Freddie Mac's Economic and Housing Research Group said on Monday that the U.S. economy and job market are firing on nearly all cylinders, "but the housing market has essentially stalled." The solid growth of the U.S. economy during the second quarter, an increase of 4.2 percent and exceeding forecasts of 4.1 percent, was the fastest in nearly four years. Solid consumer spending and business investment, the Group says in its September Forecast, should keep the economy on a very strong growth path of 3.0 percent this year, moderating to 2.4 percent next year.

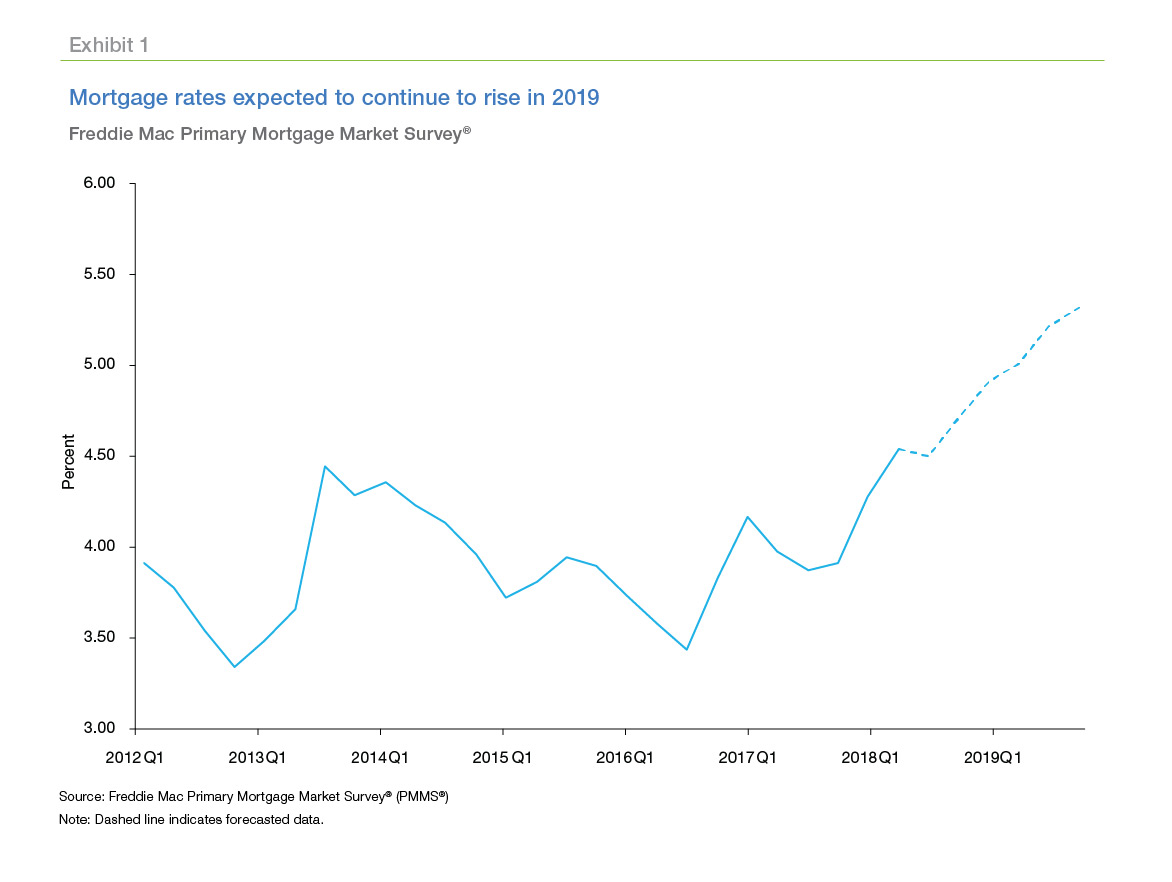

However, weaker affordability, homebuilder constraints, and ongoing supply and demand imbalances over the summer resulted in fewer home sales and less home construction compared to earlier in the year. Those sales declined in the second quarter, typically the strongest period of the year, and showed further weakness at the beginning of the third quarter. July home sales, new and existing, were down for the fourth consecutive month to an annualized rate of 5.97 million units. New home construction also lost momentum in the second quarter, falling 4.5 percent from the first quarter.

Even though inventory conditions have improved marginally, and home price pressures have begun to lessen, Freddie expects sales this year to come in below those in 2017. They are projecting total sales, both new and existing homes, to nudge down by 0.9 percent, from 6.12 million in 2017 to 6.07 by the end of this year. Sales will rebound in 2019, rising 1.8 percent to 6.18 million units. Housing starts are now forecast to rise 7.5 percent this year and 4.7 percent in 2019.

