Doug Duncan, Fannie Mae's chief economist, says homebuyers need to do more shopping around before they settle on a mortgage lender. Results from a recent National Housing Survey shows that one-third of consumers who bought a home last year got only one mortgage quote.

Duncan's report notes that consumers are typically "keen" to compare prices before buying ordinary goods or services - about three out of four say they like to shop around before making a purchase, but yet when it comes to getting a mortgage fewer do. This despite the stakes being generally much higher, "as it is one of the biggest expenses most people will ever incur and shopping for multiple quotes can save borrowers thousands of dollars," Duncan says.

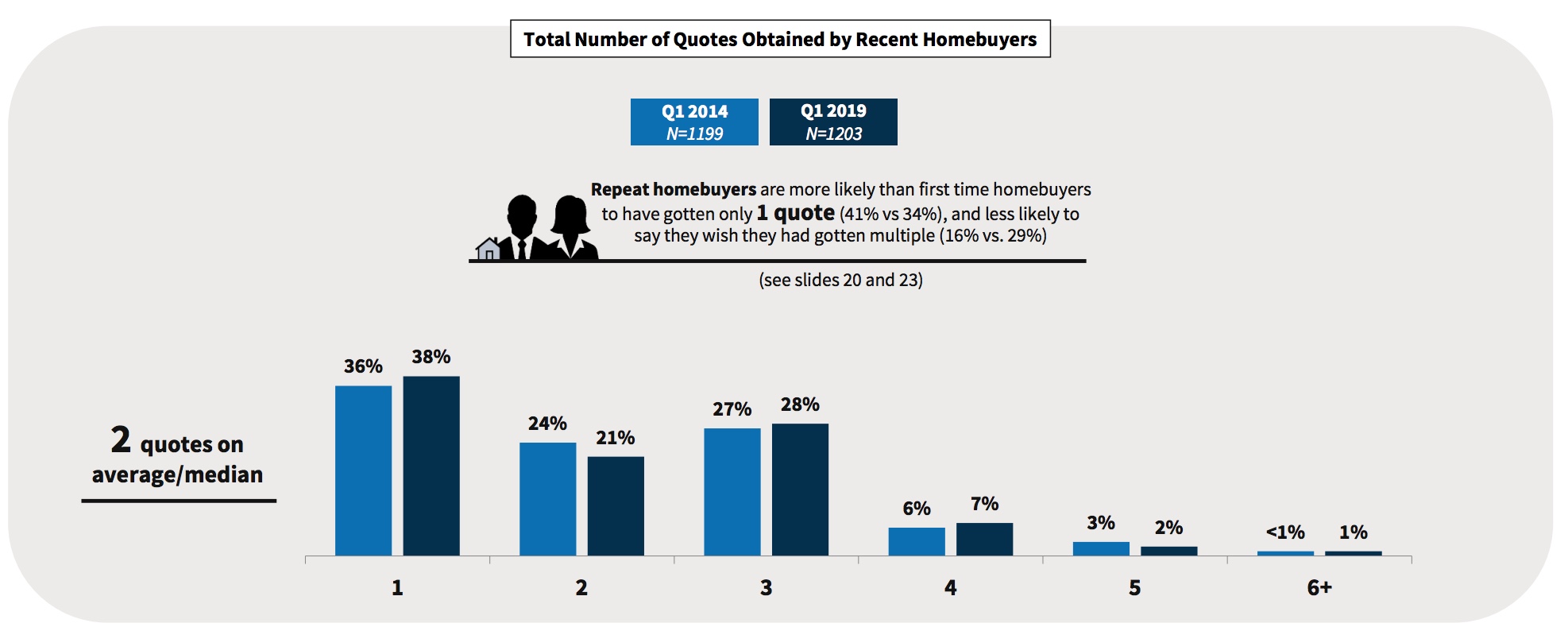

Repeat homebuyers were less likely to get more than one quote than first time homebuyers. Forty-one percent of move-up buyers say they got only one compared to 34 percent of first timers. They are also less likely (16 percent v 29 percent) to say they wish they had done more shopping. The two-thirds who did comparison shop said they experienced more financially favorable terms than those who didn't obtain multiple quotes.

The average number of quotes obtained by homebuyers was two. Very few homebuyers obtained more than three quotes.

Most of those buyers who did comparison shopping said they did so before signing a purchase contract. Only 25 percent shopped after deciding on a home.

Only a fraction of those who got only one quote expressed regret, but Duncan said many reported they had somewhat less success negotiating terms than did those who were able to use other quotes for leverage. "Competition only works if consumers assess their options," he said.

The decision to go with the first offer appears to be explained in part by the influence of non-financial priorities. Real estate agents and family and friends were listed among the most influential sources of advice regarding lender selection; however, the data does not indicate whether third party advice includes encouragement to seek multiple quotes.

