Mortgage lenders may be missing out on an opportunity to offer consumers something they are asking for - a wider use of mobile technology in the mortgage process. Fannie Mae says its National Housing Survey (NHS) has shown a desire on the part of consumers to shop and apply for a mortgage via their mobile devices. At the same time the company's Mortgage Lender Sentiment Survey (MLSS) indicates that lenders still favor more traditional channels such as using loan officers, brick and mortar branches, and third party partnerships.

Steve Deggendorf, Fannie Mae's Director of Business Strategy, writes in the FM Commentary blog that mobile devices are increasing used for a variety of financial transactions including bill payments and banking but are less common in the mortgage space. He says the lower priority that lenders are placing on mobile channels and the differences between lenders and consumers in how they view the subject "could place lenders at risk of not meeting consumer demand or encouraging new entrants to address this growing demand at the expense of existing firms." Lenders need to get the right mix of traditional, on-line, and mobile channels and tools

Responses to the NHS indicate that homebuyers are increasingly going online to get their mortgages, using both personal computer and newer mobile-based technologies. The data suggest that consumers' desire to shop and apply for a mortgage via a mobile device in the future is more than twice the current usage.

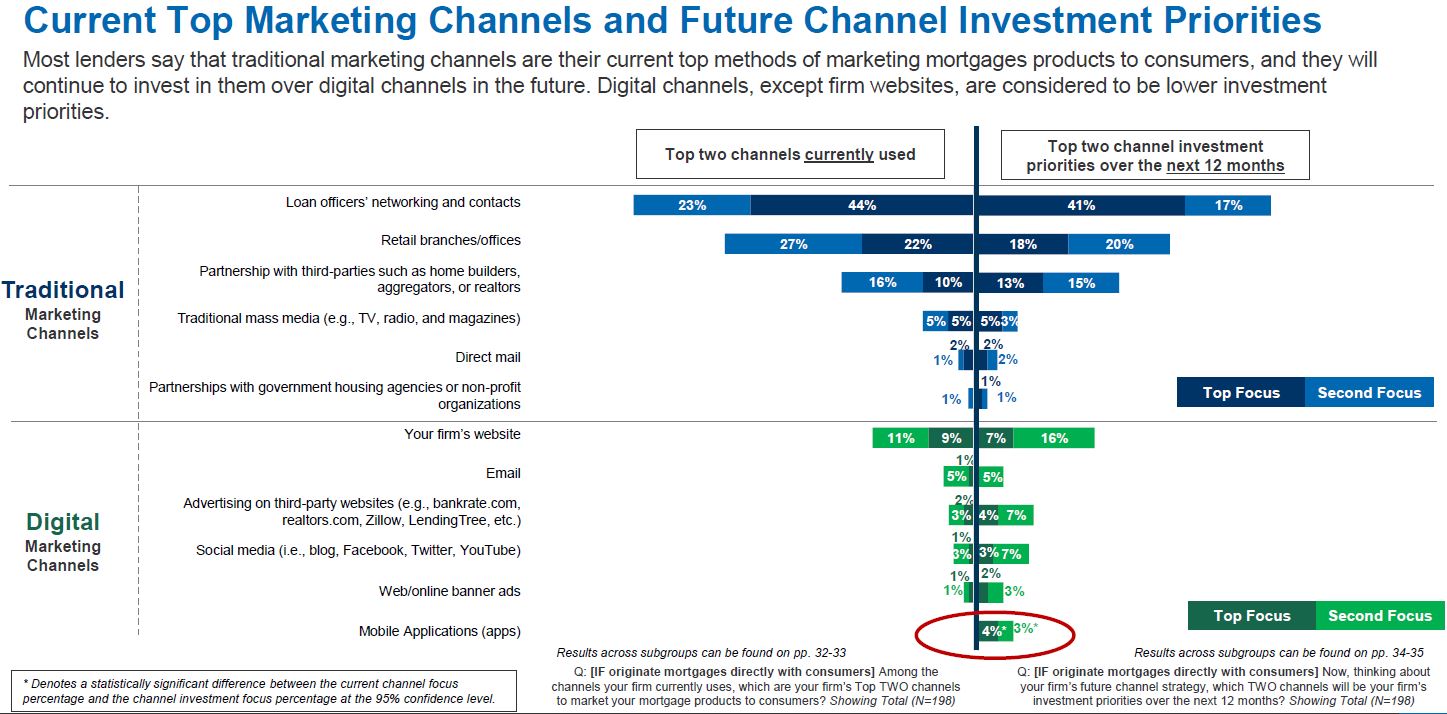

In MLSS responses, only about 25 percent of lenders said they offer a mobile app that enables consumers to shop for a home or obtain a mortgage. While the combination used by most combines traditional and digital marketing, mobile apps are used much less often and lenders also say they will continue to emphasize investment in traditional over digital, and especially mobile, channels in the future.

