Adjustable rate mortgages have lost much of the popularity they enjoyed in the mid-2000s and Freddie Mac's 28th Annual Adjustable-Rate Mortgage Survey for 2012 found that hybrid ARMs, especially the 5/1 hybrid are the most popular ARMs offered by lenders.

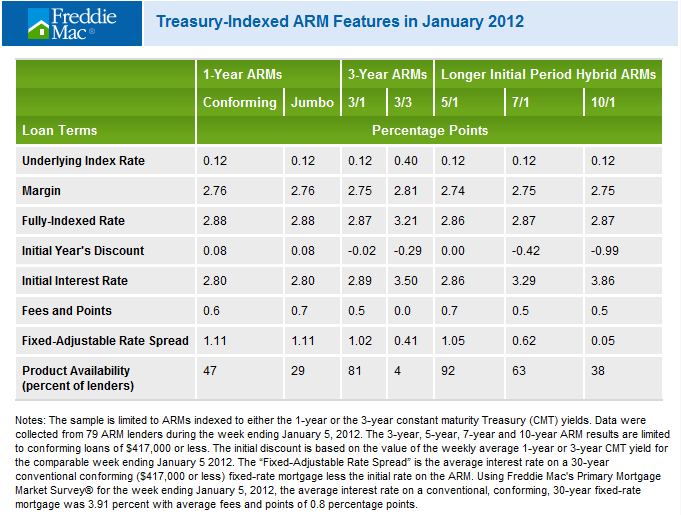

With ARM initial period rates at historically low levels, reflecting, in part, the low levels of the Treasury yields that are used as indexes, the survey, conducted between January 3 and January 5, found there was, in fact, little difference in the initial interest rate for the traditional one-year adjustable, the 3/1 hybrid and the 5/1 hybrid. The longer-term products such as the 7/1 and 10/1 hybrids were, because of their long initial fixed-rate period, priced closer to the rate on a 30-year fixed rate mortgage.

The 5/1 hybrid ARM continued to be the most popular loan product (sic) offered by lenders and nearly all of the ARM lenders who participated in the survey offered such a loan. Following the 5/1 in popularity were the 3/1 and the 7/1. Less than one-half of the lenders now offer the one-year adjustable, and only 4 percent offered a 3/3 ARM that adjusts once every three years. The 7/1 and 10/1 ARMs, were available from 63 percent and 38 percent of the survey participants, respectively.

The survey found that the interest rate savings for the 5/1 hybrid compared to the 30-year fixed-rate mortgage was about 1 percentage point in early 2012. This was virtually unchanged from the savings found in the January 2011 survey.

Of the 121 ARM lenders surveyed, 65 percent offered loans tied to constant-maturity Treasuries, down from 71 percent in 2011; the remaining offered products tied to future rates indexed to the London Interbank Offered Rate (LIBOR). With the onset of the debt crisis in the Eurozone, the 1-year LIBOR rate less the 1-year constant-maturity Treasury yield peaked over the week ending January 6 at over 1 percentage point, compared to around 0.5 percentage points over the same week in 2011. As a result, 1-year LIBOR indexed ARMs may have adjusted up or did not adjust materially down compared with Treasury-indexed ARMs. The uncertainty over LIBOR movements may have led some current borrowers to avoid LIBOR ARMs.

Frank Nothaft, vice president and chief economist, Freddie Mac said of the survey findings, "Homebuyers have shied away from ARMs, particularly traditional 1-year ARMs, because they are wary of the risk and uncertainty. Borrowers who have taken out ARMs generally prefer hybrids, because these products include an extended initial period where the interest rate is fixed. ARMs today are financing just over 10 percent of new home-purchase loans. In June 2004, ARMs hit a peak share of 40 percent of the home-purchase market but by early 2009, that share had fallen to just 3 percent, according to the Federal Housing Finance Agency. We are expecting ARMs to gradually gain back some favor with mortgage borrowers rising to a 14 percent share of the home-purchase market in 2012."