The week ahead holds a wide variety of data and events.

The bond market is focused on inflation reports and Treasury auctions while stock investors prepare to kick-off corporate earnings season. Also on the market's radar is ongoing political debate on the U.S. budget plan. Even after a government shutdown was avoided late Friday night with a compromise that will cut some $38.5 billion in spending for the last six months of the current fiscal year, major ideological party differences are still present and neither party seems willing to give in to larger concessions. President Obama is anticipated to deliver a major speech Wednesday to lay out how the federal budget deficits can be curtailed.

Rate watchers face an increasingly bond bearish trading environment. Adding pressure to the already anxious technical atmosphere are three Treasury coupon auctions and two major inflation reports. Consequently we wouldn't be surprised to see the benchmark 10-year Treasury note tick towards 3.70% before taking a run at a recovery rally.

In regard to MBS specifically, higher mortgage rates have led to lower lock volumes which implies less business for loan originators, but there is an upside in the production slowdown: Loan Pricing isn't deteriorating at the same pace as benchmark Treasury yields. Why? One answer has to do with Supply and Demand in the secondary market. Fewer new lock requests means less new MBS supply in the secondary mortgage market. Less new loan supply in the TBA MBS market (loan pipeline hedging) means less sellers are present. This is a favorable trading environment for all mortgage-backed securities market participants, which explains why MBS have generally outperformed their directional guidance givers (Treasuries) lately. For loan pricing, it lessens the pain of a prolonged bearish trend in benchmark yields. But we must warn, if benchmark yields continue their ascent, "rate sheet influential" MBS coupons will likely experience a modest amount of snowball selling as they catch up with the benchmark sell-off.

On corporate earnings, Reuters reports that investors will look to corporate profits and outlooks for confirmation the S&P 500 has another leg to its rally as the earnings season gets under way. "Earnings are what the market is all about. Earnings are critical in here, guidance is critical in here, the conference calls are critical in here," said Paul Mendelsohn, chief investment strategist at Windham Financial Services in Charlotte, Vermont. "In terms of earnings and sectors, you basically want to be with those people who have the ability to raise prices or are participating in the commodity price increases," he said. "And you really don't want to be in those people who have the input costs increases and are going to see their margins squeezed by rising commodity prices.

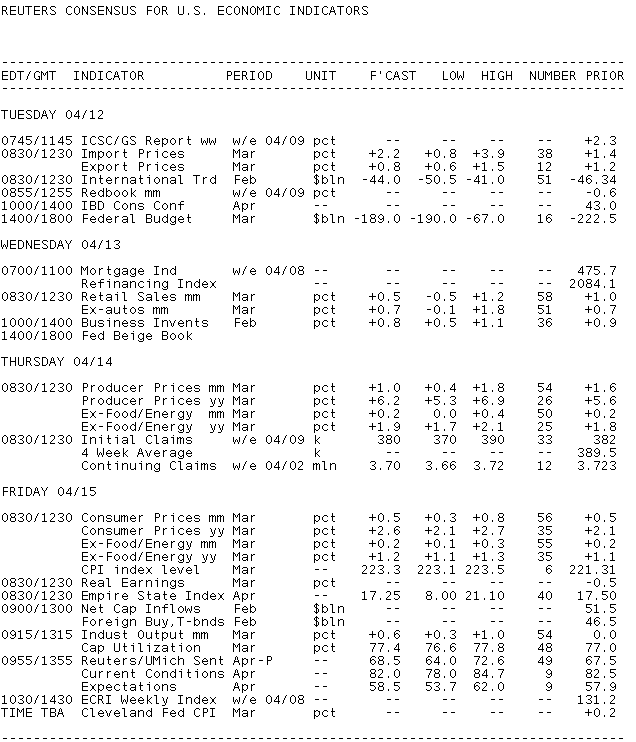

Key Events This Week:

Monday:

No economic events but Monday is Class A Notification Day in the TBA MBS market aka the monthly roll.

12:15 - Federal Reserve Vice Chair Janet Yellen speaks on

"Commodity Prices, the Economic Outlook and Monetary Policy" before the

Economc Club of New York. Audience Q&A expected.

Treasury Auctions:

11:30 - 3-Month Bills

11:30 - 6-Month Bills

Tuesday:

4:15 - William Dudley, president of the New York Fed, speaks

on "Financial Reform: The Importance of International Coordination" at

seminar of Institute of Regulation and Risk, North Asia, in Hong Kong.

8:30 - The monthly Trade Balance is

anticipated to shrink in February after a significant widening to begin

the year. The January trade deficit ballooned to $46.3 billion - the

biggest shortfall since June - from $40.3 billion in December, as total

imports jumped 5.2% versus a 2.7% climb in exports. Rising oil prices

played some role, but imports of other items also expanded rapidly (auto

parts: 14%, consumer goods: 2.2%).

