Blackstone Group has disclosed that it has secured Fannie Mae's backing for a mortgage backed by some of the single-family homes it purchased, principally from bank-owned real estate inventories (REO), during the housing crisis. According to the Urban Institute (UI), which produced a Note on the transaction, the loan "marks the first time a government-sponsored enterprise (GSE) has facilitated financing for a large institutional operator of SFR (single-family rental) properties."

Blackstone, a private equity company, operates Invitation Homes (IH), the largest single family rental operator in the U.S. which purchased an estimated 48,000 single-family homes across the country. However, UI was not alone. Frank Nothaft, Senior Economist at CoreLogic estimated recently that, of the approximately 6.3 million homes that were foreclosed during the financial crisis, three million were turned into rental properties. While many of the homes were turned into rentals by small investors, huge institutional investors like Blackstone also actively acquired them. UI puts current institutional ownership at 300,000 units.

The Blackstone/IH 10-year, $1 billion loan will be originated by Wells Fargo, securitized and sold to investors with the Fannie Mae Guarantee under what UI says is a pilot program. The UI says this development is noteworthy because it sends a signal the company is seriously considering entering this space.

They won't exactly be pioneers. Morgan Stanley says some of the large investors began to securitize their portfolios early on; by the fall of 2015 about 90,000 properties had been securitized for $12 billion. Some big investors assisted smaller investors to create pools of their properties then securitized them. Morgan Stanley says, with few exceptions these offerings have carried AAA ratings and have performed accordingly.

UI says the GSE role in the rental market has historically focused on multi-family properties or to a lesser extent, to properties owned by smaller investors defined as those owning ten or fewer homes. Fannie Mae has typically limited financing to small investors at 10 properties and Freddie Mac to six. Clearly, this doesn't work for institutional investors who own thousands.

The Note's authors, UI analysts Laurie Goodman and Karan Kaul, say that "It makes sense, policy-wise, for the GSEs to enter this space." But they also stress that a framework should be used for subsidizing single-family rental debt that includes some specific measures:

- The benefits of a taxpayer guarantee are used in a manner similar to that in the GSE multifamily arena to increase availability of rental housing to those earning 100 percent of the area median income (AMI) or less, and

- Allowances are made to allow non-institutional players such as small investors, community-based organizations, and mission nonprofits to compete effectively.

They say that the Federal Housing Finance Agency (FHFA), regulator and conservator of the GSEs, "should articulate a clear role for the GSEs in the SFR market and work to fulfill that role in a manner that attracts new investment while meeting the demand for workforce housing," the same case that justifies the GSEs existing role in financing multifamily housing.

UI says the GSEs financed about a third of all multifamily originations in 2015. While there are no explicit affordability requirements, 80 to 90 percent of this financing has always been for housing affordable to those earning 100 percent of area median income.

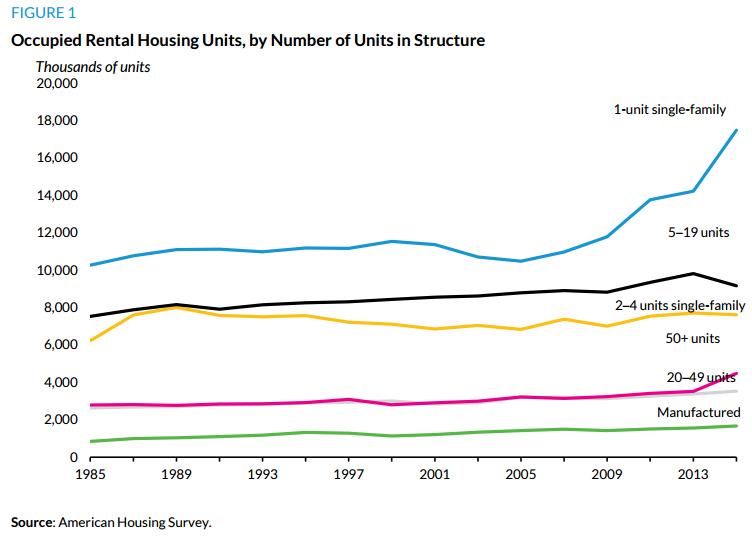

Multifamily buildings, (defined by the GSEs as buildings with five or more units) are a critical source of rental housing, but single-family homes composed 40 percent of the rental stock in 2015 per American Housing Survey data. An additional 17 percent is two-to-four unit structures, which are also classified as single-family. Thus, 57 percent of the US rental housing stock is single-family, and 43 percent is multifamily.

This is not new. One-unit structures have always been the largest component of the total rental housing stock, but as mentioned above, that increased by 67 percent between 2005 and 2015, to 17.5 million units. This reflects not only foreclosures, but the rapid increase of renter households.

Early on, these buyers used cash and then later both securitization and bank lending.

