The Urban Institute (UI) says the surge in foreclosures predicted as the COVID-19 pandemic drove unemployment to the highest level since the Great Depression may not materialize, even when the current forbearances end. Two UI researchers, Michael Neal and Laurie Goodman, say that even vulnerable homeowners may be spared, and they think they have identified the reasons.

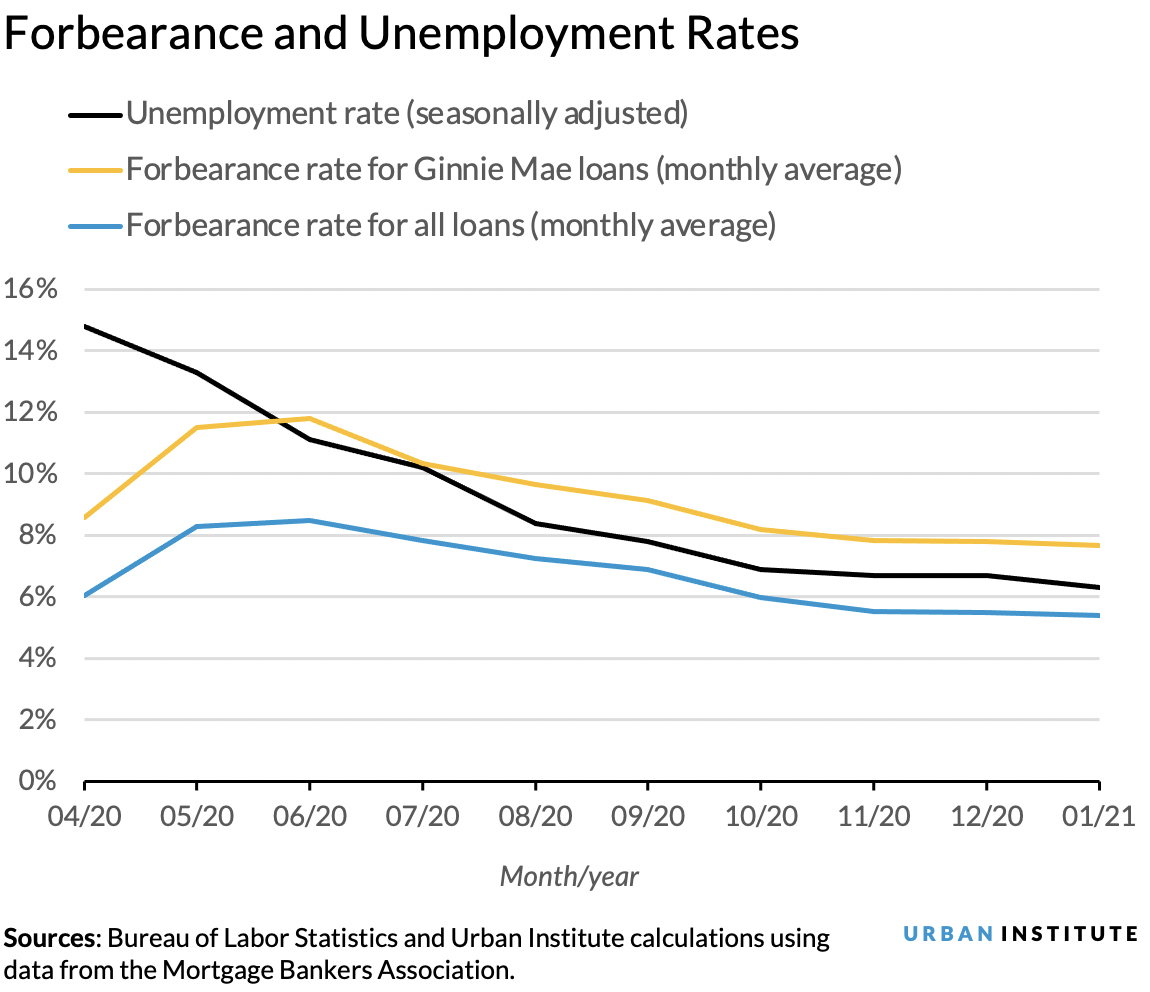

Mortgage forbearance rates peaked at 8.55 percent of active mortgage in June 2020 and began to fall when unemployment rates did. Since October, however, both unemployment and forbearance rates have flattened. This has heightened concern that many homeowners could face foreclosure later this year.

