Freddie Mac's economists restated their February forecast in their Economic and Housing Outlook just released for March, that 2015 could be the best year for home sales and new home construction since 2007. That year there were 5.8 million sales - this year the economist forecast 5.6 million sales along with 1.18 million housing starts.

Len Kiefer, Deputy Chief Economist said, "This month kicks off the spring homebuying season. Between now and the end of June, we'll see about 40 percent of all home sales for the year. So these next few months will essentially tell us whether or not 2015 will be a good or bad year for housing markets. Overall, we're feeling good about housing and we expect this year to be the best year for home sales and new home construction since 2007." There are, the report says, several reasons to be optimistic.

Affordability

About 80 percent of metro markets in the U.S. continue to be affordable based on data through the fourth quarter of 2014. There are three drivers of affordability and house prices, the first drives, continue to rise across the country, but are still about 10 percent below their 2006 peak. Peak-to-trough comparison can be misleading as many markets experienced unsustainable highs during the last decade but fundamental drivers, like payment-to-income and price-to-rent ratios indicate that most markets have home values that are sustainable.

The second driver, interest rates, were down in January by 0.75 percent from a year earlier and, while they have rebounded, still remain low on a year-over-year basis. But, the caveat is that the third component of affordability, household income, will be the key driver of housing markets. Incomes have largely stagnated over the past decade, barely rising and, after adjusting for inflation, actually falling for the median household, but even with this driver there were glimmers of good news in the most recent jobs report. Over the twelve months ending in February 2015 the economy added nearly 3.3 million jobs, the fastest pace since 2000. And with labor markets tightening there is an expectation the wages and incomes will rise.

Demand

One key demographic segment-Millennials aged 25 to 34-have started to see their job prospects improve recently. The employment-to-population ratio for those aged 25 to 34 has increased to 76.8 percent, the highest level since 2008. Better job prospects for Millennials will drive household formation and housing demand.

There has already been an indication of housing demand in rental markets which are seeing the lowest vacancy levels since 2000 which has led to rapidly rising rents across the country - an average of 3.6 percent in 2014 and nearly 11 percent over the last three years. With rising demand and improving job prospects for younger households, rents will probably rise at or above the rate of inflation this year as well. "This may be the tipping point," the report says. "Many current renters may decide to strike while the iron is hot (mortgage rates are low and home prices not too high) and purchase a home this year.

In fact, study findings indicate that many feel it could make financial sense to buy today."

Credit Availability

Freddie Mac says it believes that these prospective homebuyers will not be thwarted by lack of financing because there is wider credit availability in the market today. In addition to low mortgage rates and rising job growth, the down payment hurdle is starting to shrink for creditworthy borrowers, including first-time homebuyers and current homeowners who want to refinance. This includes those renter households hit by rising rents who have been unable to save much for a down payment, but have good credit and a good-paying job.

Broader access to credit will be driven by a confluence of factors. The company says it expects that the new representation and warranty framework for Freddie Mac and Fannie Mae will give lenders the confidence to ease credit outlays and that newly reduced FHA mortgage premiums will help many prospective first-time homebuyers enter the market with a federally- insured loan. Finally, the new three percent down mortgage initiatives from Fannie Mae and Freddie Mac should help those qualified borrowers who have limited down payment savings buy homes with conventional financing. This will be especially important for prospective first-time homebuyers that have been sitting on the sidelines.

The economists further downgraded the forecast for economic growth in the first quarter of 2015 from the 1.0 percent decline it predicted last month to a 2.0 percent decline based on lower oil prices and overall low inflation for the quarter so far. They have also lowered the CPI forecast for the year by 0.3 percent to a 1.0 percent increase. The prediction for interest rates, which they lowered last month has been slightly increased this month. The average 30-year fixed-rate mortgage rate forecast has been upped from 3.9 percent to 4.0 percent for 2015 and from 4.8 percent to 4.9 percent for 2016.

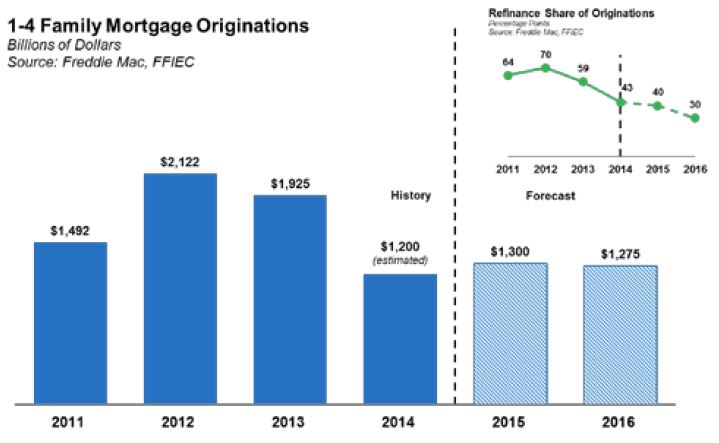

They are holding to last month's estimates of housing sales as noted above and to an increase in home prices of 3.9 percent. The forecast for mortgage origination activity is also unchanged at $1.3 trillion with a refinance share of 40 percent. For 2016, they see originations tapering a bit to $1.275 trillion as refinance share declines to 30 percent.