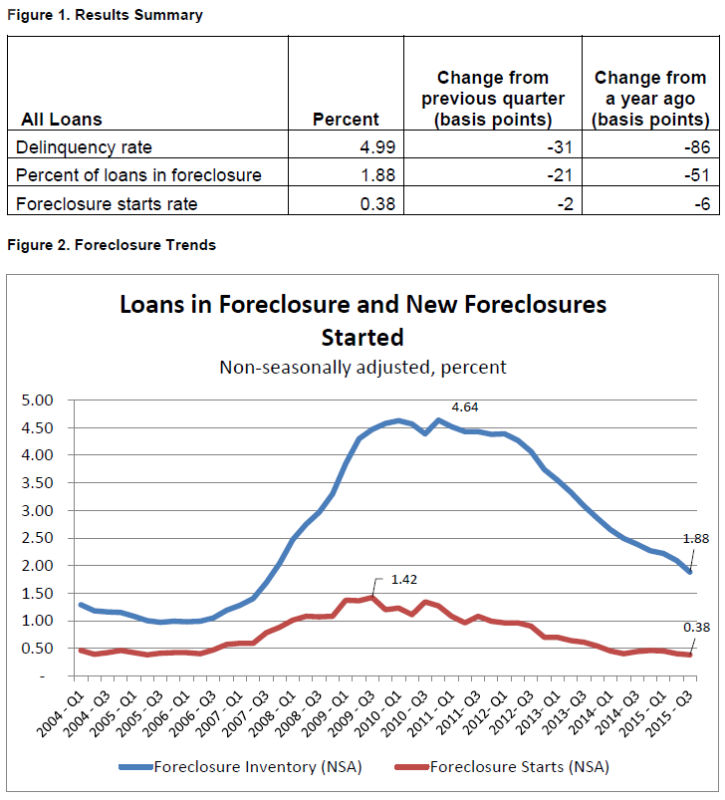

Measures of mortgage distress continued to reach new eight to ten year lows during the third quarter of 2015. The Mortgage Bankers Association's (MBA's) National Delinquency Survey showed substantial improvement in the delinquency rate, and the foreclosure inventory.

MBA said that 4.99 percent of all one-to-four unit residential mortgage loans outstanding at the end of the quarter had missed at least one payment, the lowest rate since the first quarter of 2007. An additional 1.88 percent were in some stage of foreclosure, i.e. the foreclosure inventory. The delinquency rate was down 31 basis points (bps) from the second quarter and 86 bps from the third quarter of 2014. The foreclosure inventory was 21 bps lower than the previous quarter and 51 points below the rate a year earlier. It was the lowest level for the inventory since the third quarter of 2007.

Serious delinquencies, loans more than 90 days past due on in foreclosure represented 3.57 percent of active mortgage loans a decrease of 38 and 108 bps respectively from the previous quarter and year and also the lowest rate since Q3 2007. Foreclosure starts were down as well but much more modestly from the two earlier period - 2 and 6 bps respectively. Still, starts were at the lowest level in ten years.

Marina Walsh, MBA's Vice President of Industry Analysis, said, "Overall delinquency rates and the percentage of loans in foreclosure continued to fall in the third quarter and are at their lowest levels since the first quarter of 2007. The serious delinquency rate - measured by those loans that are 90 days or more delinquent or in the process of foreclosure - declined for nearly every state in the nation. The factors influencing this outcome include a nationwide housing market recovery, resolution of long-standing troubled loans that eventually proceeded through the foreclosure process, and an improving employment outlook that provided distressed borrowers viable alternatives to foreclosure.

Walsh noted that the delinquency rate for FHA loans overall declined 10 bps to 8.91 percent on a quarterly basis and seriously delinquent loans were down by 20 bps. Early delinquencies, i.e. 30 day, increased 11 bps. In addition, the FHA foreclosure inventory rate dropped to 2.65 percent in the third quarter, from 2.68 percent in the second quarter and 2.73 percent a year ago.

"While only 40 percent of loans serviced are in judicial states, these states account for a majority of loans in foreclosure, Walsh said. "For states where the judicial process is more frequently used, 3.01 percent of loans serviced were in the foreclosure process, compared to 1.06 percent in non-judicial states. States that utilize both judicial and non-judicial foreclosure processes had a foreclosure inventory rate closer that of the non-judicial states at 1.26 percent.

Three judicial states, New Jersey, New York, and Florida continued to have the highest percentage of loans in foreclosure. The three have topped all other states in this regard since the fourth quarter of 2012 but New Jersey's high rate, 6.47 percent, was down by 84 bps, the nation's largest quarterly decrease. New York's inventory rate, 4.77 percent in the third quarter also was the result of a significant decline, falling from 5.31 percent in Q2. Florida's inventory fell from 4.24 percent to 3.46 percent.

"Legacy loans continued to account for the majority of all troubled mortgages," Walsh said. "Across all loans, 80 percent of the loans that were seriously delinquent were originated before the year 2009, even as the overall rate of serious delinquencies for those cohorts decreased."