Fannie Mae says that early bets on third quarter economic growth are around 3.0 percent which has the Federal Reserve talking again about raising the fed funds target rate, but odds are it won't happen at the Federal Open Market Committee (FOMC) meeting this week. Even with an acceleration in the second half of the year Fannie Mae's economists are holding to their July forecast of 1.8 percent growth this year.

The current (third quarter) GDP should come in around 2.9 percent annualized, an acceleration that will reflect a rebound in inventory investment from its very low level during the first half of the year. Consumer spending is expected to remain the biggest driver of growth and non-residential investment should increase after three consecutive quarters of decline. However, the company's Economic and Strategic Research group says they expect residential investment to decline for the second consecutive quarter, the first such occurrence since late 2013 and early 2014.

The September economic summary called the loss of 6,000 construction jobs in August discouraging, yet residential construction employment grew by 10,800, the biggest monthly gain since March. This is especially good news given the "bearish" data on new construction spending at the start of the third quarter.

The economists, headed by Doug Duncan, SVP and Chief Economists, don't think Fed board members have made the case to the markets to justify a September rate hike. Because the Fed rarely surprises the markets it will probably increase the volume of its message that it intends to act this year in hopes the fund futures will price in a hike. When Fannie Mae was preparing its report, the futures' odds of a September hike were 36 percent. Since 1989 the Fed has only raised rates five times when the futures market priced less than 40 percent chance of an increase within three weeks of an FOMC meeting. Regardless of market sentiment, Fannie Mae is holding to its earlier prediction of no rate hike at all this year.

Housing data for the single family market were generally week in the latest reports which covered July. Housing starts increased but single family starts were little changed and permits fell to the weakest pace since September 2015. In the multi-family segment however starts rose for the third time in four months and permits were higher for the fourth month in a row. The share of starts in for-rent multi-family building continues to trend up.

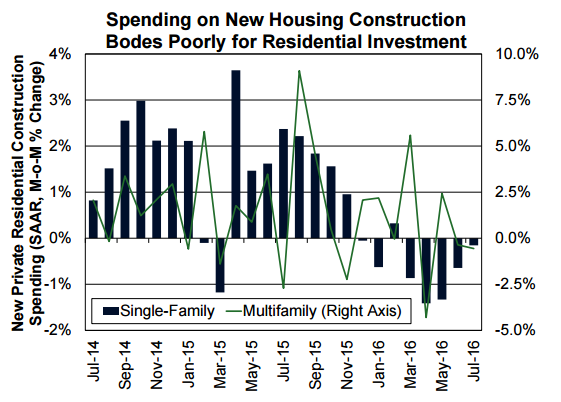

The Census Bureau's report on construction spending for July was more bearish for residential investment that the number of housing starts would indicate. Spending on new single family construction was down for the fifth straight month and dropped for the second month for multi-family construction. This reflects a drop in the average cost per unit of housing starts, especially in the single-family segment. Another reason for the decline in residential investment is the 3.2 percent drop in existing home sales. Residential investment figures include real estate brokerage commissions so the decline in sales add headwinds from that perspective as well. Existing home sales were also down in July from the same month last year, the first time sales have underperformed on an annual basis in 2016. Year-to-date figures however are still running 2.6 percent ahead of 2015.

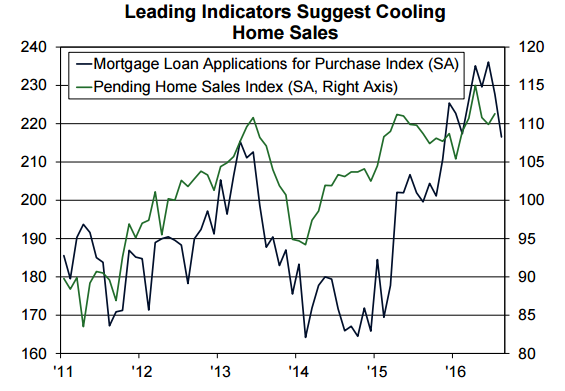

Leading indicators don't suggest a rebound in home sales in the near term. Pending home sales rose just 1.3 percent in July, and data for June were revised from a slight gain to a modest drop. Meanwhile, average monthly purchase mortgage applications fell in August for the second consecutive month to the lowest reading since last November.

Housing inventories remain right. The supply of existing homes for sale was down 5.8 percent from a year earlier and was the lowest supply in any July since 2002. The lean numbers continue to support home price appreciation which, depending on the source of the data, are maintaining gains of 5.0 to 6.0 percent. The increases at the low-end of the housing market have outpaced overall averages, further impeding potential first-time homebuyers.

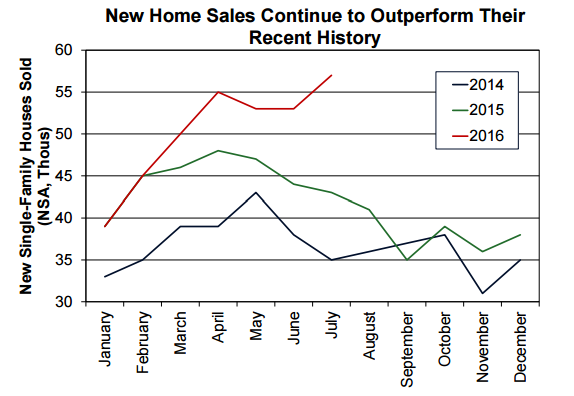

There was a 12.4 percent jump in new home sales in July, the largest increase in two years. The economists note, however, that new home sales are based on contract signings which are volatile and the numbers often suffer large revisions so it is unwise to read too much into the data. Nonetheless, the new home sales trend has strengthened markedly, significantly outperforming activity in recent years. If the improving trend holds up, it should brighten the outlook for single-family homebuilding, especially when the share of new home sales that are under construction or not yet started has climbed to nearly 70 percent," the summary says.

Fannie Mae's economists are holding to most of their earlier forecasts for interest rates, home sales and price gains and purchase mortgage originations. However, they did raise their projected mortgage refinance originations by $50 billion for the second half of the year. For the entire year they expect total mortgage originations to be up 5.4 percent from 2015 to $1.8 trillion and the refi share to be 44 percent.