A recent study by Fannie Mae found some distinct differences in the ways higher income earners look for a mortgage compared to lower income earners. Steve Deggendorf, Fannie Mae's Director of Business Strategy looked at the shopping behaviors of the two groups through the company's regular National Housing Survey during the second quarter of 2013.

Deggendorf not only found distinct differences in the shopping behaviors of higher and lower income mortgage borrowers but also found opportunities for online tools that could improve the ability of all borrowers to shop for a mortgage. Careful shopping, he says, "could help mortgage borrowers obtain better outcomes, including lower costs, fewer surprises at the loan closing table, and higher long-term satisfaction with their choices."

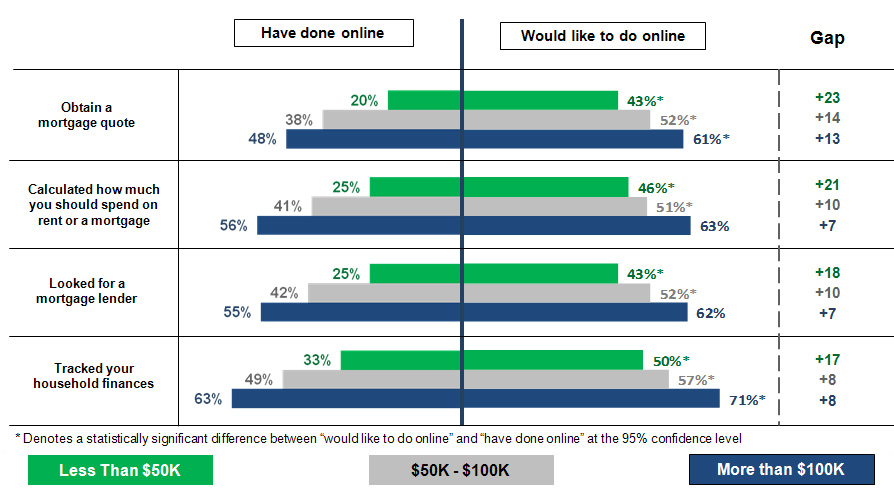

The study defined the two income groups as those with family incomes below $50,000 and those above $100,000 and found that in general the higher income borrowers were more likely to rely on their own mortgage calculations and use of tools to assess how and how much to borrow. They were also more likely to pick a lender based on its competitiveness. The lower income group was more likely to rely on real estate agents, mortgage lenders, family, and friends for advice and recommendations. In addition the higher income group more often said that a better ability to compare multiple loan offers would make shopping easier while the lower income respondents wanted earlier to understand loan terms and costs.

The higher income group tended to use online shopping about twice as much as the lower income group however all groups would like to increase their usage indicating that the Internet will likely play a growing role for all borrowers and that there is a need for shopping enhancements.

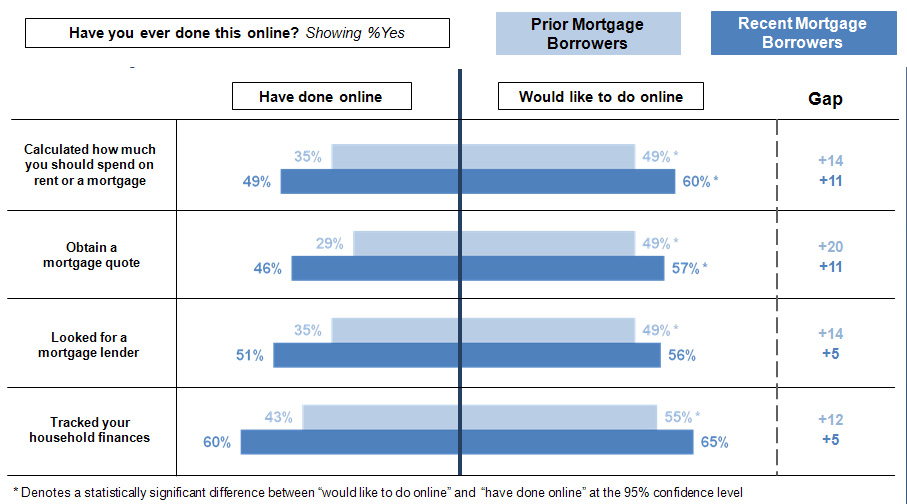

The study found that those who have obtained a mortgage in the last three years were more likely to have used technology in their mortgage shopping than borrowers from an earlier period. Deggendorf said this could be partially explained by the growing use of on-line tools in general but also by recent borrowers having higher income and education levels than earlier ones.

Despite a general increase in the use of mobile technology (tablets and smart phones) respondents said they tended to rely on their personal computers when shopping for financial products and were also likely to continue to do so. Respondents also indicated that social media would probably continue to play a small role in mortgage shopping as is currently the case.

Deggendorf says many researchers have observed that the use of online research and mobile tools enable consumers to obtain product reviews and compare prices both at home in in stores. He says that only time will tell what inroads enhanced technology tools allow us to make in improving outcomes for more complex activities such as mortgage shopping. They could, for example, offer real-time information and education where and when needed such as when house-hunting or sitting face-to-face with a lender. "Enhanced online tools, especially given the aspiration to use them much more often in the future, could help consumers of all incomes to become better mortgage shoppers and achieve better outcomes by addressing the issues they think will make the process easier, such as enhancing their understanding of mortgage terms and costs and their ability to make simultaneous comparisons of loan terms from multiple lenders."