Homeownership has barely budged off the historic lows reached during the Great Recession and its aftermath. The housing industry has been struggling to understand why this phenomenon has continued even as the economy recovered, and more households are being formed.

Many potential first-time homebuyers, especially Millennials have reported on the hurdles they must overcome to buy, including the difficulty of saving for a downpayment and for many a large burden of debt, especially student loan debt. Fannie Mae says the financial barriers are even higher for low-to-moderate income (LMI) individuals and even when they do purchase, they are often at higher risk of default due to unaffordable mortgage terms, higher loan-to-value ratios, and fragile household balance sheets.

The company commissioned a study by three researchers to see if affordable lending programs administered through state Housing Finance Agencies (HFAs) might be a partial solution to providing homeownership. The three, Stephanie Moulton of Ohio State University; Matthew Record also of Ohio State and San Jose State University; and Erik Hembre, University of Illinois, Chicago; .have published a working paper on their initial findings.

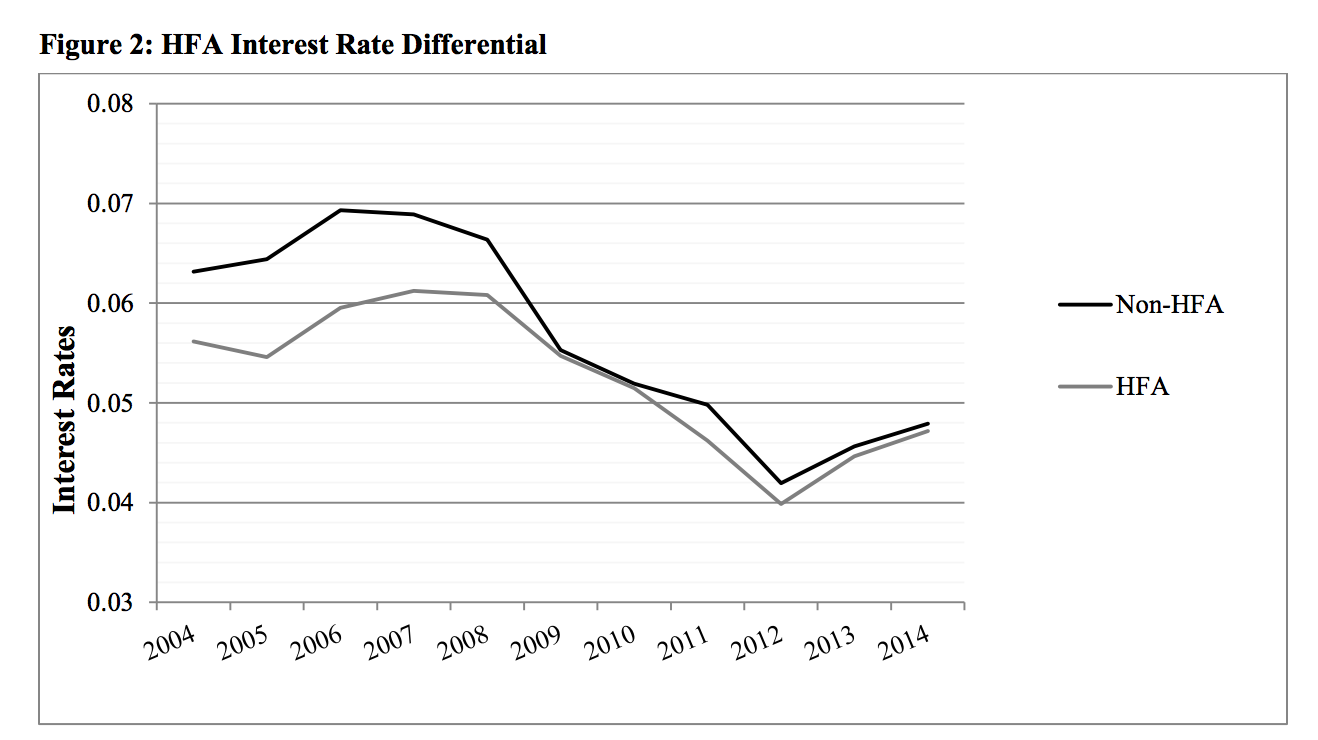

By the end of 2014, HFAs had facilitated home purchases for more than 3.2 million households, the majority of whom were LMI first-time homebuyers with incomes below 115 percent of the area median. These mortgages do not rely on the risk-based pricing of the subprime mortgages originated during the housing boom; prior to 2010, a majority of the mortgages originated by HFAs were financed through tax-exempt mortgage revenue bonds (MRBs), allowing agencies to charge below market interest rates. Further, mortgages originated through HFAs typically meet conforming loan standards and are often securitized by Fannie Mae, Freddie Mac, or Ginnie Mae.

