Treasury yields have rallied close to calendar year lows Monday morning as euro zone debt concern weigh on investor sentiment.

Fitch Ratings cut its credit rating on Greece by three notches into junk territory late Friday, while Standard & Poor's affirmed Italy's A+ but cut its stable outlook to negative. The downgrades, along with weak manufacturing data from China, prompted a flight to quality in early trading. The 10-year Treasury was quoted at 3.10% at 8am Eastern Time, five basis points lower than Friday's close. The 2-year note was at 0.50% and the 30-year bond was yielding 4.27%. And the FNCL 4.0 was up 7/32 to 100-10 while the FNCL 4.5 was trading 5/32 higher at 103-19.

Asian stocks fell abruptly on China's softer than anticipated data: the Shanghai index finished 2.9% lower Monday, while shares in Japan and Hong Kong fell 1.52% and 2.11%, respectively. U.S. equity futures are following the trend - S&P 500 futures are down 11.75 points at 1,316 and Dow futures are 120 points (-0.96%) lower at 12,346.

Oil prices are unwinding with light crude prices falling 2.38% to $97.80, while gold prices are flat at $1,508.90.

Key Events This Week:

Monday:

8:10 - James Bullard, president of the St. Louis Fed, speaks about monetary policy at the Mineral Area College Cozean Foundation in Park Hill, Mo.

Treasury Auctions:

11:30 - 3-Month Bills

11:30 - 6-Month Bills

Tuesday:

2:00(am) - Eric Rosengren, president of the Boston Fed, speaks to a conference on a framework for financial stability and regulatory priorities in St. Petersburg, Russia.

8:25 - Fed governor Elizabeth Duke speaks on financial education at Boston University.

9:50 - Thomas Hoenig, president of the Kansas City Fed, speaks to the 29th Annual Monetary and Trade Conference in Philadelphia.

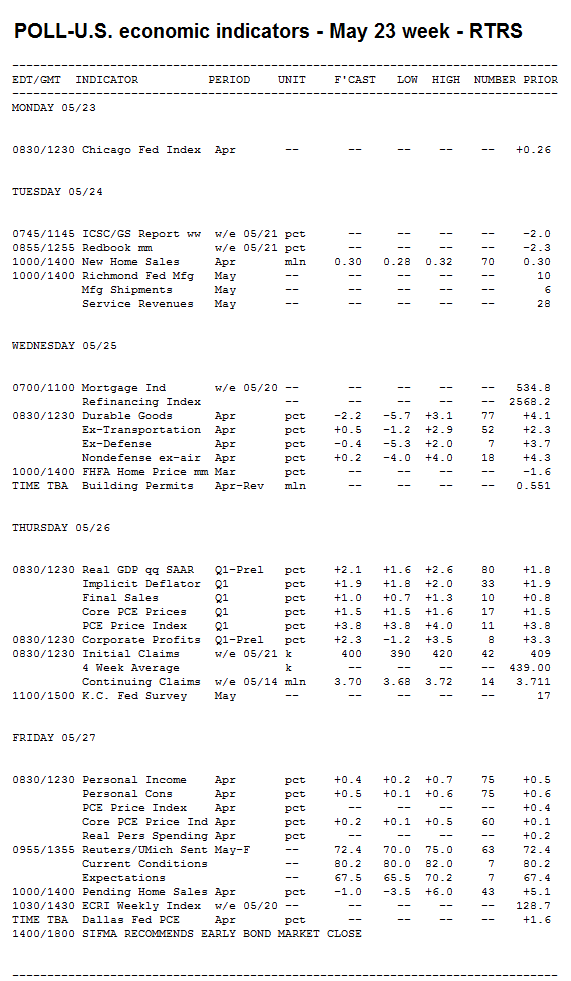

10:00 - The 11.1% gain in New Home Sales for March was the first increase since December, but economists don't anticipate a repeat in April. The consensus forecast calls for the 300k annual pace of sales to remain flat, reflecting the dismal state of the industry. That pace is 40% lower than the 40-year average of 500k, according to economists at BBVA.

"March new home sales bounced hard off of February lows, proving in large part that the prior month's dismal performance, the weakest reading in the 50-plus year history of data collection, was a one-time drop," said economists at Janney Capital Markets. "Despite the bounce from those lows, we hold no expectation that new home sales will rise meaningfully in April, or really at any point in the near future."

Janney points out that new home prices - which increased 2.9% in March -have held at "much higher levels" than trends among existing home sales. For instance, prices in this index have dropped 12% since mid-2006, whereas existing home prices are off by 29%.

"Based on this builder hesitancy to lower prices, a trend which we see continuing, the ratio of new to existing home sales seems unlikely to recover to pre-crash levels until at least the middle of the current decade," they predict. "That timeframe coincides with heavier debt maturities at the major homebuilders, maturities which may encourage said builders to raise additional cash through prices cuts and greater property sales."