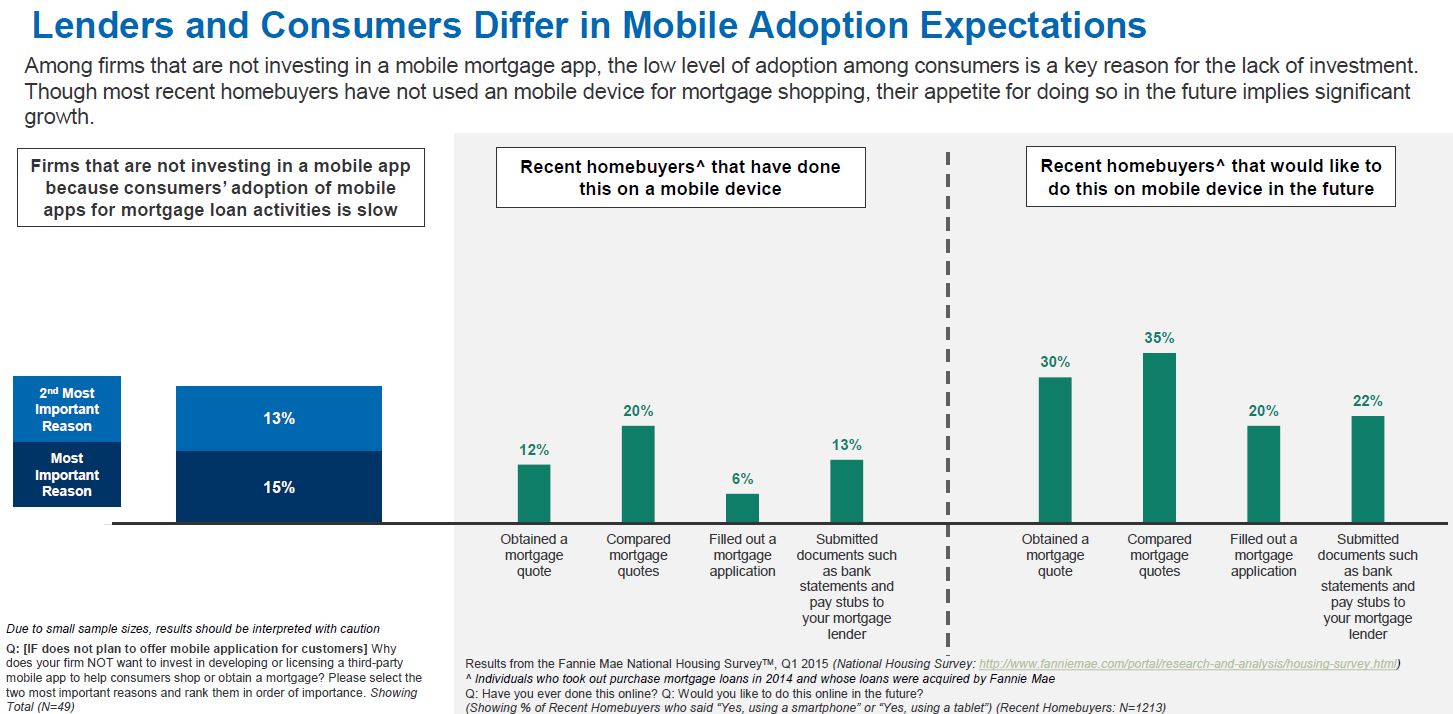

Forty percent of those who don't currently offer an app do plan to develop one over the next 12 months. Of the remainder, one third cite the high cost of development, information security risks, compliance issues, and slow consumer adoption as reasons for not moving forward. Another quarter of lenders who are not up on mobile platforms do not know or are unsure of their next steps in that direction.

But Deggendorf, says lenders may be underestimating consumer appetite for a mobile application and the rate at which they will adopt the technology. Results from the NHS show that, although only 12 percent of recent homebuyers say they have used mobile devices to get a mortgage quote and 6 percent to fill out a mortgage application, 30 percent and 20 percent, respectively, say they would like to use a mobile device in the future to perform these mortgage activities.

