Transparency is critical and today much of the paperwork associated with a mortgage is far too confusing.

Recent government regulations have made credit products, especially mortgages, even more opaque with mandated disclosures in obscure legal language produced in small type. As a result, an extra burden has been imposed on lenders while providing no additional benefit to consumers.

Elizabeth Warren, Special Advisor to the Secretary of the Treasury for the Consumer Financial Protection Bureau, told a House subcommittee on March 17th that, "A simple, straightforward and consistent presentation of a credit agreement is the best way to level the playing field between consumers and lenders - and among different types of lenders - and foster honest competition."

So on May 18th, the Consumer Financial Protection Bureau (CFPB) put pen to paper and released their first attempt at simplifying home loan disclosures by combining the Good Faith Estimate and Truth in Lending statement.

The industry responded with more than 13,000 comments. Now the CFPB has offered an even newer version. And they want more feedback.

A few words from the CFPB...

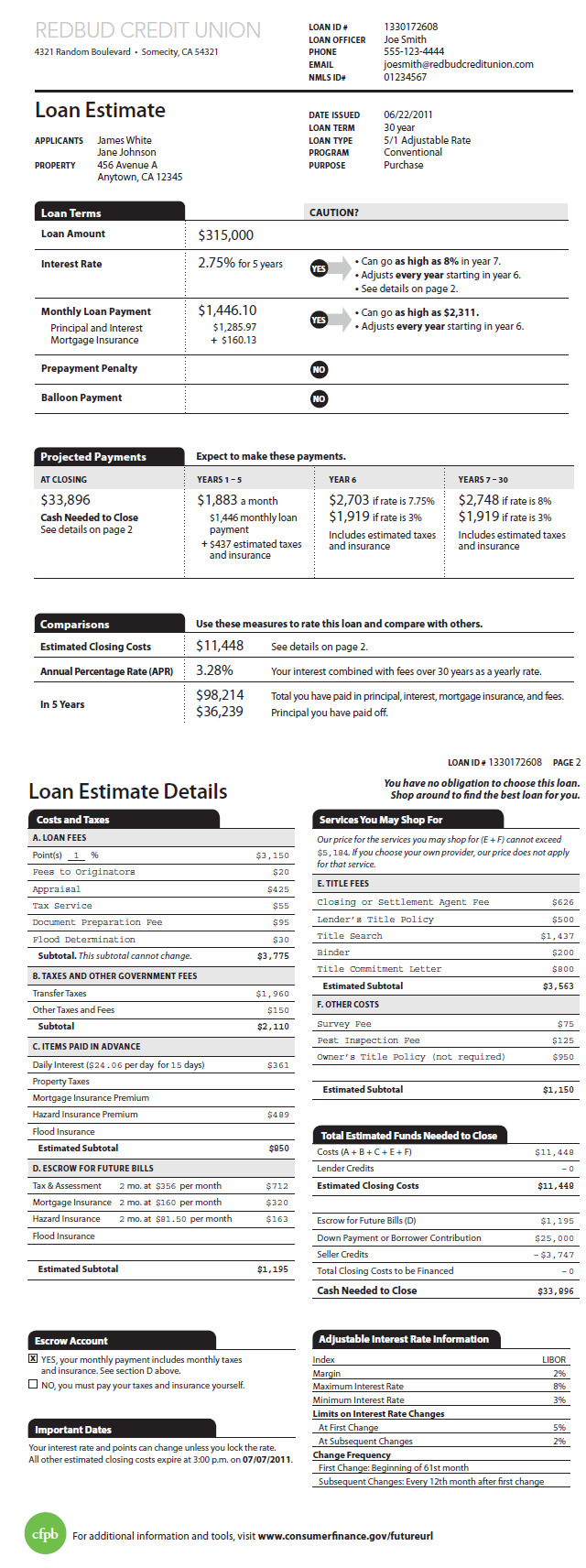

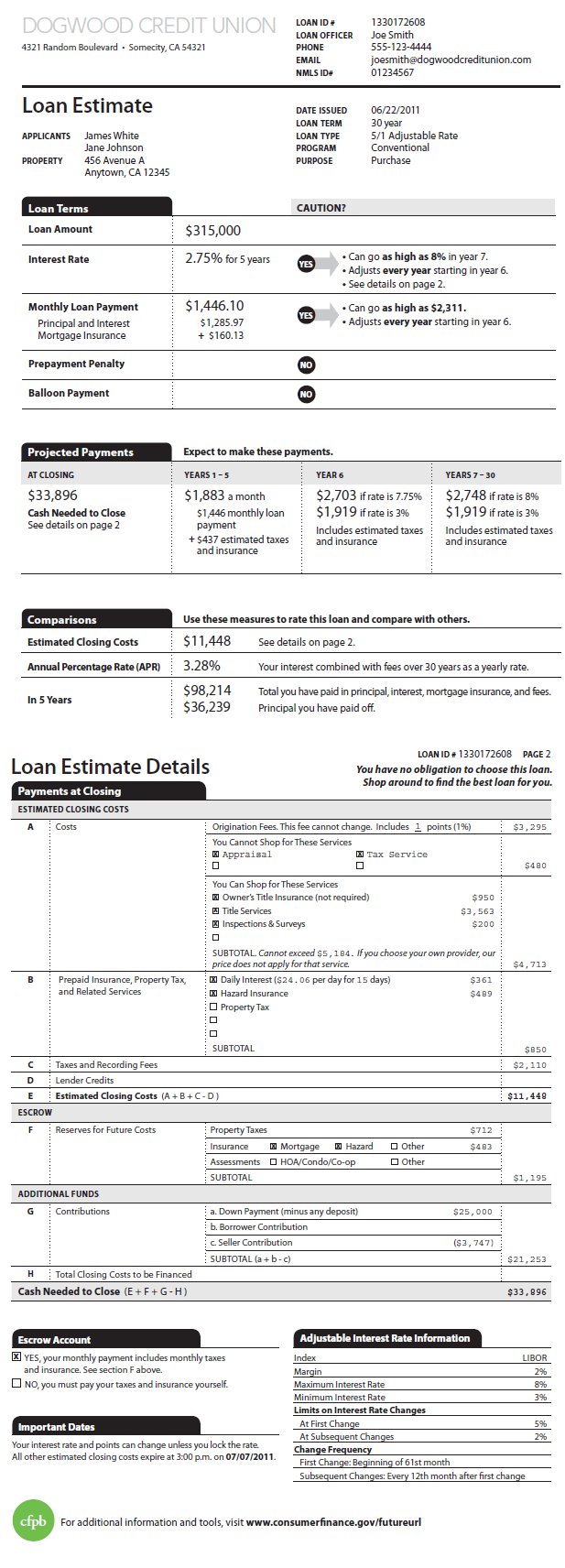

Below are the latest disclosure forms for the same loan product, which come to us from the (fictitious, of course) Redbud Credit Union and Dogwood Credit Union …