Economists at Nomura Global Economics made the same point: "Owing to the incredible amount of foreclosure and short sales in the market for existing homes, the new-to-existing-home-price-ratio is simply too wide for new home sales to compete on price. New home sales have hit bottom, but as yet are not exhibiting any measurable upward trend."

1:20 - James Bullard, president of the St. Louis Fed, speaks to the Cape Girardeau West Rotary Club in Cape Girardeau, Mo.

Treasury Auctions:

11:30 - 4-Week Bills

1:00 - 2-Year Notes

Wednesday:

8:30 - New Orders for Durable Goods jumped 4.1% in March, but economists expect most of that to be erased in April due to weak orders from Boeing. The median estimate is -3%, with some economists predicting a decline as big as 5.7%. According to forecasters at IHS Global Insight, orders excluding planes and turbines should climb "a token 0.2%, after a solid 3.9% gain" the month before.

"Durable goods orders likely plummeted on weak transportation and a seasonal quirk that depresses the first month of each quarter," said economists at Citigroup. "We think the underlying path of orders still is rising [but] special factors likely caused a dramatic retreat in durable goods orders in April after the strong March report."

Citi noted aircraft orders fell sharply and auto orders could be lower due to supply disruptions in Japan.

"In addition to the transportation weakness we have observed an inter-quarterly seasonal pattern in which core capital goods show initial weakness and subsequent rebound," they added. "There has been an outright decline in core capital goods orders in the first month of the past 11 quarters, despite having a positive trend since the end of the recession."

1:00 - Narayana Kocherlakota, president of the Minneapolis Fed, speaks to the Chamber of Commerce in Rochester, Minnesota.

Treasury Auctions:

1:00 - 5-Year Notes

Thursday:

8:30 - Economists expect some upward revisions to first-quarter GDP, thanks to faster inventory accumulation and better trade relations than first projected. But even the most optimistic forecasts don't expect growth to match the previous quarter. The consensus looks for a growth rate of +2.1% from January to March, up from +1.8% in the initial estimate and compared with a 3.1% uplift in Q4-2010. Estimates range from +1.9% to +2.6%.

"The first-quarter slowdown in growth was exaggerated by bad weather and by a sharp drop in defense spending, but there is no question that the economy has entered a soft patch," said economists at IHS Global Insight.

"Most of the recalibration is in inventory and trade," wrote analysts at Citigroup. "The most notable change in this report will be a recasting of foreign trade. The monthly trade report for March showed much faster growth of both exports and imports than the Commerce Department had assumed. While the trade balance, and therefore the contribution to first quarter growth, was only marginally altered, the new figures imply a faster pace of demand growth both here and abroad."

8:30 - Initial Jobless Claims are expected to come in above the 400k mark for a sixth consecutive week in the period ending May 21. In last week's report, weekly claims fell 29k to 409k; this week economists expect further decrease, but only to 405k.

"Initial jobless claims probably remained close to 400,000 after the effects of a series of special factors in April and early May boosted the level," wrote analysts at Citigroup, noting that flooding along the Mississippi River could result in more claims than anticipated

"There may be a surge in auto-related filings during the Memorial Day week as two major Japanese producers have announced temporary closures," they added.

Treasury Auctions:

1:00 - 7-Year Notes

Friday:

8:30 - The Personal Income & Outlays report should show some optimistic trends with income and spending each rising amid benign inflation. Income is expected to rise 0.5% in April, compared with a 0.4% advance in March. Spending is forecast to jump 0.6% following a 0.4% gain. The core PCE index - the Fed's preferred inflation measure - is expected to slow to 0.1% from 0.2% a month before.

"Consumer incomes are slowly recovering from the depths of the recession, though as is the case with most economic phenomena, the uptrend is much slower than the downdraft," wrote analysts at Janney. "Although firms are once again hiring, wages have yet to feel any meaningful upward pressure, which is limiting the core improvement in incomes to the pace at which joblessness falls."

Janney points out that much of the spending increase is owed to higher energy costs, "as the average price at the pump leapt 7.5% in April."

Moreover, they expect headline inflation to rise "nearly 0.4%," so the growth of consumer spending will be "barely above water in inflation-adjusted terms."

9:55 - Does anyone expect Consumer Sentiment to rise? Not so much. The preliminary index for May rose 2.6 points to 72.4, and economists think that pretty much sums up the month. The consensus forecast is 72.5, and forecasts lie in a narrow range from 71 to 73.

"Recent news has been a mixed bag," noted economists at IHS Global Insight. "April payrolls and average hourly earnings improved, but the unemployment rate increased to 9.0%. Stock market volatility and still-high gasoline prices continue to hurt U.S. consumers despite the recent drop in commodity prices."

10:00 - The Pending Home Sales Index is itself a forecasting tool of existing home sales. As such, few economists make predictions or provide commentary. But it won't be ignored. The index looks at sales contracts that have been signed, but not finalized, thereby providing an early picture of the housing sector. The March index jumped 5.1%, but the pace remained down 11.4% from a year ago. The April index seems unlikely to repeat such a strong gain.

SIFMA recommends a 2pm bond market close in observance of the Memorial Day holiday.