The authors say about a quarter of the 2.7 million borrowers who remain in forbearance plans are continuing to make their payments, but about 2.1 million are delinquent along with another 1.1 million homeowners who are not in plans. Forbearance is now scheduled to end mid-year and many borrowers who haven't regained their pre-pandemic financial positions may face the loss of their homes.

UI says this won't necessarily happen, even among government loan borrowers whose risks are higher due to higher-initial-loan to value (LTV) and debt-to-income (DTI) ratios, lower credit scores and lower incomes than borrowers with conventional loans. They may benefit from the large amounts of home equity that borrowers have accumulated through home price appreciation and the loss mitigation waterfalls put in place by Fannie Mae, Freddie Mac, the FHA VA, and the Department of Agriculture's Rural Housing (RH) program.

Those waterfalls, or forbearance off-ramps, allow borrowers options to pay back the past due amounts that accumulated during forbearance. The first step in the waterfall is to repay the forborne amount in a lump sum or over a short period. But, where a borrower is unable to increase their pre-forbearance payment, they can revert to their pre-forbearance payment and move the forborne amount to the end of the loan.

For an FHA mortgage, the forborne amount becomes a "soft second" or a subordinate loan on which the borrower is not required to make payments until the house is sold or refinanced. For a GSE (Fannie Mae and Freddie Mac) loan, the mortgage term is extended. If the borrower's then current income is not enough to cover their original monthly payment, they could qualify for a modification which would lower their monthly payment. Loss mitigation options are also available to borrowers who did not utilize forbearance. However, not all borrowers will qualify for a loan modification and may have to exit homeownership.

Even where borrowers are not financially stable when forbearance expires and do not qualify for a modification, those with home equity could still exit the home with their credit intact and possibly some cash in hand by selling their home and downsizing or renting. Equity also increases the viability of the waterfall because lenders are more likely to work out an alternative solution to foreclosure for a delinquent homeowner who has it.

Of the 3.2 million currently delinquent borrowers, 626,000 have government loans in Ginnie Mae securities and, because the average LTV ratio at origination is 96.5 percent for FHA purchase borrowers, 100 percent for VA loans, and 101 percent for USDA loans, these borrowers will generally have less equity than those with GSE loans.

Goodman and Neal developed a methodology to estimate the home equity for government loans that shows that even among delinquent borrowers less than 1.0 percent have negative equity and 5.5 percent are near negative, a total of 3.6 percent. In the aftermath of the Great Recession, the latter number was approximately 30 percent.

Further, they found the average government loan borrower has 22 percent equity. Most of the 3,771 delinquent or forborne borrowers in negative equity are VA borrowers (2,817), many of which had origination LTVs of 100 percent. Another 1,000 in negative territory are evenly split between FHA and RH. Nearly all the negative equity loans were originated from 2018 to 2020, most in 2020.

The additional 5.5 percent of borrowers with near-negative equity or less than 5 percent will have none left after the transaction costs of selling. They have little incentive to sell by themselves.

Home price gains (60 percent from early 2012 through late 2020) have pushed home prices up above their pre-recession peak by an average of 19.7 percent, but those increases have been uneven. Many areas still have prices below the 2005-2006 levels. The share of mortgages with negative equity range from 0.1 percent in several states to highs of 1.8 percent in Wisconsin and 1.4 percent in Illinois. The share of non-current borrowers with negative equity or near-negative equity are mostly in the single digits, with only Wisconsin, Illinois, and Alaska exceeding 10 percent. These may be the states that do see significant numbers of foreclosures.

The authors say that even as improvement in the forbearance rates have slowed along with the decline in unemployment, they still expect far fewer foreclosures than during and after the Great Recession. Many of today's homeowners in distress have both significant equity buffers and improved loss mitigation tools. The extensions in forbearance terms announced earlier this month will give struggling borrowers more time to benefit from improved employment prospects as the economy recovers and to build an equity cushion; this is particularly critical to homeowners without equity. A further extension in forbearance may well be necessary.