There was plenty of foreshadowing, but Fannie Mae's Chief Economist Doug Duncan said last week that cost-cutting has risen as a priority for mortgage lenders. Both the Mortgage Bankers Association's (MBA's) first quarter Quarterly Mortgage Bankers Performance Report and an earlier release from Fannie Mae regarding results from its second quarter Mortgage Lender Sentiment Survey reported mortgage lender's declining profits and gloomy outlook for improved financial results.

The MBA's report was only the second in its 10-year history in which independent mortgage lenders and bank mortgage subsidiaries reported a loss, in this case $118 per loan. Fannie Mae's lender survey found more than a third of the 170 institutions that responded expected net profits to decline while nearly another half expected no change. Fannie Mae said it was the seventh consecutive quarter that lenders conveyed a negative profit outlook.

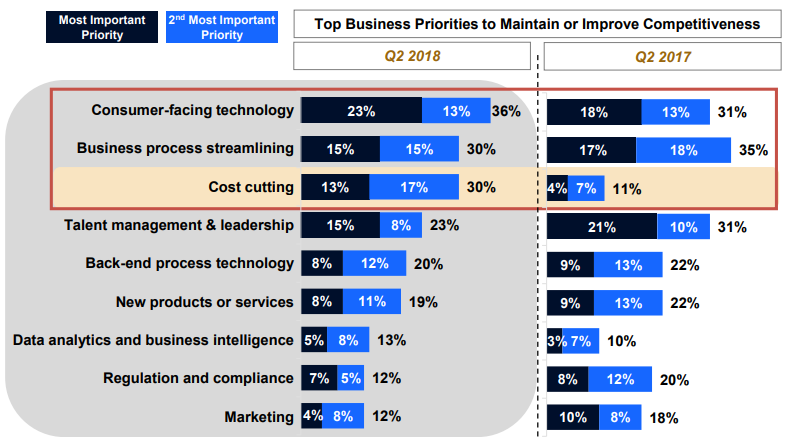

Declining demand is the driver of the problem, pushing per-loan production costs higher. Duncan dug more deeply into the Fannie Mae survey results for his Perspectives blog post, and reports among the top business priorities named by respondents, cost cutting has jumped from near the bottom in May 2017 to the third most important in May of this year. "Consumer-facing technology" and "business process streamlining" were the top two priorities both this year and last, and one could argue that the seconds reflect cost concerns as well.

Duncan says lenders are facing an increasingly difficult market environment. With mortgage rates up about 80 basis points since last September, refinancing is falling sharply; the average of weekly applications was the lowest for the month of May than in any period since December 2000. With existing and new home sales both down in April, Purchase applications fell as well, down 2.9 percent from April to May.

He says increasingly tight margins will likely persist as a top driver of lenders' mortgage business strategy. Fannie May's outlook calls for interest rates to continue to rise and housing inventories to remain tight. "Despite lenders making significant investments to improve operational efficiency over the past few years, margins have still declined."

Pre-tax production profits were 33 basis points in the first quarter of 2016, 10 basis points in the same quarter of 2017, and represented a loss of 8 basis points in the first quarter of this year, the first negative outcome since 2014. Now, Duncan says, lenders appear to be turning to cost cutting as a means of managing their bottom lines. "

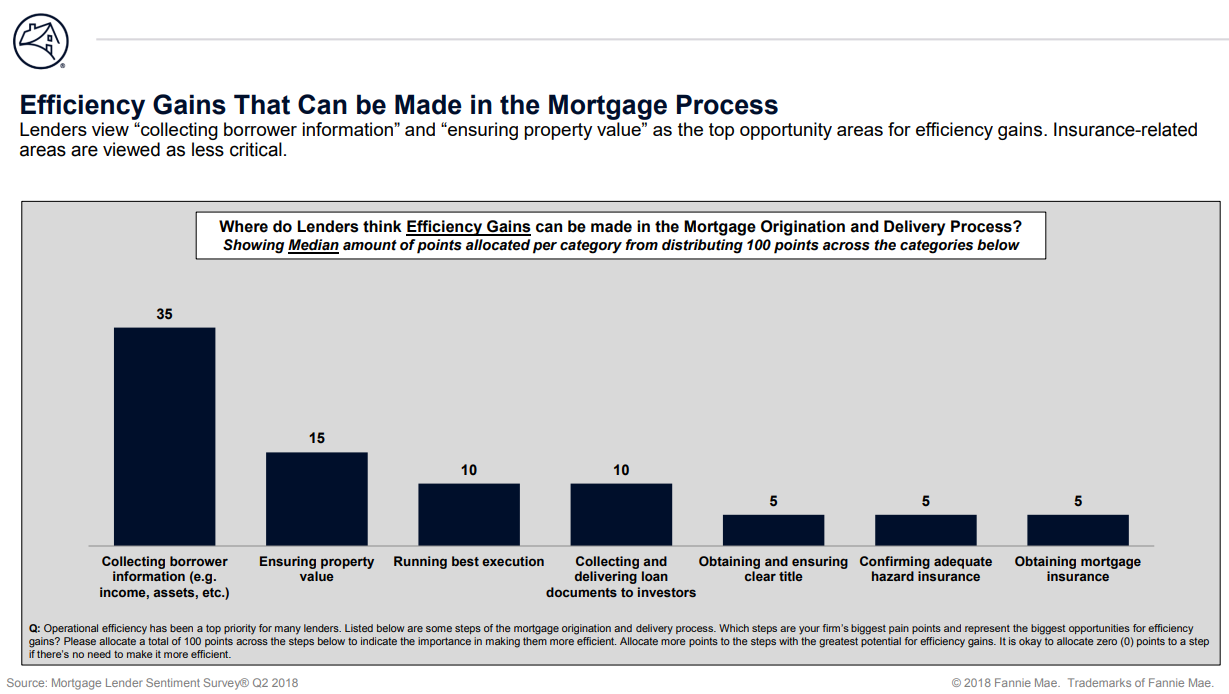

When asked where efficiency gains might best be made, lenders view "collecting borrower information" that is data on assets and income, etc., as the most productive area, cited by 35 percent of respondents. Ensuring property value was second at 15 percent. Functions related to hazard and private mortgage insurance received the fewest mentions.

Personnel expenses made up 66 percent of total loan production expense in the first quarter of 2018, about the same as the two previous first quarters and "Payroll reduction could potentially assume a more prominent role in future cost-cutting efforts." Hiring on behalf of nonbanks and mortgage brokers remained elevated in April, still near expansion highs, but Duncan suggests that mortgage industry employment may be approaching the cyclical peak. "With rising interest rates and tight housing supply squeezing mortgage origination volumes, lenders could soon turn to job reduction as a means of maintaining a competitive edge."