Stock markets are flying this morning in reaction to China’s announcement on Saturday that it will loosen the yuan’s peg to the U.S. dollar

The People’s Bank of China said now that economic recovery has “cemented,” there is “no foundation” for large fluctuations in the yuan’s rate. On Sunday, the central bank added that currency reform would contain inflation and help prevent asset bubbles from forming.

“While this weekend’s announcement from China is a small step and likely aimed at keeping the pressure off during the G20 meeting and to avoid being labelled a currency manipulator by the U.S. Treasury next month, it is still significant step to a slowly appreciating CNY this year,” said economists BMO Capital Markets. “The CNY has already appreciated considerably versus the EUR so far this year so a more rapid pace of strength versus the USD will likely not take place until next year, when the global economic recovery is more sturdy.”

At 8:30 eastern time, the UK FTSE 100 was up 51.32 points to 5,302.16 and the German Dax was up 78.75 points to 6295.73. In Asia, Japan’s Nikkei was up 242.99 points to 10,238.01, Hong Kong’s Hang Seng was up 625.47 points to 20,912.18, and China’s Shanghai Composite was up 72.99 points to 2,586.21.

At home, Dow futures are up 115 points to 10,488 and S&P 500 futures are up 15.00 points to 1,121.00. The 2-year Treasury note is 3.2bps at 0.746% and the benchmark 10-year Treasury note yield is 7.2bps higher at 3.297%

While the US dollar weakens, NYMEX Light Crude is trading $1.12 higher at $78.30. Spot Gold, which hit another record high at $1,265.39 overnight, is currently up $0.20 to $1,258.50

Key Events This Week:

Monday:

Treasury Auctions:

- 11:30 ― 3-Month Bills

- 11:30 ― 6-Month Bills

Tuesday:

The nation's first "comprehensive strategy to prevent and end homelessness" will be released by the U.S. Interagency Counsel on Homelessness (USICH). The council is an independent agency composed of 19 cabinet secretaries and agency heads dealing with aspects of homelessness. The report is designed to serve as a roadmap for joint action by the agencies represented on the council in the formation of programs and budget proposals toward the council's goals.

The report, titled "Opening Doors: The Federal Strategic Plan to Prevent and End Homelessness," is the result The HEARTH Act, signed into law in May, 2009 and subsequent meetings USICH has held with stakeholders, input from organized federal working groups, public comment, and experts throughout the country, all focused on developing an action plan to solve homelessness for veterans, adults, and families.

After the plan is released in a formal White House presentation which will be broadcast live on the White House website, USICH and the member agencies plan to work with Congress, mayors, legislatures, advocates, community organizations, and other stakeholders to implement the proposed programs.

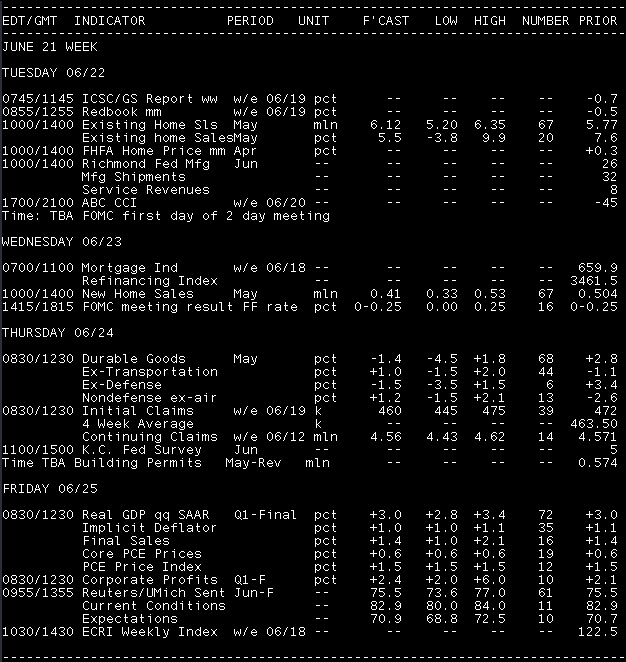

10:00 ― Existing Home Sales are expected to rise 7.5% in May, putting the annual sales pace at 6.20 million and building upon the 7.6% drop seen in April. As positive at that sounds, oversupply problems remain ― at the current sales pace there are 8.4 months’ worth of existing homes on the market right now. Economists are anticipating a broad rise in part because the government tax credit for first time homebuyers expired at the end of April; in addition, pending home sales indicates a rise.

“Although the federal homebuyer tax credit expired at the end of April, contracts do not need to be closed until the end of June,” noted economists at Nomura Global Economics. “The existing home sales report ― unlike the new home sales report or the pending home sales index ― tracks contract closing, and therefore could remain strong for a bit longer. We forecast that sales increased by about 6% month-over-month in May to an annualized rate of 6.1 million units. Sales are likely to drop off sharply once the closing deadline passes, however.”

Gauging the potential market reaction, economists at BBVA say any negative surprise “would raise questions regarding the strength and sustainability of the housing market in a post home buyers’ tax credit period.”