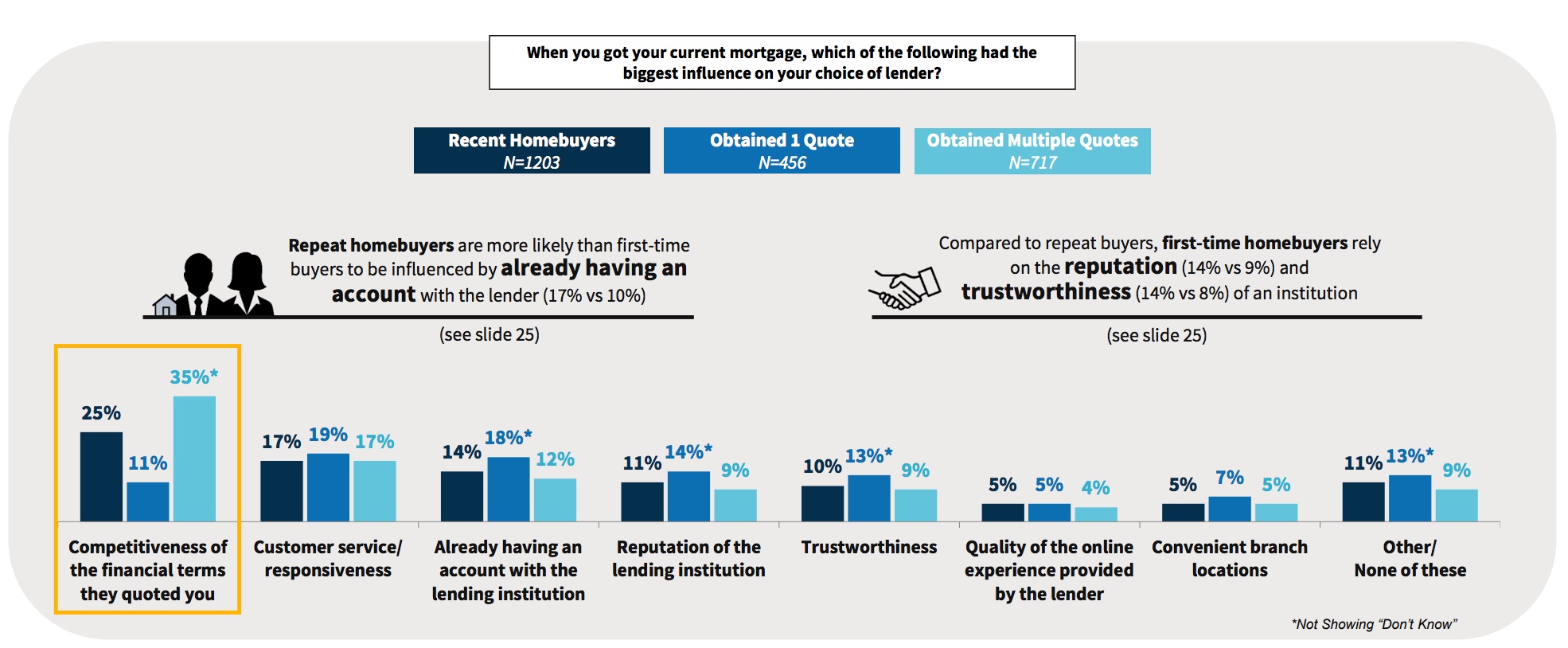

Thirty-five percent of recent homebuyers who received only one quote reported doing so because they were more comfortable with that particular lender and another 28 percent said they were happy with the first quote. Non-shoppers also reported much less concern with competitive terms when selecting a lender, citing other non-financial priorities, such as customer service or already having a relationship with the lender. Duncan said individual households may have good reason for accepting that tradeoff. Buyers who go online to research mortgage prices say they generally turn toward well-known websites like Google, Zillow, and Bankrate.

Duncan says that mortgage shopping can be a complicated and time-consuming endeavor because it means looking at several interrelated components - rates, fees, points - and assumptions about how long the borrower will stay in the mortgage. Advertised quotes are often "teasers" while a true quote is based on variables that are unique to each borrower and evaluated differently by each lender. Then too, pricing can vary daily. Added to this is the time pressure buyers are under when they have actually signed a contract.

He concludes that Fannie Mae's prior research shows that consumers of all backgrounds lack knowledge about mortgage basics. "Building that knowledge may be an important step toward promoting mortgage shopping and improving outcomes for consumers," he said. "Simply knowing that one can save thousands of dollars by getting multiple mortgage quotes may motivate more homebuyers to comparison shop. There is also an opportunity to provide homebuyers with improved access to better tools to understand, shop, and compare mortgages quickly and easily. Removing friction from the shopping process may further encourage homebuyers to get multiple quotes, thereby achieving better outcomes."