The February deficit should

narrow with exports outpacing imports, economists say. Forecasts look

for a gap of $44 billion. The rise in oil prices should be offset by a

drop in import volume, and automotive imports are anticipated to decline

after two heavy months.

"The combination of the weak dollar

(bolstering export competitiveness) and rising global demand should be

the key factors contributing to the improvement," predict economists at

TD Securities. "Exports should rise for the eighth straight month while

imports should fall modestly. Rising energy prices, however, should push

the petroleum deficit sharply higher and excluding petroleum the trade

deficit is expected to improve.

In the coming months, with the weak

dollar continuing to boost export activity, the deficit should ease

further though this is likely to be offset by rising energy prices."

9:15 - Federal Reserve Bank of Kansas City President Thomas Hoenig participates in panel, "Too Big to Fail? How Best to Regulate and Structure Financial Institutions to Ensure Future Economic Prosperity" before the National Association of Attorneys General Presidential Initiative Summit.

2:00 - The Tea Party won't be pleased with this one. The Treasury's Budget Statement

for March is expected to print a monthly deficit of $190 billion,

according to economists polled by Thomson Reuters. That figure is nearly

triple the March 2010 deficit of $65.4 billion, and far bigger than the

five-year March average of $98.6 billion. Adding it to the deficit in

the first five months of this fiscal year, the total will be $822.3

billion. Not a good start to the era of fiscal constraint.

"Tax

receipts from individuals (income and payroll taxes) were probably less

than in March 2010 because of payroll tax cuts," said economists at

Nomura Global Economics. "In addition, outlays in the same month of last

year were much smaller than this year, reflecting a reduction in the

projected cost of the Troubled Asset Relief Program (TARP)."

2:45 - Federal Reserve Board Governor Daniel Tarullo testifies on "Derivatives Regulation" before the Senate Banking Committee

2:55 - Federal Reserve Bank of Dallas President Richard Fisher

moderates panel, "How Does An Economy Grow? Government Policy and the

Private Sector" before the George W. Bush Presidential Center -- The 4%

Project: Driving Economic Growth event.

Treasury Auctions:

11:30 - 4-Week Bills

1:00 - 3-Year Notes

Wednesday:

President Obama is anticipated to deliver a major speech Wednesday to lay out how the federal budget deficits can be curtailed.

8:30 - Retail Sales are

anticipated to grow for the eighth consecutive month in March, but the

overall pace is slower and a good portion of the increase is going

straight into the gas tank. The consensus forecast expects headline

sales to increase 0.5%, versus advances of 1% and 0.7% in the prior two

months. Auto sales, which last increased 2.3% and played a big role in

the recent increases, are expected to decline this month - retail sales

excluding auto sales are expected to advance 0.7%.

"Retail sales have been strong in 2011, but are getting hammered

by inflation," say economists at Bank of Tokyo-Mitsubishi, noting that

average retail gas prices shot up 10.8% in March to $3.62 per gallon.

They predict a 0.7% advance overall, but calculate that increase to be

just 0.1% once the effect of higher gas prices is taken out of the

equation.

"Automakers reported a decline in vehicle sales in

March, as consumers cut back purchases of trucks in light of the higher

gas prices, just as they did in 2008," BTMU added.

Economists at TD

Securities forecast that gasoline sales will post a 3% advance in the

month, which they say will offset the drop in auto sales.

"Core

consumer spending is also expected to be higher, rising by 0.4% m/m,

reflecting the positive tone in overall consumer spending," TD

continued. "In the months ahead, given the continued recovery in overall

economic conditions and sustained employment growth, we expect the

advance in consumer spending to be sustained."

10:00 - Look for Business Inventories to

grow 0.8% in February, following a 0.9% uptick in January. Inventories

remain lean and their growth should help GDP in the first-quarter

following impressive sales during the holiday period. The economics team

at Deutsche Bank said their growth takes on added significance "because

sizable inventory restocking is likely to account for nearly half of

the rise in real GDP we are forecasting for Q1."

Economists at

Nomura, who predict a 0.7% rise, added: "The combination of price

effects from higher energy prices and inventory accumulation probably

pushed up the dollar amount of private inventories, while stockpiling

activity by retailers could be moderate relative to wholesalers and

manufacturers."

2:00 - The Federal Reserve's Beige Book is

an anecdotal summary of regional economic performance published by the

12 districts of the central bank. It is published two weeks before the

FOMC meetings, where monetary policy is determined. This report will be

closely watched for talk of inflation and, of course, regional growth.

The

last report said the economy "continued to expand at a modest to

moderate pace in January and early February." Expectations are similar

for this report.

"While March surveys of business sentiment

remain upbeat, firms continue to feel the pressure of higher commodity

prices and express anxiety over geopolitical uncertainty," said

economists at Nomura. "The risks still seem balanced, and, in the words

of NY Fed President Bill Dudley, the economy's recovery is 'still

tenuous.'"

