Even as homeownership rates remain at historic lows the mortgage debt on single family homes is increasing, ending seven years of decline. Freddie Mac's Office of Chief Economist, in its June U.S. Economic and Housing Market Outlook, looked at how, as the housing market is "pivoting toward normalcy," this new debt will be managed; "who will hold it, at what price, and in what form?"

The report says it is tempting to think that the improving outlook for the economy and jobs will mean an increase in homeownership but the economists say "housing demand is unlikely to trump demographics for several years." While new households are forming they are also tending to rent and that patterns is likely to continue for several years.

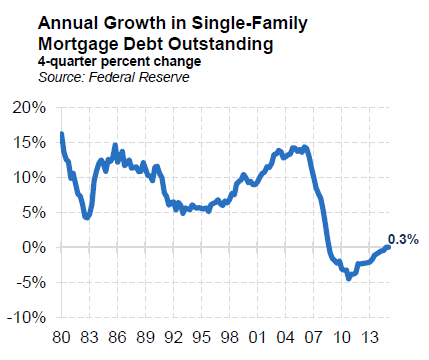

The declining mortgage debt outstanding (MDO) and low interest rates had lowered the debt service to disposable income ratio for mortgages to the lowest levels since the early 1980s, 4.6 percent in the fourth quarter of 2014, down from a high of 7.2 percent in early 2007. Additionally Freddie Mac notes that in more normal times the resale of an existing home results in an increase in aggregate mortgage debt of about 30 percent with each new home purchase loan. Since the housing crash and its negative home price appreciation that has not been the case but in the first quarter of 2015 the average payoff of a closed Freddie Mac loan was about $170,000 while the unpaid principal balance (UPB) of a new loan averaged about $225,000 - returning to the more normal 30 percent.

If home sales and home prices continue to increase then MDO should be driven higher, reversing the decline that resulted in part from low homeownership. The latest American Community Survey data from 2013 shows that ownership and mortgage utilization vary by household age. Households typically start off as renters, transition into homeownership in the late 20s and early 30s with homeownership tending to increase throughout life. But as households enter their 50s and 60s their mortgages dwindle and more own their homes free and clear.

At present we have the largest age group - Millennials - beginning to form households although primarily as renters. Many Boomers have paid down their mortgage principal while others own their homes outright and the Gen Xers are entering the age when homeownership rises and mortgage utilization peaks, but the report points out this small generation doesn't have a lot of impact on the numbers.

While homeownership rates are down for all age groups they still mortgage their homes. Even if the age gaps continue the nation is likely to see many millions more households and homeowners over the next five years and thus greater mortgage debt. "That fact will challenge capital markets: who will hold the new debt, at what price and in what form?"

The declining single-family mortgage debt has, until recently, meant the market has not had to answer these questions but with MDO set to increase the market is going to have to find it a home. The Federal Reserve's $1.7 trillion current holdings in agency mortgage backed securities will also eventually need to be placed with new investors.

Freddie Mac says that fortunately investors' appetite for mortgage bonds seems to be coming back. The development of credit-risk transfer transactions such as the company's Structured Agency Credit Risk (STACR) offerings and Agency Credit Insurance Structure (ACIS) transactions, is expected to become increasing important to housing the debt over the next few years.

In this edition Freddie Mac's economists revised a few of their projections from previous Outlooks. GDP growth estimates were downgraded from 2.3 to 2.0 percent for the year based on a further drop in the first quarter numbers as a result of the Bureau of Economic Analysis "second estimate." The forecast for 2016 remains at 2.7 percent.

Most of the earlier housing forecasts are unchanged - home sales remain at 5.6 million units, housing starts at 1.14 million and house price growth at 4.5 percent this year and 3.5 percent next year. Mortgage originations however have been revised upward by 8 percent to a projected $1.35 trillion in 2015, tapering to $1.275 trillion in 2016. The refinance share will be 43 percent this year, dropping to 30 percent in 2016.