How will the economic philosophy that was altered by the last election actually evolve into policy? The is the question raised by Fannie Mae's Economic and Strategic Research Group, headed by Doug Duncan, Senior Vice President and Chief Economist say, in their January economic forecast. With limited information available on the economic priorities of the Trump Administration, and those of the House and Senate also uncertain, "establishing reasonable estimates of the nature and sequencing, much less the magnitude, of policy changes [is] unusually challenging." Thus, the company's economic team says its theme for 2017 is "Will Policy Changes Extend the Expansion?"

Incoming data supports the company's expectations that the strong growth in the third quarter was unsustainable and the current estimate is for the economy to continue growing below potential at about 2 percent through 2017. If so, in March it will become the third longest and the weakest expansion since World War II. There are minor signs of inflation, consumer debt is rising, and business investment languishes. Some potential members of the Administration have made statements in support of tax reduction and regulatory relief but there are also comments about tightening trade rules which may work against an improved business environment. The economists say that while they believe that some form of fiscal stimulus and deregulation might happen later this year or next year that could boost growth, they have not included any new federal policies in their baseline forecast.

So how long will the expansion last? Fannie Mae says it has not changed its forecast to reflect the uncertain nature of policy actions but the timing and content of changes "could make the difference between an accelerating economy and a recession." In either scenario, its expectation is that housing will cope reasonably well.

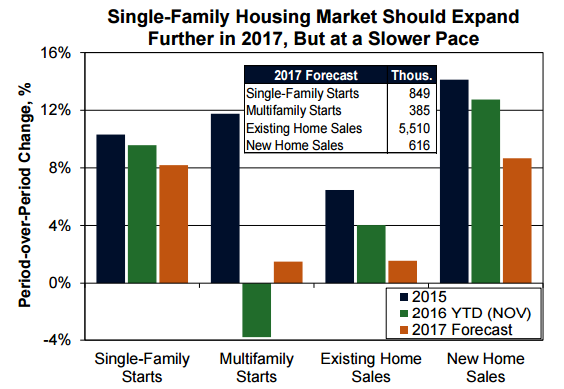

A year ago the forecast was for the housing market to face affordability challenges as the expansion moved into its late cycle. Strong home price gains that outpaced income growth, rising interest rates, and elevated rents and the impact on savings would particularly affect first-time buyers. Fannie Mae projected a moderation in home sales from the 2015 increase of 7.0 percent to 3.7 percent. Despite the surge in interest rates after the election, the year's average was the lowest since Freddie Mac became to keep score in 1972. Fannie Mae says it also underestimated price appreciation and inventories of both new and existing homes remained tight, putting pressure on prices.

Existing home sales hit an expansion high in November but pending home sales, which typically predict upcoming sales one to two months later, fell substantially, suggesting an impact from rising interest rates. Price gains appear to have been stronger in 2016 than the prior year and inventories remained tight all year, partially because of a dwindling number of distressed sales coupled with a downtrend in mobility rates with the share of Americans changing residences falling to an all-time low.

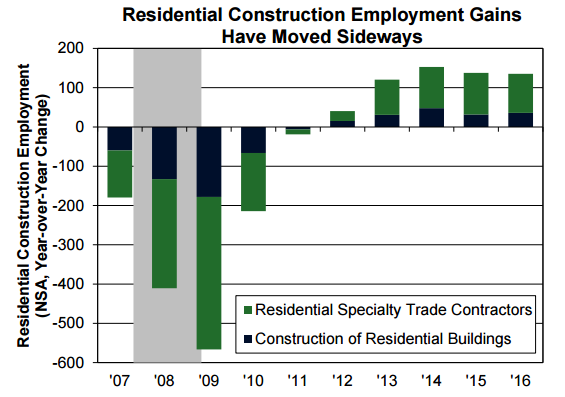

Residential spending rose in November, confirming expectations of a strong rebound in residential investment in the fourth quarter after two straight quarterly declines. However, for all of 2016 homebuilding was a disappointment; housing starts grew at just half the 10.8 percent pace in 2015 rather than meeting expectations that growth would hold steady. Lack of skilled labor and available building sites along with the increased cost of mortgage lending contributed to the poor homebuilding performance.

Homebuilder confidence improved after the election based on expectations of deregulation, but lender sentiment as measured by Fannie Mae's quarterly survey, eroded. A majority of lenders cited unfavorable mortgage rates for a worsening near-term outlook. Consumer sentiment expressed in the National Housing Survey declined in December for the fifth consecutive month with rising interest rates tamping down home purchase sentiment.

Mortgage rates, after rising for eight consecutive weeks after the election and reaching the highest level since April 2014, have now backed off and have fallen more than 20 basis points since the first of the year. Fannie Mae expects them to rise only gradually to about 4.3 percent by the fourth quarter of 2017. There is a risk that rates could rise faster but if income growth also strengthens, then the housing recovery can continue as expected.

Demographic factors favor housing, with research showing that oldest Millennials have begun to buy homes and are closing the homeownership attainment gap with their predecessors. There will be further slowdowns in the accelerating pace of home sales and single-family starts this year but a gain for multi-family construction starts after a decline in 2016, the first in seven years.

The company has revised higher by about $30 billion its forecast for refinance originations in the fourth quarter of 2016 and modestly downgraded the forecast for 2017. Projections for purchase originations are slightly higher due to stronger existing home sales and home price gains but moderated by weaker housing starts and new home sales than predicted earlier.

Mortgage originations for all of 2017 will be down 19 percent from an estimated $1.94 trillion in 2016 to $1.57 trillion as the decline in refinancing outpaces the increase in purchase originations. The refinance share is expected to decline from 48 to 33 percent.