In a hearing on Thursday before the House Financial Services Committee, Edward L. Golding, Principal Deputy Assistant Secretary of the Department of Housing and Urban Development (HUD) said that the value of the Federal Housing Administration's Mutual Mortgage Insurance (MMI) Fund has improved by $19 billion in the last year. The Fund fell into negative territory during the housing crisis, battered by poor performance of its guarantee portfolio.

Golding said the Fund increased from $4.8 billion in FY 2014 to $23.8 billion in the most recent year, a total of $40 billion in growth since 2012. The Fund, which is required by Congress to maintain a capital ratio of 2.0 percent, has improved since 2012 from a negative 1.44 percent to a positive 2.07 percent. Further, the Independent Actuary's 2015 review predicts that the Fund will finish 2016 with a ratio of 2.77 percent.

Golding said the underlying fundamentals of the FHA portfolio are strong and show positive performance in credit quality, reduced delinquencies, and higher recoveries on distressed assets. The early payment delinquency (EPD) rates are typical of the better credit quality of new business. The EPD give an early warning of problems, measuring the rate at which loans experience delinquencies in their first 90 days. The EDP rates for FY2010 through FY2015 vintage loans are less than 20 percent of those for the 2007 and 2008 vintages.

Over the last four years the serious (90+ day) delinquencies have fallen by 35 percent, a nearly $35 billion reduction in the seriously delinquent portfolio and recoveries on defaults have improved by 43 percent since 2013.

As the performance of the portfolio continued to improve, FHA was able to weigh its premium pricing structure against the need for expanded, affordable access to credit in the market and last January announced a reduction in the annual mortgage insurance premiums (MIP) on its Single-Family Forward loans. When the reduction was announced, FHA told stakeholders it was expected to introduce 250,000 new borrowers into the market over a three-year period, an average of roughly 83,000 per year. This new activity would come from previously underserved potential borrowers - best represented as those with credit scores at or below 680.

Golding said instead, in the first twelve months since the MIP reduction 106,000 additional borrowers with credit scores at 680 or below received an FHA loan, exceeding initial projections. The number of purchase endorsements increased by 27 percent-growing from 594,997 purchase loans in FY 2014 to 753,389 in FY 2015 and refinance activity, which had declined sharply in FY 2014, rebounded by 90 percent between FY 2014 and FY 2015.

In the years since the crisis began, FHA has made substantial changes to its credit guidelines to improve and strengthen the position of the Fund. To further align credit standards with acceptable risk levels, FHA also implemented changes such as:

- Instituting a 10 percent down payment requirement on loans with credit scores less than 580.

- Strengthening manual underwriting guidelines to discourage extreme risk layering.

- Working with Congress to end risky seller-funded down-payment assistance practices.

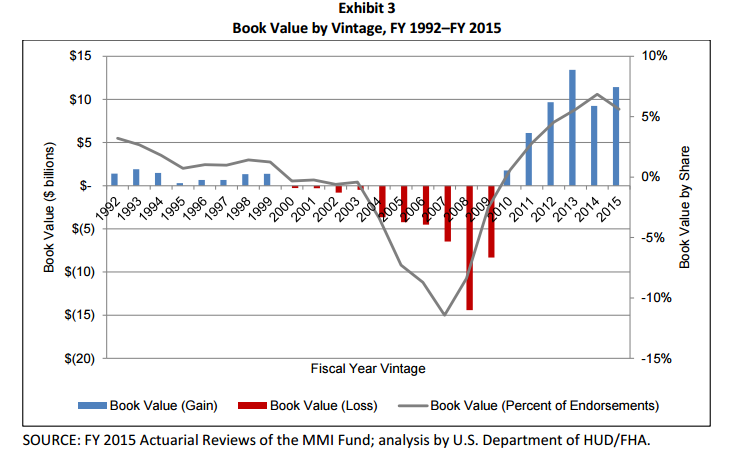

These changes significantly improved the quality of FHA's incoming business, and slowly but steadily increased the value of the Forward portfolio. While the overall effect of any individual vintage year on a $1 trillion portfolio is limited, a steady accumulation of high-quality loans over several years improves the Fund. The 2005-2008 loan vintages that account for the bulk of FHA's more recent losses now represent only 10 percent of the Forward portfolio with more recent loans performing at or above expectations.

Golding said that in recent years, although a small part of the total portfolio, HECM loans - the so-called reverse mortgage program for seniors - has had a significant impact on the MMI Fund. In FY 2015, FHA's HECM program helped 57,990 senior households to age in place, an increase of 6,374 borrowers from FY 2014. Thirty-nine percent of HECM borrowers were single females and 22 percent were single males, and multiple borrowers comprised 39 percent of HECM borrowers, the same level as FY 2014. Additionally, the borrower's average age has declined, from approximately 77 in FY 1990 to around 72 in FY 2015.

He said while the value of the Forward portfolio has steadily improved in value over the last three years, HECM valuations have exhibited more variability. Since the program is dependent on the market value of the property used as security, the HECM portfolio can experience significant swings in value year over year as the market factors that influence the present value of future home price change. The changes in these market factors, in turn, alter the projected losses on and values of loans in the portfolio.

HECMS are sensitive to changes in economic assumptions because they are held longer (an average weighted life of 15 years versus about six for Forward loans) thus accounting for greater discounting and greater rate sensitivity over time. Also, while FHA is only the guarantor of the Forward portfolio it is likely to own the proceeds of selling a HECM mortgaged home making house price appreciation a major consideration.

Still Golding maintains the HECM program is fundamentally sound and has benefitted from policy changes Congress permitted it to make in 2013 to improve sustainability and consumer value including changing the manner in which borrowers can take draws from the loans and altering the due on death clause to benefit non-borrower surviving spouses.

Recapping FHA's overall performance over the past year Golding said:

- FHA endorsements accounted for 19 percent of the total purchase mortgage market and 14 percent of refinancing. It endorsed 1.12 million mortgages through its single family program. By dollar volume, 66 percent of FHA mortgages were for purchase and 34 percent were for home refinances. These mortgages went to borrowers with an average credit score of 680 and represent an average loan size of $190,928 for all mortgages, and an average loan size of $186,176 for purchase mortgages.

Exhibit 1 - endorsements by loan type p 2

- In FY 2015, 82 percent of all FHA purchase originations were to first time homebuyers - a total of 614,148 loans. This is consistent with FHA's endorsement trends over the past 15 fiscal years, during which approximately 80 percent of annual purchase endorsements were for first- time homebuyers. Over the course of its 81-year history, FHA has funded approximately 13 percent of total market mortgage originations but more than 50 percent of all first-time homebuyer market purchase mortgages.

- In FY 2015, a third of FHA mortgages went to minority buyers, consistent with long-term trends. The proportion of FHA purchase endorsements to Hispanic and African-American borrowers remained steady at around 17 percent and 11 percent respectively.

- FHA served borrowers in every state, the District of Columbia, Puerto Rico, and the U.S. Virgin Islands. Because credit policies and premiums do not vary by geography, FHA provides a stabilizing force across jurisdictions, ensuring broad credit access during localized downturns.