"The spring and summer home buying and selling season ultimately ended up being a letdown, despite a faster growing economy and healthy demand for buying a home," said Freddie Mac Chief Economist Sam Khater. "Unfortunately, too many would-be buyers continue to be tripped up by not enough affordable supply and the one-two punch of much higher home prices and mortgage rates."

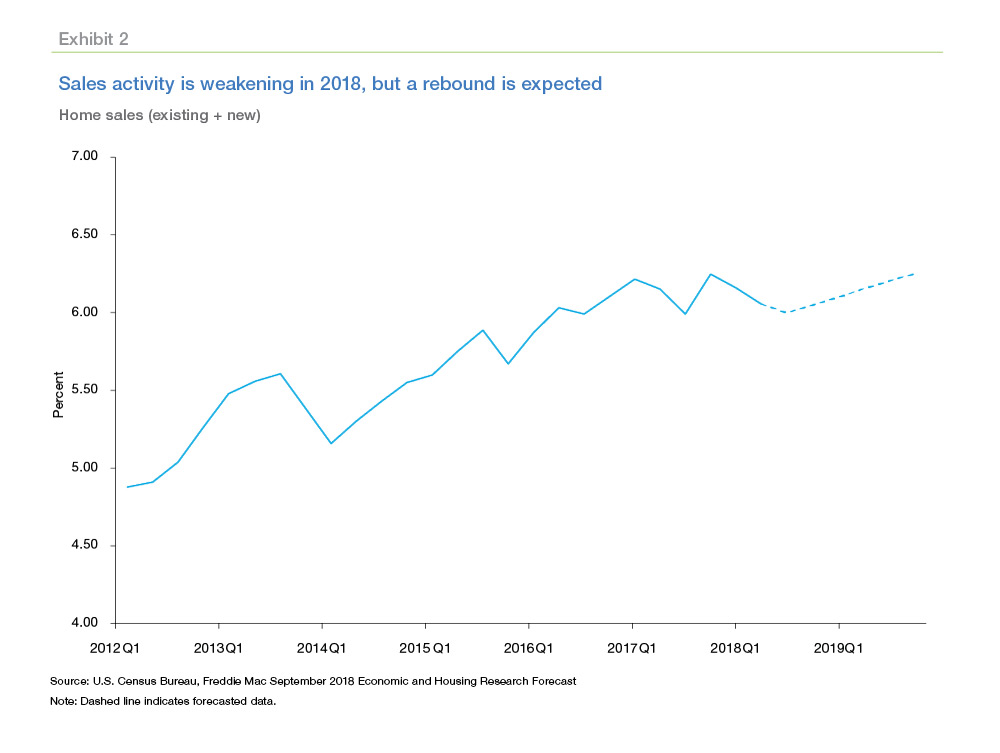

Home prices grew at a slower pace in the second quarter. The Freddie Mac House Price Index (FMHPI) increased 0.9 percent compared to 2.1 percent in the first quarter. Prices are expected to moderate going forward, ending the year with an average appreciation of 5.5 percent, still exceeding the rate of inflation, and 4.5 percent next year. Any easing of prices however will be in the face of rising interest rates. Those rates actually inched backward over the summer, but most have started to trend higher again in recent weeks. Freddie Mac expects the 30-year fixed-rate will average 4.5 percent this year and 5.1 percent in 2019.

Khater added, "Prospective buyers are being squeezed the most where demand is the strongest: the entry-level portion of the market. While price appreciation is welcomingly starting to ease in many markets, weakening affordability continues to hamper overall activity."

