Fannie Mae continues to dribble out findings from its Q1 Mortgage Lender Sentiment Survey®. The latest installment is an entry on the company's FM Commentary blog on its survey's responses about experiences with TRID.

TRID, the Consumer Financial Protection Bureau's (CFPB's) TILA-RESPA Integrated Disclosure (TRID) rule which went into effect for loans initiated last October, replaced the old Good Faith Estimate and HUD-1 with a Loan Estimate for with broader and deeper details on the loan, and a Closing Disclosure with final itemized costs and fees. Most important, the rule contains strict timelines governing any discrepancies between the two disclosures, thus causing some lenders to revamp disclosure and closing processes.

The Lender Sentiment Survey was conducted among senior mortgage executives in February, a few months after the first loans originated under TRID began arriving at the closing table. Fannie Mae used the survey to examine lenders' experiences with implementing TRID requirements, including challenges and operational practices, and lenders' views about TRID's impact on the competitiveness of the mortgage industry.

Sheila Teimourian, Fannie Mae Vice President and Deputy General Counsel, reports that the effects of TRID have not been evenly distributed. The survey found that lenders faced challenges in implementing TRID with more than three-quarters calling "managing/ coordinating with third-party technology vendors and communication with key players (e.g., buyer, seller and loan officer)" the two biggest challenges.

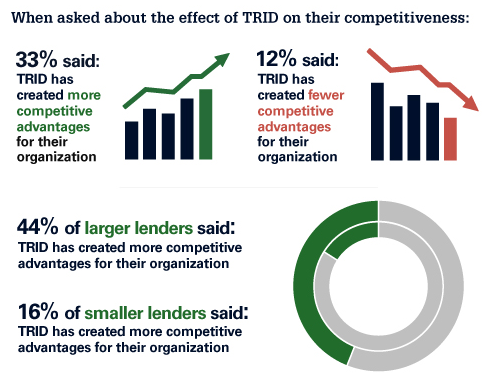

But the burden seems to have fallen disproportionately on smaller lenders while larger ones appear to have "leveraged the situation to their advantage." Teimourian says that, despite the complexity of compliance, nearly one third of lenders (and 44 percent of large ones) said that moving to TRID disclosures gave them a competitive advantage against only 12 percent who said it put them at a competitive disadvantage. Many small to mid-sized lenders said the larger institutions had the capacity to upgrade systems and the in-house compliance resources to increase efficiency and competitive advantages.

The survey indicated that complying with TRID extended closing times by an average of nearly seven days. Teimourian speculates that this time period may shorten as lenders gain experience with the requirements (and the newest origination metrics from Ellie Mae show average days-to-close for all loan types now even shorter than those pre-TRID) but coping with the demands of the spring buying season "may test even the most prepared of lenders."

Lenders reported that confidence in their ability to close a loan quickly is a more critical competitive issue than is price, although a sizeable 44 percent say they raised loan fees as a result of TRID.

The author says the survey's results largely confirm the sense that lenders and their service providers have had difficulties in complying with TRID, especially the smaller ones. Lenders remain concerned about compliance and the consequences for failure and this has also been evident from trade association and Congressional proposals in recent months.

Teimourian concludes that despite media reports in recent weeks that lenders' TRID-related concerns have abated somewhat, there is a "growing sense of unease" over interpretations and policies of due diligence firms and secondary market investors over compliance. "Finally, it will remain to be seen whether the competitive advantage that larger lenders reported as a result of TRID implementation will be sustained or whether small and mid-sized lenders will close this gap using their own resources or through innovative third-party vendors."