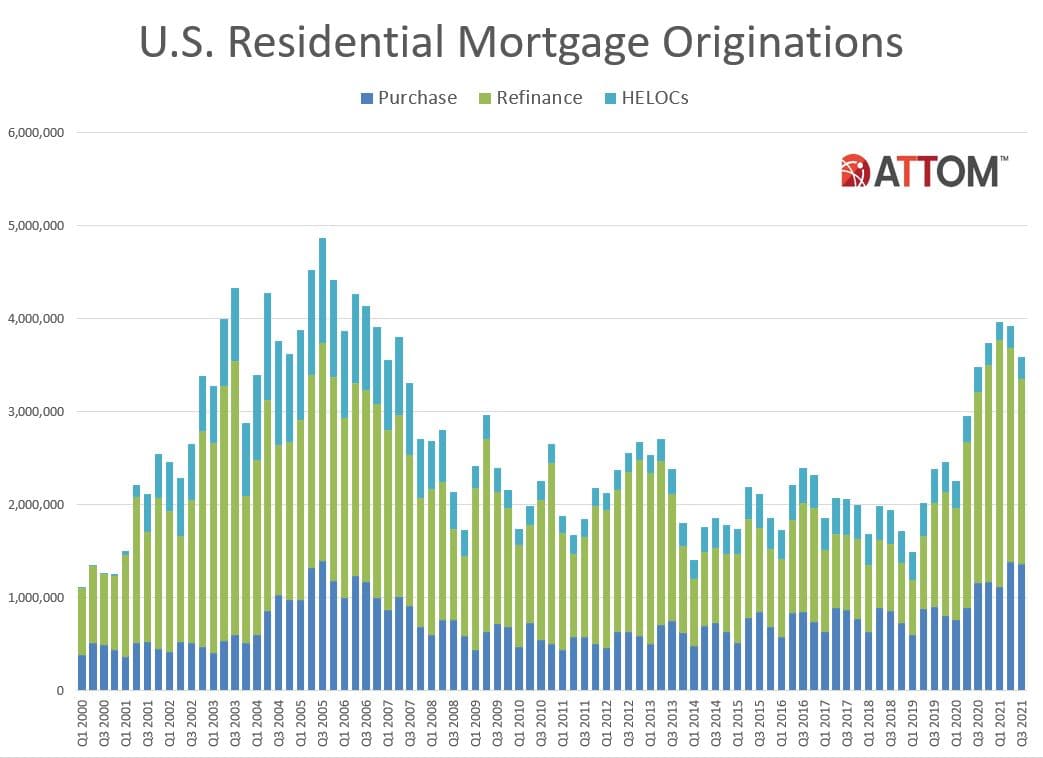

A new report from ATTOM says that the number of mortgage originations dropped sharply in the third quarter. The company says there were 3.59 million residential mortgages originated during that period, a 3,2 percent increase over the 3.48 million during the same quarter in 2020, but an 8.4 percent decline from the 3.92 million originations in the second quarter of 2012, the largest quarterly dip in more than a year.

The quarter-over-quarter slide followed another in Q2 and marked the first time in more than two years that total lending decreased in two consecutive quarters. It was also the first time in any year since at least 2000 that total lending activity went down from both the first to the second quarter and from the second to the third quarter of any year, usually are peak homebuying seasons. The two-quarter decline hit both refinancing and purchase lending, masking an increase in home-equity lines of credit (HELOCs).

By dollar volume, lenders issued $1.15 trillion worth of mortgages during in the third quarter, a period when 30-year fixed-rates remained below 3 percent. That volume was up 10.7 percent year-over-year (from $1.04 trillion) but was down quarterly by 6 percent from $1.23 trillion in the second quarter, the first quarterly decline since early 2020.

Homeowners refinanced just shy of 2 million homes during the quarter, a 13 percent decline from the prior period and down 3 percent from a year earlier. In addition to being the second straight decrease, it was the largest in three years. The dollar volume of refinance loans was down 10 percent from the second quarter of 2021, to $624.1 billion, although still up annually by 1 percent. While refinancing accounted for the largest share of lending, that share dropped from 59 percent in both the previous quarter and a year earlier to 55 percent in Q3.

The number of purchase loans dropped 2 percent from Q2 to 1.36 million units. This, however, was still a year-over-year gain of 17 percent. The dollar volume dipped 1 percent to $482.6 billion compared to Q2 but was 30 percent higher than the third quarter of 2020.

Home-equity lending, meanwhile, rose for the second straight quarter, which last happened in mid-2019. The tally of home-equity lines of credit, while down annually by 9 percent, rose 2 percent between the second and third quarters of 2021, to about 238,500. The $46 billion third-quarter volume of these loans, though, was still down 0.8 percent from the second quarter and 15 percent lower than in the third quarter of 2020.

ATTOM said the decline in lending might or might not mean the decade-long housing boom is cooling off, but at a minimum it has reversed patterns seen from early 2019 through early 2021, when total lending activity nearly tripled amid various forces including record low interest rates and a pandemic that spurred a surge in homebuying which, in turn, has driven home prices to record highs.

"The overflow stack of work that was hitting lenders for several years shrank again in the third quarter across the U.S. amid a few emerging trends," said Todd Teta, chief product officer at ATTOM. "It looks more and more like homeowner's voracious appetites for refinance deals has eased notably, while purchase lending also dipped. It's still too early to say if the trends point to major shifts in lending patterns or the broader housing market boom. But the drop-off is significant, especially for home buying, which could suggest an impending housing market slowdown. We will be watching the lending trends extra closely in the coming months."

Overall lending activity decreased from the second quarter of 2021 to the third quarter of 2021 in 186, or 86 percent, of the 216 metropolitan statistical areas around the country with a population greater than 200,000 and at least 1,000 total loans in the third quarter.