If HFA originated mortgages meet conforming loan standards, what, if anything, is their added benefit to the mortgage market? Aside from targeting LMI first time homebuyers, HFAs tend to originate mortgages at lower costs with additional value-added services such as homebuyer education and counseling and preventative servicing practices. The theory is that these services might lead to better loan performance. HFAs were granted an exemption from the Qualified Residential Mortgage (QRM) requirements in part because of the assertion from the National Council of State Housing Agencies (NCHSA) that HFA originated mortgages had inherently lower risk due to "government oversight, an important public purpose, strong underwriting, proactive servicing, and a proven track record of safe and sound performance."

There are few empirical analyses of HFA originated mortgages. How do HFA borrowers compare to conventional first-time homebuyers? Do loans originated through HFA programs perform better than loans to otherwise similar borrowers? And if yes, what are the mechanisms that lead to better loan outcomes? Is it something about the structure of the loan, or additional services provided that reduces the risk of default? The Fannie Mae study examined more than one million loans single-family purchase loans it securitized between 2005 and 2016 and tracked outcomes through late 2016.

More than 10 percent of the loans were originated through state HFA loan programs. Of those, 21 percent were to households with incomes below 50 percent of area median, half were to those with incomes between 50-80 percent of area median, 18 percent were to households between 81 and 100 percent, and only 12 percent were to households with incomes greater than 100 percent of area median.

