One obvious lesson we've all learned from the ongoing mortgage crisis: everyone loses when consumers are unable to determine if they can afford to pay back their loans.

Unfortunately recent government regulations have made credit products, especially mortgages, even more opaque with mandated disclosures in obscure legal language produced in small type. As a result, an extra burden has been imposed on lenders while providing no additional benefit to consumers. Transparency is critical and today much of the paperwork associated with a mortgage is far too confusing.

Elizabeth Warren, Special Advisor to the Secretary of the Treasury for the Consumer Financial Protection Bureau, told a House subcommittee on March 17th that, "A simple, straightforward and consistent presentation of a credit agreement is the best way to level the playing field between consumers and lenders - and among different types of lenders - and foster honest competition."

Today the Consumer Financial Protection Bureau (CFPB) put pen to paper and released their first attempt at simplifying home loan disclosures by combining the Good Faith Estimate and Truth in Lending statement. And now they want our feedback....

From the CFPB...

Know Before You Owe. Go!

Written by Patricia McCoy

We’ve just posted two draft designs for a single, simpler mortgage disclosure form on our Know Before You Owe page. Now, we need to hear from you!

The task is pretty simple: Consumers would receive a form similar to one of these versions within a few days of applying for a loan. Take a look, and tell us which one would do a better job of disclosing the necessary information.

Right now, anyone who applies for a mortgage gets two disclosures that contain basic information about the mortgage: the Truth in Lending form and the Good Faith Estimate.

The feedback process we’re starting today is one of the first steps in combining the Truth in Lending form and the Good Faith Estimate into a single, simpler disclosure form. While you’re looking at one of the forms, think about these questions:

- Would this form help consumers understand the true costs and risks of a mortgage?

- Could lenders and brokers clearly and easily explain the form to their customers?

- What would you like to see improved on the form? Is there some way to make things a little bit clearer?

At the heart of our work is the idea that the consumer financial product and services market should work for you. We think we should learn from you what you want to see. One of the best ways to do that is also the simplest: we’re asking.

This is the first step in a process that will last months. There will be more opportunities to weigh in as we move forward. But if you want to help set the direction of a new mortgage disclosure form from the beginning, you should weigh in today.