UI says that the homeownership rate is likely to decline over the next 15 years. As the bulk of net new households will be renters and given the acute shortage of rental homes and rapidly rising rents, investing in more rental housing is "a no-brainer." With single family homes being the largest and fastest growing segment of the housing market it offers the most promise in addressing the problem of rental affordability.

Thus, Goodman and Kaul say they are sure it makes sense for the GSEs to finance SFR properties. "Access to stable, long-term and nonfleeting financing-which allows institutional landlords (both for-profit and nonprofit) to purchase, hold, and stabilize the properties, and run the stabilized properties as a business, rather than flipping them- will be crucial in preserving their long-term commitment to this space."

This pilot is a good first step as it helps Fannie Mae understand the economics, opportunities, and risks of what is an entirely new market for the company and a pilot was necessary to understand the risks and challenges and gather robust property and rent data. The SRF market is very new and does not provide the large performance, borrower, and property level data sets with which the GSE's have familiarity and experience. As the largest operator in this space, IH had these datasets which allowed Fannie to conduct necessary due diligence. Additionally, since this was technically a refinance, there was no time pressure, allowing Fannie to vet the deal carefully.

Fannie Mae has imposed rigorous safeguards that require the borrower to retain a 5 percent first-loss position and the 95 percent guarantee is reinsured under a loss-sharing arrangement with Wells Fargo. While precise terms for this loan are not available, Fannie Mae's typical arrangement with multifamily lenders is for the lender to share one-third of the loss while Fannie absorbs the remaining two-thirds on a pari passu (equal footing) basis.

Fannie's risk is further lessened by the low loan-to-value (LTV) ratio of the loan which is refinancing earlier (2014) debt. At least one of the earlier loans had an original LTV of 75 percent and given appreciation over the last three years this could put the current LTV (without considering amortization) at 63 percent.

UI says this three-stage mitigation framework - 5 percent first loss, Wells Fargo risk sharing, and low LTV - should offer Fannie Mae and taxpayers greater loss protection than they receive on typical multifamily loans. The several safe guards are fully warranted given this is a first deal in the space. It is also the first time Fannie Mae has shared credit risk with an owner of rental properties instead of with approved and carefully monitored multifamily lenders.

The authors say their view that the GSEs should support the SFR market raises the question of how they should do so. This pilot transaction raises questions that should be addressed before going further.

1. What affordability criteria should be imposed on this type of financing? Clearly the GSE financing will reduce borrowing costs and improve funding stability for institutional investors which should stimulate further investment. But the mission of improving availability of rental housing to lower income renters could be increased by making such financing available to community and mission-based non-profits with the scale and skills but who lack capital. It should also be considered that institutional buyers compete with potential owner-occupants, especially first-time buyers. "This suggests that taxpayer-backed financing for institutional SFR owners should be accompanied by explicit affordable housing requirements." For example, requiring landlords to rent a certain percentage of units to renters earning 100 percent of the AMI or less or requiring them to accept Section 8 vouchers.

2. Should GSE financing be extended to the purchase of vacant or to-be-built SFR properties? The IH portfolio is currently 95 percent occupied with a well-established rental history, making the pilot a relatively low risk deal. There could, however be instances where it could take time to repair and rehabilitate properties before they can be rented out and financial and operating data will be limited, presenting more risk to the GSEs. At the same time, financing such properties would make it easier for smaller operators and nonprofits, many of whom are mission specialists in neighborhood stabilization but lack financing, to play a bigger role in this market.

3. What sale restrictions should be imposed on SFR homes receiving taxpayer backing? Over the normal course of business, institutional landlords may choose to sell some properties, especially those that are less profitable. It is also possible that landlords will come up with programs to sell properties to tenants. Should this activity be permitted and what restrictions should be put in place? At the very least, it seems that the use of land contracts or similar arrangements should be strictly prohibited.

(As an aside, Blackstone as well as Starwood - another big SFR investor - have previously announced their intention to liquidate about 5 percent of their portfolios each year and Blackstone/IH has initiated a program to sell units to its tenants saying it reduces their marketing time and costs.)

4. How should SFRs be treated in the context of housing goals and multifamily caps? If these properties are in underserved markets, should they count toward the GSEs multifamily housing goals? Similarly, should SFR properties that are affordable to renters at the 60 percent AMI level be exempt from the GSEs' multifamily caps?

5. To what eligibility and property maintenance criteria should SFR owners be held accountable? If more of these IH type transactions are drawn, the borrowers should be subject to standards that include transparent and clearly articulated property maintenance requirements.

UI says its views this pilot transaction as an important first step and assumes there will be more such deals in the future. If so, as they move from pilot to program, FHFA should work with stakeholders to evaluate the role GSEs should play in this market, how that role can increase the availability of rental housing, and ultimately construct a scalable program to do exactly that.