Treasury Auctions:

- 11:30 ― 4-Week Bills

- 1:00 ― 2-Year Notes

Wednesday:

10:00 ― Economists are anticipating a major decline in the New Home Sales Index. The consensus looks for sales to fall by more than 20% from an annual pace of 504k to 400k, and some predictions are as low as 370k. The anticipated drop in May follows a 14.8% jump in April, which received a boost as homebuyers raced to close their contracts before the expiration of the tax credit.

“New home sales jumped 49% during March and April combined,” said economists at IHS Global Insight. “With the homebuyers' tax credit expiring April 30, sales will likely post their largest monthly percentage drop on record (data start in 1963). We project that sales will plummet 26% to 375,000 (annual rate).”

2:15 ― Few changes are expected in the FOMC’s latest meeting announcement. The Federal Reserve has indicated that policy won’t be tightened at any time soon, so it’s a virtual certainty that the overnight lending rate will remain in the zero to 0.25% range. Though most economists believe the recession ended months ago, lowering the unemployment rate remains much more important that worrying about inflation.

“Recent Fed speeches have indicated that economic conditions are improving in line with Fed expectations, but growth will only be moderate and inflationary pressures will remain at bay,” said economists at BBVA. “A surprise in the statement would be the removal of the ‘extended period of time’ language, which would indicate that rates will rise sooner than expected.”

“While the economic recovery is still moving ahead, the employment market picture remains extremely troublesome in terms not only of the persistently high unemployment rate, but also in sharp increases in the duration of unemployment,” added economists at IHS Global Insight. “Core CPI inflation remains below 1%, and well below the Fed's target of 1.5% to 2.0% ― with potentially more downward pressure in the next few months. Beyond these domestic risks, the crisis in the Eurozone and much lower level for the euro threatens further disinflationary shocks to the U.S. economy.”

In the last meeting, only Kansas City Fed president Thomas Hoenig dissented from the majority vote. Recent comments suggest he made repeat that vote, though Eurozone troubles could push him into the majority vote.

Treasury Auctions:

- 1:00 ― 5-Year Notes

Thursday:

8:30 ― Expectations are divided for Durable Goods. The “consensus” is for a 0.5% decline in May, but predictions range from -2.5% to +1.5%, according to Bloomberg. In April the index leapt 2.8% on account of a 16% increase in transportation orders, a 228% surge in orders for non-defense aircraft, and a 7.2% rise in orders for motor vehicles and parts.

Economists at Nomura are predicting a 2.5% cut as aircraft orders reverse earlier gains and industrial orders get hit by weaker metal prices.

“Boeing booked just five new orders during the month, down from 34 in April,” they noted. “We believe this will translate into a 75% decline in the dollar value of aircraft orders. Lower metals prices should also reduce the nominal value of primary metals orders and shipments. We expect core orders (non-defense capital goods orders excluding aircraft) to show another healthy gain, however, indicating that business demand for investment goods remained strong.”

Economists from BBVA point out, however, that aside from transportation order, new orders should see “a widespread increase, which would point to strengthening private demand.”

8:30 ― In the week ending June 12, Jobless Claims rose 12k to 472,000, adding additional frustration after months of stubborn stagnation. The four-week average of new claims was at 463,500, above the 450k mark which economists say would indicate private jobs growth between 40K and 80K per month.

“The labor market has added private jobs consistently in 2010 from January through May. Until the May payroll data job growth had accelerated each month,” said economists at BTMU. “In April, net new private jobs jumped by +218K then dropped back sharply to just +41K in May. Furthermore, the downward trend in initial jobless claims has stalled, leading us to believe that April’s strong growth in private payrolls is the anomaly, rather than May’s anemic growth, which is now looking more and more believable.”

- Treasury Auctions:

- 1:00 ― 7-Year Notes

Friday:

8:30 ― Final revisions to Q1 GDP aren’t expected to be large. The previous revision downsized the indicator from +3.2% to +3.0%, and economists say no data has indicated any large revisions since then.

“We expect inventory accumulation to be revised up slightly, and net foreign trade and consumer spending on services to be revised down,” said economists at IHS Global Insight. “If we're right, that would tilt the distribution of first-quarter growth even further towards inventories and away from final sales, which would intensify concerns about the future strength of the recovery once the inventory boost to growth begins to fade.”

Economists at BBVA said if GDP were revised lower, it would “negatively affect the market’s mood and increase concerns over the sustainability of the recovery.”

10:00 ― Consumer Sentiment rose almost two points to 75.5 in June’s preliminary survey, marking the highest level in about a year-and-a-half. The gain was surprising given declines in the stock market, the ongoing Eurozone debt crisis, and high unemployment levels. But now, with gasoline prices falling, equity markets stabilizing, and support plans for the Euro crisis agreed upon, economists are expecting the Reuter's/University of Michigan's index to remain on an upward trend.

“Somewhat surprisingly, the preliminary estimate of consumer sentiment held up well in the face of declining stock prices. Even the report's assessment of current government policy improved despite the oil spill in the Gulf of Mexico. This encouraging outcome may be a sign that the consumer sentiment recovery is more durable than previously feared,” said economists at Nomura.