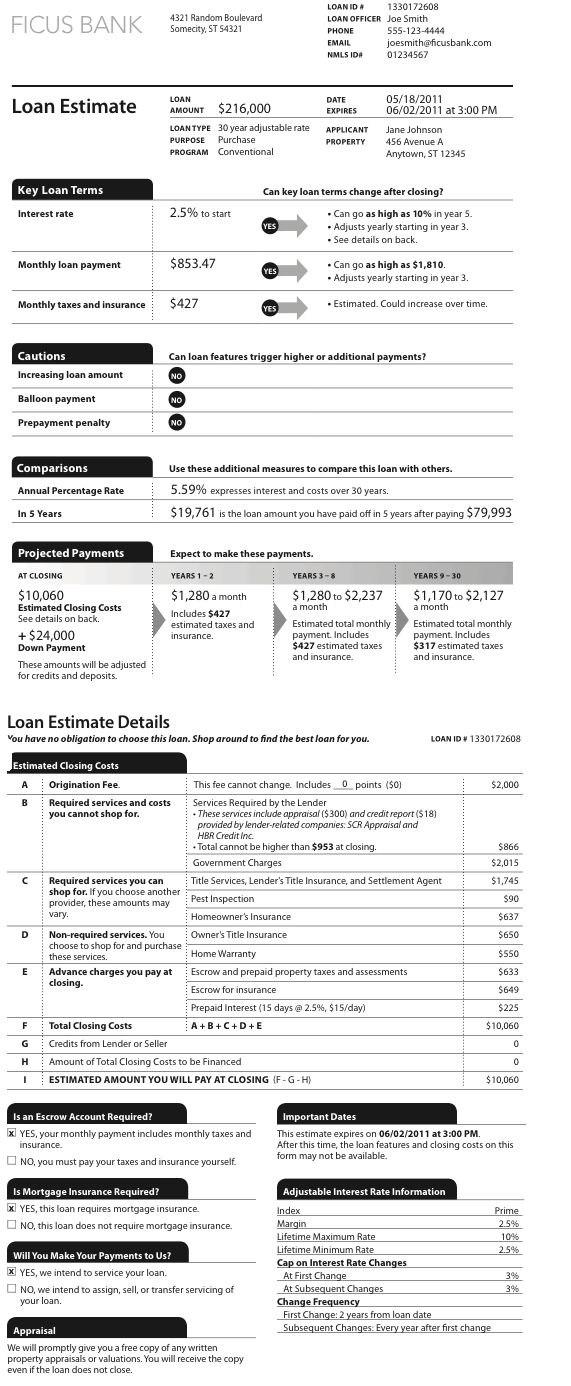

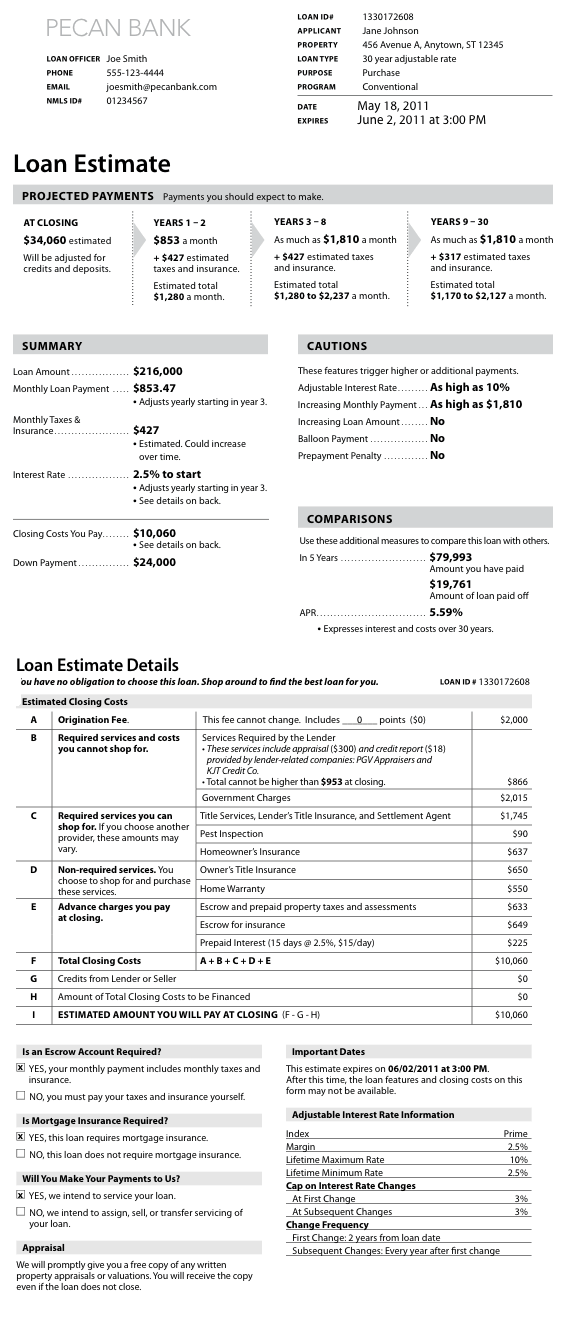

Here are two disclosure forms for the same loan product. Please select the disclosure that you could most easily use to inform a consumer about the loan they’ve requested.

OPTION 1

OPTION 2

From now until Friday, May 27th, you can review our draft designs, and tell us what you like best. It only takes a few minutes, and your input will be delivered to our team.

------------------------------------

Tomorrow, the CFPB will begin testing two alternate prototype forms that are designed to be given to consumers who have just applied for a mortgage loan. This testing – which will take place over the next several months and involve one-on-one interviews with consumers, lenders, and brokers – will precede and inform the CFPB’s formal rulemaking process. The Bureau will also consider underlying regulatory issues and ways to refine closing-stage forms, a process that will likely extend into the fall and early next year. The Bureau is required by the Dodd-Frank Act to issue proposed forms and implementing regulations by July 2012 for formal notice and comment

WHICH VERSION IS BETTER?

David Stevens, President and CEO of the Mortgage Bankers Association (MBA) issued the statement below in response.

"Making mortgages easier to understand for prospective borrowers has been a long term priority for the mortgage industry and we are pleased to see the initial prototypes take a step in that direction. One of the challenges this effort inevitably faces is trying to strike the right balance between simplification and providing as much information as possible to help borrowers make the most informed choices. Previous attempts at revising the forms have struggled with this paradox and this is going to be a focus of everyone involved in this effort.

"The CFPB staff has obviously put a lot of thought into the new forms and we look forward to participating in the review and revision process alongside consumers. One of MBA's primary goals will be to make certain that not only do the new forms provide consumers with the information they need in a simple, clean way, but also that they can be implemented into lenders' operations and systems with a minimum of disruption.

"Just 18 months ago the industry expended considerable costs on RESPA changes. We need to make sure that this new form is highly beneficial to consumers who will bear the implementation costs."