- The revised first page features the dark tabs and yes/no buttons from the Ficus Bank draft from Round 1. Both Round 1 forms generally performed well, but some groups of consumers found the Ficus Bank format easier to use, so we kept many of the Ficus design elements. The new prototype also integrates several of the best Pecan features, and it reorganizes and clarifies the information to reflect the lessons we learned from Round 1. Again, this time, the first page is the same for both prototypes.

- The second pages of the Round 2 forms provide alternative approaches to showing closing costs, so that we can focus in on how much detail is helpful to consumers.

Just like last time, here are a few questions we’d like you to keep in mind as you review:

- Would this form help consumers understand the closing costs associated with their loans?

- Could lenders and brokers clearly and easily explain the form to their customers?

- What would you like to see improved on the form? Is there some way to make things a little bit clearer?

In the first round, the back page was the same on both versions. The front page – the “shopping sheet” – was different. This time, the first page is the same on both versions, and the focus is on the back page, which deals with closing costs: how well do these new drafts communicate that information? Which format would you prefer to have your customer use to compare your loan with another?

OPTION 1

OPTION2

WHAT VERSION DO YOU LIKE MORE? <----SHARE YOUR FEEDBACK WITH THE CFPB

This round is open for feedback until Tuesday, July 5th, at 7pm Eastern time.

PS. Dare I say the CFPB is using common sense to communicate with the industry and consumers? I think that's what's happening here....