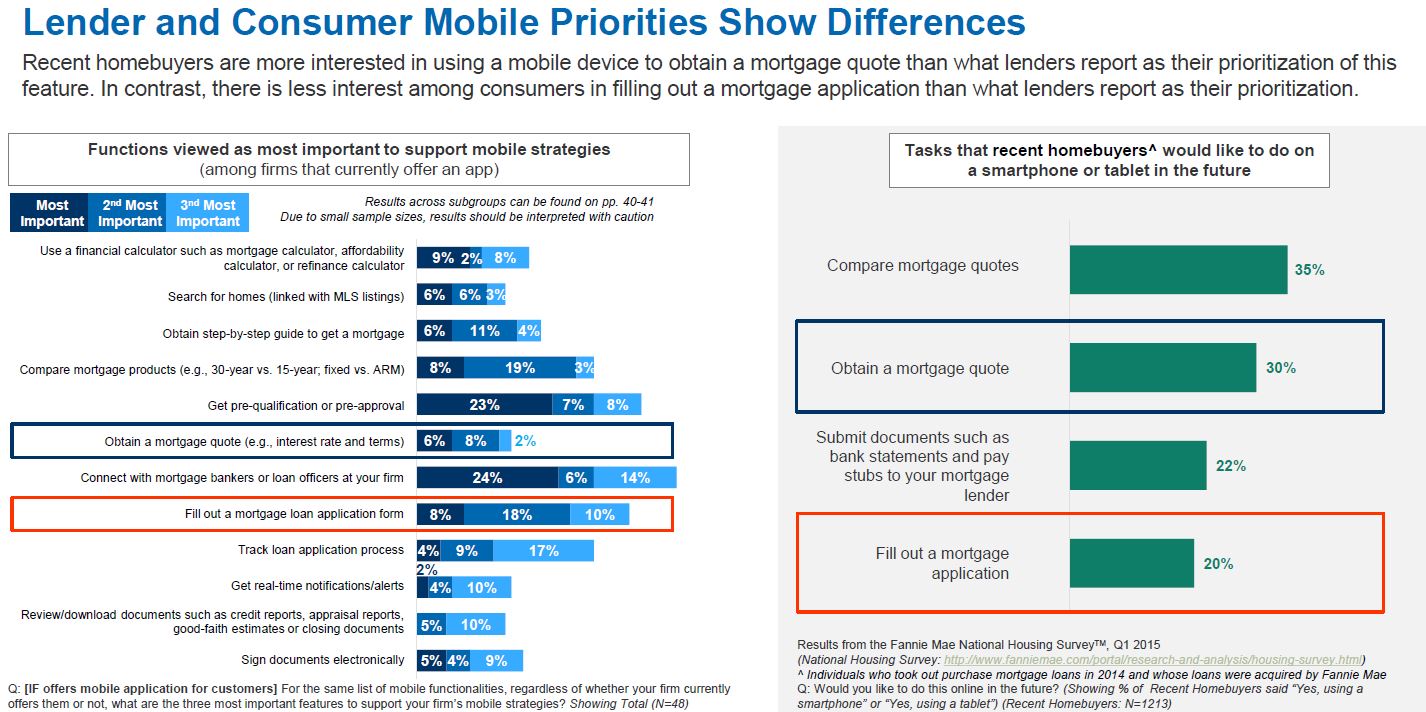

In addition, consumers and lenders appear to differ on the mortgage processes they would like to access on their mobile devices. Lenders, whether with or without a current mobile application, say the most important mobile functions include allowing consumers to get pre-qualification, connect with loan officers, fill out application forms, and track the application process. Consumers however are more interested in using mobile devices to obtain a mortgage quote, giving this functionality a much greater priority than lenders do. Consumers also are less interested in using mobile devices to fill out a mortgage application than lenders appear to be in providing that ability.

Lenders and consumers do agree on one concern - security. Almost one-third of lenders cites those risks as the primary reason for not developing an app and over half of recent homebuyers say they would worry about it in applying for and closing a mortgage online.

Deggendorf, says Fannie Mae's research shows that there is still an important role for face-to-face contact. Many consumers want the ability to speak to an expert and some point in the mortgage shopping process. At the same time, mortgage lenders need to determine an appropriate mix of traditional, online, and mobile mortgage access. The NHS consumer study, Consumer Attitudes about Getting a Mortgage Online and via Mobile Technology, found that those consumers with a college education, higher income, and younger age drive the use of online and mobile tools in mortgage shopping among recent borrowers. Deggendorf says this data may be helpful to those considering enhancing their mix of tradition and technology for their market segments.