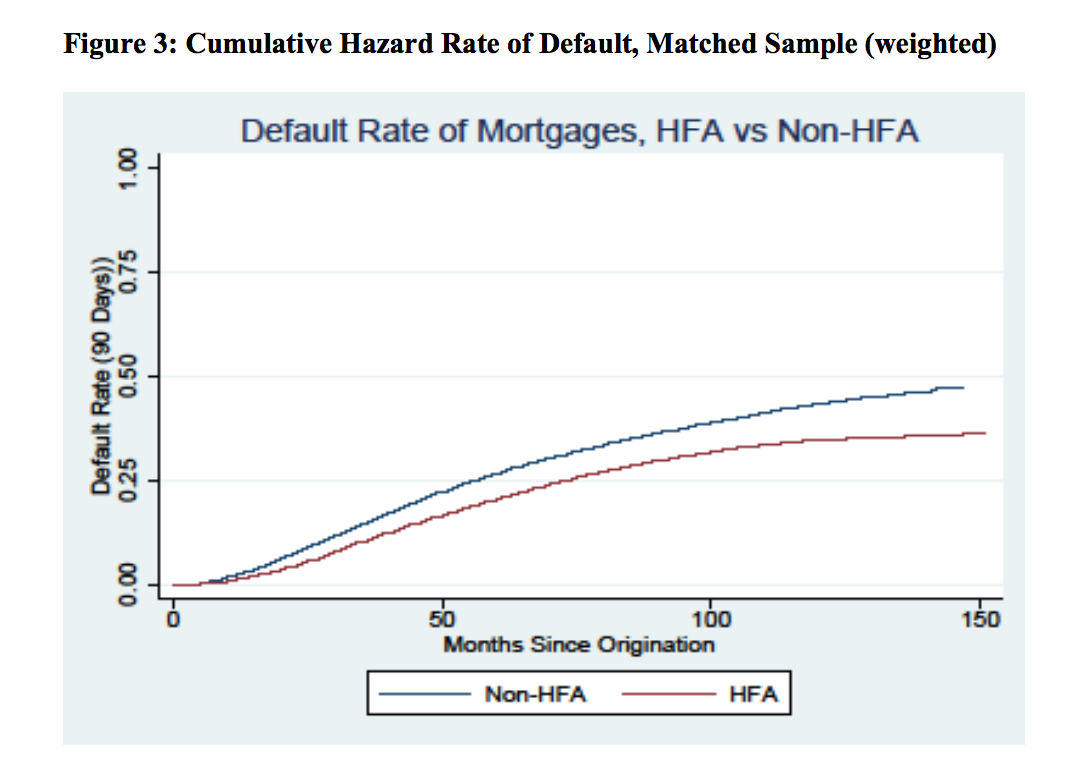

They constructed a matched sample of HFA and non-HFA loans with similar characteristics at closing such as geography, loan terms, income, credit score, and loan-to-value (LTV) ratio. Among the LMI borrower sample more than one in five experienced a 90-day default between origination and October 2016 and 14 percent experienced foreclosure. About half prepaid their loan. through refinancing or home sale. Findings from a competing hazard analysis show that the risk of ever experiencing 90-day default is about 20 percent lower for borrowers with loans originated through HFAs, and the risk of foreclosure is about 30 percent lower. The relative likelihood of prepayment is also about 30 percent lower.

To account for changing dynamics in the mortgage market during the study period, the models were estimated separately for origination cohorts in three time periods: 2005-2007; 2008-2011; and 2012-2014. The reduced risk of default associated with HFA loans is not observed for the 2012-2014 cohort of originations; however, less than one percent of loans in this cohort had experienced a 90-day default by the end of the study period.

Next, the working paper provides analyses of the mechanisms that contribute to lower default and foreclosure rates for HFA mortgages. Structural characteristics are considered first, including whether the loan was originated through a broker or correspondent (as opposed to a retail channel), if the loan had secondary financing, and whether the loan was underwritten with full documentation. Of the structural attributes included, the working paper shows that broker and correspondent originated mortgages have a higher risk of default, while those with secondary financing (often in the form of community second mortgages from an affordable lending program) and those with full documentation have a lower risk of default. As HFA mortgages are more likely to have full documentation, be originated in the retail channel, and include community seconds (typically associated with better credit performance than other sources of subordinate financing), all factors that improve the relative credit profile of HFA loans, including these factors can explain some but not all of the historically observed better credit performance of HFA loans.

The study also brought in data from NCHSA's annual State HFA Factbook that show whether, in any given year, the state HFA provided homeownership education and counseling, operated a direct lending program (versus originating all loans through participating lenders), or provided most of its own loan servicing or contracted it out to a Master Servicer or other private lender. The results indicate that loans originated by HFAs with direct servicing or with homeownership counseling are less likely to experience default or foreclosure. Direct lending had no observed effects. Combined, these structural attributes and service delivery practices explain about three-fourths of the HFA effect on reduced default and foreclosure. The majority can be attributed to servicing practices.

Fannie Mae says the study's results contribute to an understanding of different ways to reduce the risk of lending to LMI first-time homebuyers, beyond underwriting. As demonstrated by the recent mortgage crisis, careful underwriting clearly has an important role to play in reducing default risk. In this sample of Fannie Mae first-time homebuyers, the average credit score increased by nearly 50 points during the study period, with an average score of about 700 for the 2005 to 2007 origination cohort, to an average score of nearly 750 for the 2012 to 2014 origination cohort. Similarly, the average combined LTV (CLTV) from first lien and any subordinate liens declined from 93 percent to 87 percent. Tightening underwriting too much however, may make it difficult for otherwise creditworthy LMI homebuyers to enter the market.

One of the big takeaways from this study is the importance of borrower screening and servicing practices. Not only are HFAs more likely to require full documentation and careful underwriting, they also serve as a third-party monitor on the partner lenders originating loans through the state program, creating an additional incentive for careful screening by the lender. This highlights the potential role for policies that increase the transparency of lender origination practices and that incorporate mechanisms for monitoring by third-parties. Further, there is some evidence that preventative servicing practices (e.g., prompt contact with the borrower when a payment is missed) may contribute to the observed HFA performance gap, as loans originated by HFAs servicing their own mortgages perform better in this sample. This suggests that early intervention when a borrower misses a payment may help improve mortgage sustainability for LMI borrowers.