Foreclosure sales have not regained the momentum they had before numerous lender moratoria brought the process to a virtual halt last Fall.

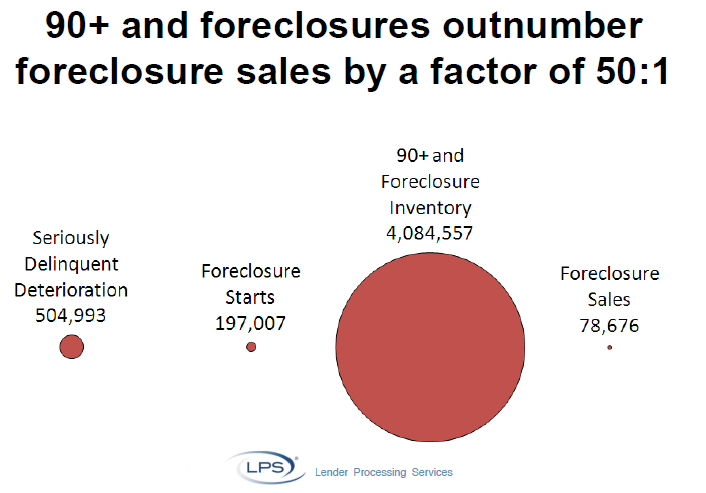

According to the May Mortgage Monitor Report released by Lender Processing Services, Inc. (LPS), the number of serious delinquencies (90 days delinquent) and foreclosures (loans referred to an attorney for foreclosures but not yet sold) outnumber the actual foreclosure sales by a factor of 50 to 1.

During the month of May there were a total of 4,084,557 loans that were seriously delinquent or in foreclosure while only 78,676 foreclosure sales took place in the month.

The delinquency rate was essentially unchanged from April at 7.97 percent but was down from a rate of 9.74 in May 2010. The foreclosure rate declined slightly to 4.11 percent from 4.14 but was up substantially from the 3.66 percent rate a year earlier. There were 197,007 foreclosure starts in May, nearly 10 thousand more than in April but down from 237,198 one year earlier.

New problem loans, defined as those that were 60 days or more delinquent during the month but had been current six months earlier, were at 1.27 percent, down from approximately 1.80 percent a year earlier and less than one-half the peak level seen in 2009.

Foreclosure sales peaked almost exactly three years ago at around 130,000 per month and, after a number of sharp monthly variations, were at almost that level last September when deficiencies in the foreclosure process were uncovered and foreclosure sales plummeted to about 60,000 in October. Sales have not recovered. The 78,000+ sales in May represented less than 6 percent of the loans in the foreclosure inventory.

The May data shows that the biggest drop in foreclosure sales since the September 2010 peak has been seen in East Coast states, with a decline of 96% in DC, 80% in Maryland, 79% in New York, and 75% in New Jersey. Additionally, inventories of foreclosures in judicial states have increased twice as much as inventories in non-judicial states over the last year.

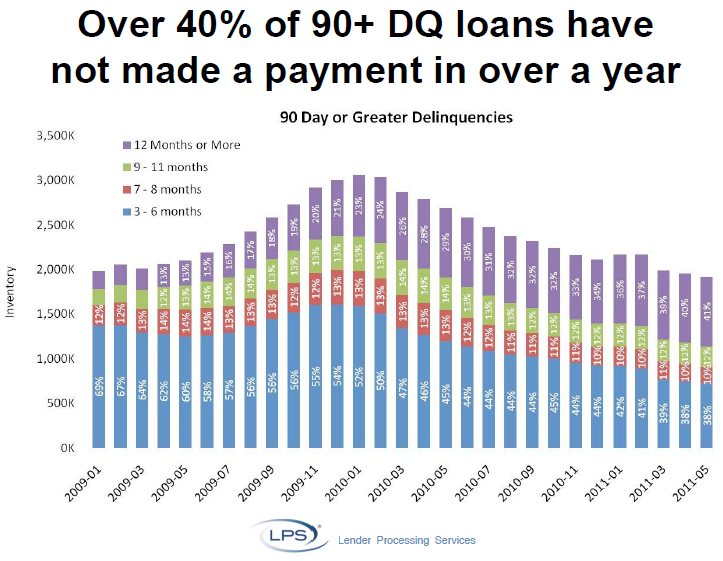

The average time a loan spends in foreclosure continues to increase. In May 40 percent of delinquent borrowers had not made a payment in over a year and one third of those in foreclosure had not made a one in over two years.

Negative equity continues to be a problem. LPS reports that nearly 30 percent of performing loans are in a negative equity position. This is ominous as other LPS data shows that underwater loans default with 10 times the frequency of those where the borrowers have equity. Of the 70 percent of current foreclosures with negative equity, over 35 percent have combined loan to value ratios of over 150 percent.

The Million Dollar Question: Have Home Prices Bottomed?

"Nationally, housing faces a long road to recovery, but not all markets are equal", says MND's Managing Editor Adam Quinones. "While areas with a high concentration of distressed properties are clearly stuck in a deflating environment, some communities will see price stability. It's all based on local and regional economies. Where are jobs being created? Where are the best schools? Where is value being created by the community? Where do buyers want to live? This is where the housing recovery can build momentum. Of course you need to be in the right financial situation to even be asking these questions. That's another problem all together. Tight credit demands from lenders combined with damaged borrower credit profiles (and a lack of reserves) implies buyer demand will lag the broader economic recovery, which is lagging itself. Finding a bottom in the hardest hit areas is another story. Here, the GSEs, FHA, and major banks must manage their REO inventory carefully. In these areas, home prices remain highly-sensitive to even the smallest of shocks in buyer sentiment, such as the premature release of shadow inventory. It's gonna be a tight-rope walk. Step 1 is stopping the negative feedback loop."

Foreclosure Filings in Downtrend. Masked Reality?

Housing Scorecard: Delinquencies Down. Foreclosures Delayed

Foreclosure Filings Drop. Prevention Policies Distorting Supply and Demand

LPS Data Shows Long Delays in Foreclosure Process

CoreLogic Estimates Shadow Inventory at 1.8 Million Homes

Foreclosure Filings Fall. Robogate Fallout Skews Report

ABOUT: LPS data is based on mortgage data and performance information on nearly 40 million first mortgages across all types of credit products.