3:45 - Federal Reserve Bank of St. Louis President James Bullard gives welcome before a Homer Jones Memorial Lecture event

Treasury Auctions:

1:00 - 10-Year Notes

Thursday:

8:30 - With the bond market on edge about rising inflation, the Producer Price Index will

be watched closely this month. The headline index jumped 1.6% in the

month of February and forecasters assume another substantial increase in

March at 1%. Oil prices are of course the main culprit. The core index,

which excludes volatile energy and food prices, is anticipated to rise a

moderate 0.2% for the second straight month.

"Food will not

spike as it did last month (when a freeze devastated fresh vegetable

supplies), but food commodity prices do keep climbing," said economists

at IHS Global Insight, who believe oil prices could push the headline

figure to 2%. " Core prices should probably climb at the recent average

level of about 0.2% with some pass-through of higher commodity costs

pushing prices higher."

8:30 - Initial Jobless Claims have

been falling at a pretty steady pace recently. The last report showed

382k new claims for unemployment insurance in the week ending April 2,

down 10k from the previous week and comparing with 405k in the first

week of March. Economists anticipate 380k new claims this week, about 9k

below the four-week average.

"US initial claims for unemployment

insurance are likely to continue their downtrend in coming weeks," said

economists at Nomura. "While layoffs are certainly slowing, we will

focus on whether hiring picks up in tandem."

9:00 Federal Reserve Board Governor Elizabeth Duke speaks on "Credit Conditions for Small Businesses" before the International Factoring Association Conference,

9:00 - Narayana Kocherlakota, president of the Minneapolis

Fed, speaks to the HomeTown Helena Meeting in Helena, Montana on

"Economic Development in Indian Country."

12:30 - Charles Plosser, president of the Philadelphia Fed, speaks to the Levy Institute at Bard College in New York.

1:15 - Federal Reserve Board Governor Daniel Tarullo participates in "High-Wire Act: Balancing Growth and Inflation" panel at the Bertelsmann Foundation "Back to Work: Innovation, Investment and International Open Markets" conference

6:45 - Federal Reserve Bank of Richmond President Jeffrey Lacker speaks on "Economic Outlook, April 2011" before an event hosted by the University of Baltimore Merrick School of Business

Treasury Auctions:

1:00 - 30-Year Bonds

Friday:

8:30

- The latest inflation numbers have been putting pressure on the

Federal Reserve to begin hiking interest rates or end its program of

quantitative easing a bit early. The surge in February's Consumer Price Index was

the largest since July 2009, and March is expected to produce the same

results: a 0.5% advance in headline prices and a 0.2% gain in core

prices.

"Pressures from food and energy continue to build," said

economists at RDQ after last month's report. "Not only is headline

inflation running at 2.1% over the last year but it is accelerating with

the increase over the last three months running at a whopping 5.6%

annualized rate."

Economists at BTMU note how rising prices are eating into consumer confidence.

"The

March preliminary reading on consumer sentiment showed that sentiment

dropped by a whopping -9.3 points while short-term inflation

expectations jumped to 4.6% from 3.4%in February," they said. "Higher

prices are squashing the revival in consumer spending. Adjust for

inflation and real consumer spending is expected to slow sharply to

+1.5% in Q1 compared to +4.0% in Q4."

8:30 - The Empire State Manufacturing Survey,

the first regional manufacturing report released each month, is

anticipated to hold steady at a robust 17.5 in April. The index has come

in above zero - the threshold for growth - in each of the past four

months and 14 of the previous 15 months.

9:15 - Industrial Production is

forecast to rebound by 0.6% in March, following a 0.1% cutback in

February and a moderate 0.3% climb to begin the year. Recent reports

have been disappointing owing to a two-month downturn in electricity

(utility output fell 4.2% last month and 4.5% in January), but normal

weather should make this report a clean read on the sector. Economists

at BBVA note that 0.6% was the average pace of expansion in 2010.

"The

major force behind higher output will be from core manufacturing, based

on the evidence from the ISM manufacturing survey and from factory

hiring," said economists at IHS Global Insight. "The goods sector of the

economy is in a mini-boomlet, and March gains should show that."

9:55 - Consumer Sentiment fell

precipitously in March as consumers became concerned with rising

prices, the earthquake in Japan, and geopolitical turmoil in the

middle-east. Though the stock market has rebounded, economists aren't

expecting much improvement. The consensus is for 69.0, or 1.5 points up

from March.

"Rising energy and food prices, falling home prices,

stock market volatility, and the turmoil in the Middle East have taken

their toll on consumer sentiment - especially its expectations

component," said economists at IHS Global Insight. "The prospect of a

federal government shutdown may also take its toll on confidence."

11:15 - Charles Evans, president of the Chicago Fed, speaks to the Levy Institute at Bard College in New York.

1:30 - Thomas Hoenig, president of the Kansas City Fed, speaks at Purdue University in West Lafayette, Indiana.