Earlier this year, after solid price increases nationally (11 percent in 2013 alone) and near meteoric gains in some markets, speculation began about another housing "bubble." Memories of the chaos that followed the last bubble were still very fresh - ongoing in fact - so the prospect of a repeat was a little scary.

In May 2014 CoreLogic announced a new measure it had added to its Home Price Index (HPI) data and HPI Forecasts. The Market Condition Indicator is intended to assess whether individual markets are undervalued, priced at their actual value, or overvalued by looking at home prices in light of the long-run sustainable levels that can be supported by local market fundamentals such as disposable income. An undervalued or overvalued market was defined as one having a current HPI 10 percent above or below the long-term fundamental value. . CoreLogic looked at long-term fundamental values for 300 Core Based Statistical Areas (CBSAs) based on real disposable income per capital and then calculated the gap between actual or forecasted home prices and their long-run sustainable levels.

Home prices have continued their significant recovery into 2014. Even though the double digit annual price increases have moderated after a more than 20 month streak, CoreLogic's year-over-year HPI including distressed sales was still up 6.5 percent in August. Because this trend has bolstered talk of a housing bubble CoreLogic's principal economist Mark Liu decided it was time to take another look at home prices beyond simple price appreciation.

In a recent article in the company's Insights blog Liu talked a little more about the Market Condition Indicators and whether or not a bubble is still a concern. Most homeowners use their income to pay their mortgage, Liu says, so there is an established relationship between income levels and home prices. "In the long run home price growth cannot be sustained above income growth because housing would become unaffordable, demand would decline and home price growth would either slow or decline to realign with income levels."

The figure above shows national home prices and the population weighted averages between home prices and their long-run sustainable levels in the 50 largest markets. The figure clearly shows the run up in the bubble as prices between January 2005 and November 2007 rose more than 10 percent above sustainable levels; closer to 20 percent at the absolute peak. Then prices collapsed, falling quickly to levels of less than 10 percent below sustainable levels, nearing -15 percent in mid-2012.

Since then, as house prices continued to rise, the gap narrowed to 6 percent below the long-run sustainable level by August 2014, and is forecast to shrink further to just 3 percent by the end of 2016. Any bubble on the national front is clearly a ways away.

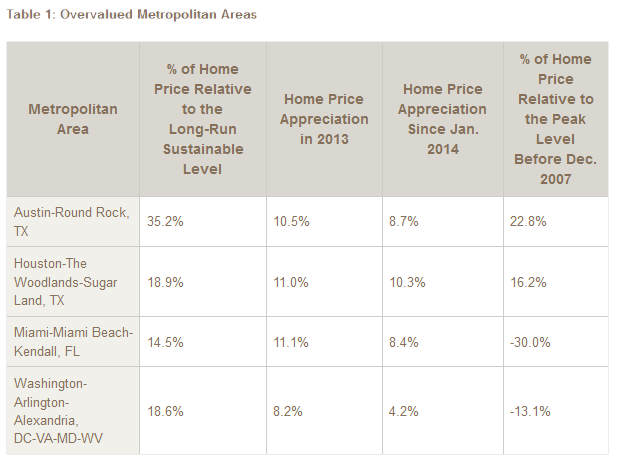

However there are CBSAs that are already in bubble territory. Table 1 shows the four overvalued markets of the top 50 CBSAs. In Austin and Houston the energy boom has fuel job and population growth and pushed home prices well above sustainable levels, in fact well above the peaks they established before the recession. Austin is 22.8 percent above its peak and Houston 16.2 percent. The other two most overvalued metros are Miami, Fla. and Washington, D.C. As home prices have risen significantly since 2013, homes have become less affordable in these two markets, and therefore, prices are less sustainable. Both however remain below their previous peaks.

At the other end of the spectrum, Pittsburgh is the most undervalued metro. The city escaped the worse of the housing downturn and now, although its home price level is about 14.7 percent more than the peak level prior to the recovery, the disposal income per capita in Pittsburgh has risen even faster at 21.1 percent. These leaves Pittsburgh with a 25 percent gap relative to the sustainable home price level. In the other three cities featured in Table 2 home prices remain significantly below their historical peak levels, in spite of strong recovery in housing markets and rapid increases in disposal income.

The bottom line, Liu says, is that the CoreLogic Market Condition Indicators show there is no bubble yet. Despite the significant growth in home prices since they hit bottom a little more than two years ago most markets are still well within their sustainable levels and most are still only recovering from the market collapse.