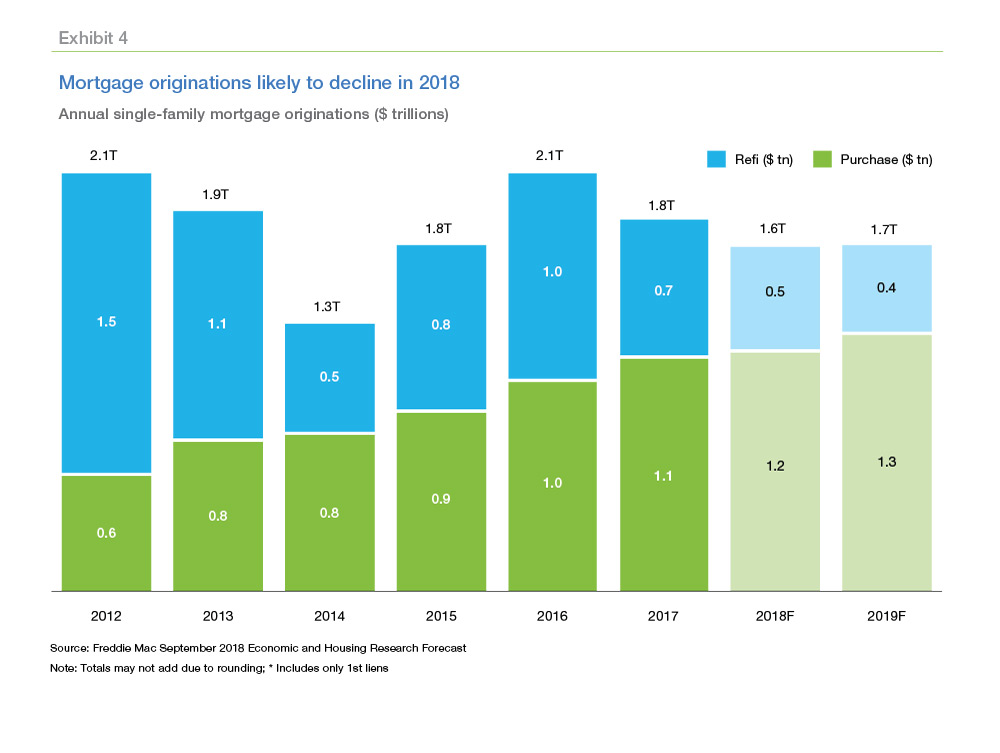

Between the impact of higher rates on refinancing and decreasing home sales, the Group expects single-family first-lien mortgage originations to slide 8.9 percent this year to $1.65 trillion.

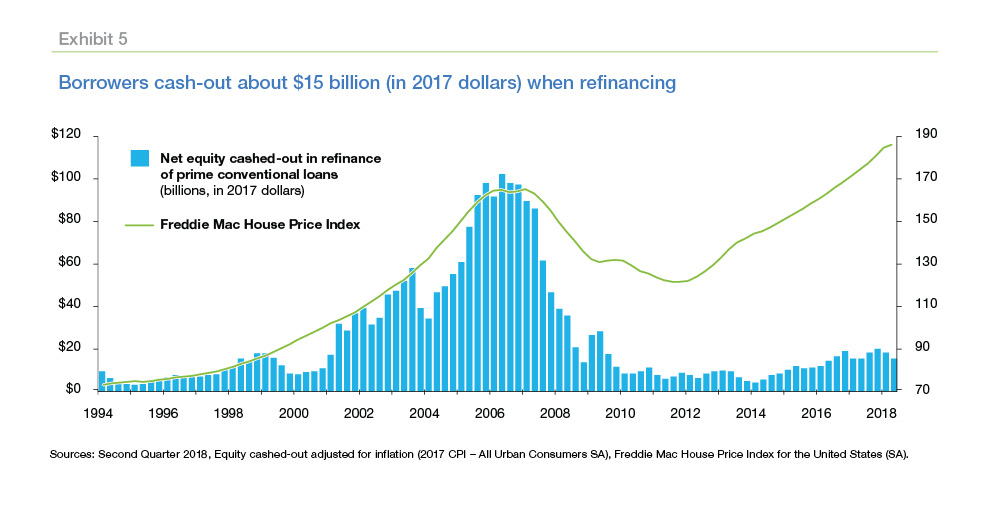

The September Forecast also contains statistics on second quarter refinancing activity. Freddie Mac says the share of those refinances that were cash-out was the highest since the third quarter of 2008. Seventy-seven percent of refinance loans were at least 5 percent larger than the loans they replaced, up from a 57 percent share a year earlier. Even as the number of cash-out refinances increases, homeowners are not cashing-out the equity in their homes the way they did in 2005 and 2006, the peak years for equity extraction that preceded the housing crisis. The second quarter 2018 total of equity cashed out is estimated at $15.5 billion. The peak volume was $102.5 billion (in 2017 dollars) in the second quarter of 2006. The Q2 total was even lower than in the second quarter of 2017 when $15.7 billion was cashed out.

Freddie Mac said borrowers who refinanced their first-lien mortgage last quarter either kept the same interest rate or took slightly higher one. Many of these borrowers refinanced not for rate reduction, but for cashing out equity to consolidate other higher interest debt, pay other bills or use towards home improvements.

More than 95 percent of refinancing borrowers chose a fixed-rate loan. Fixed-rate loans were preferred regardless of their original loan product. For example, 93 percent of borrowers who had a hybrid ARM refinanced into a fixed-rate loan. In contrast, only 3 percent of borrowers who had a fixed-rate loan refinanced into an ARM.