In the world of mortgage rates there are varying degrees of opportunity, all of which are dependent on your wants and needs.

Making the decision to lock based on a near term economic event, such as the Employment Situation Report last week, would imply you're judging opportunities based on a sensitive lock/float timeline. As in, you must close your loan in the next 30 days and cannot afford to lose your current market rate quote.

On the other end of the sensitivity spectrum we find the folks feeling sorta "ho-hum" about the whole lock/float thing. This group isn't numb to upward movements in mortgage rates, but their current payment is more than acceptable. This group needs a total reversal of fortunes. It needs a return to rates below 4.00%, or the deal just doesn't make "cents". This would take us back to the days when the "PHANTOM 3.5 MBS COUPON" were trading at will in the secondary mortgage market. Included in this group are many the folks who went down with the ship in December.

For the "ho-hum" group. Almost all of your journey still lies ahead. If...IF...interest rates do rally lower, lenders will be hesitant to get ahead of themselves. There will be a degree of defensiveness to get past. This will not be a short voyage. It will take time and a big commitment from the bond market.

These are the two ends of the rate watcher sentiment spectrum.

Somewhere in the middle we find the medium term opportunist. Right now you're thinking, "is this the end of all-time low mortgage rates?". Your refinance option is "in the money", but not by much and you're not totally attached to the idea of going through an intense fiscal frisking as part of the underwriting process. This makes you very sensitive to another trend of rising mortgage rates, but sorta mixed on whether or not it's time to "pull the trigger". You are qualified. Have applied for a loan. Your appraisal is completed. You're just waiting for one more shot at those record lows...if you don't see it soon, you're gonna take what you can get and move on.

For the medium term opportunist, we are encouraged by the relative stability seen in the mortgage market lately. After a long trend of rapidly rising mortgage rates, we have enjoyed a period stability and even a bit of positive progress! This supports our theory that the December jump in mortgage rates was exaggerated by thin holiday trading conditions and year-end balance sheet positioning. It gives us hope.

Please don't read "encouraged" to mean "overly optimistic". It's hopeful thinking. Yes there are many factors leaning in our favor, but there are also many factors leaning toward higher rates. We have indeed made noticeable improvements in 2011. And we could see a modest move lower from here, but NOTHING has been confirmed in this recovery rally yet. We have simply moved into a range and are currently in the low side of that range. But don't get it twisted, we are not outside of the recent range. Meaning we could just as easily move in the opposite direction based purely on a lack of rally motivation.

This is where the medium term opportunist meets the "here and now" day over day, super sensitive rate watchers. Mortgage rates are at their most aggressive levels in about a month. Since early December really...

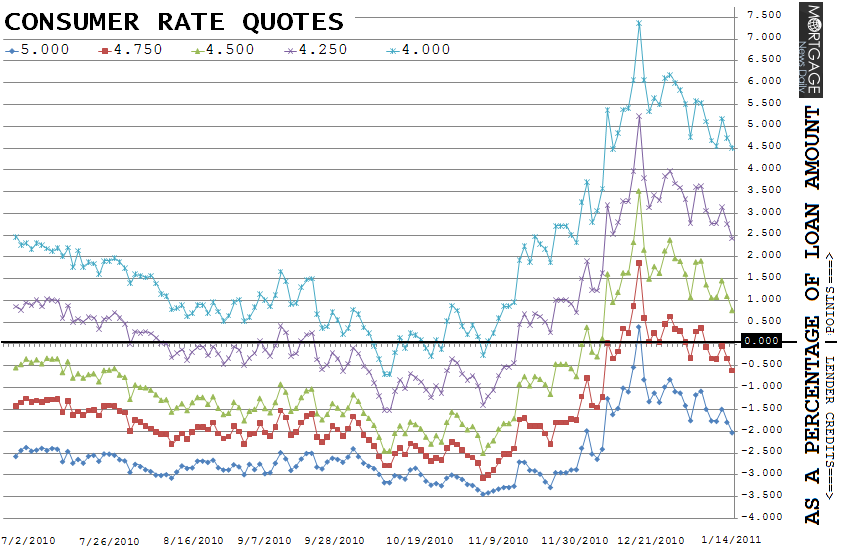

On this graph you will see five different colored lines. Each line represents a different 30 year fixed mortgage note rate. The numbers on the right vertical axis represent origination closing costs as a percentage of your loan amount. Also notice the dark black horizontal line at 0.00. If the note rate graph line is below the 0.00% marker, then the consumer may potentially receive closing cost help from their lender in the form of a lender credit toward third party fees. If the note rate line is above the 0.00% marker, the consumer should expect to pay additional points at the closing table to cover permanent buydown fees. These cost estimates were generated using average loan pricing quotes from the five major mortgage lenders.

Important Mortgage Rate Disclaimer: Loan originators

will only be able to offer these rates on conforming loan amounts to

very well-qualified borrowers who have a middle FICO score over 740 and

enough equity in their home to qualify for a refinance or a large enough

savings to cover their down payment and closing costs. If the terms of

your loan trigger any risk-based loan level pricing adjustments (LLPAs),

your rate quote will be higher. If you do not fall into the "perfect

borrower" category, make sure you ask your loan originator for an

explanation of the characteristics that make your loan more expensive.

"No point" loan doesn't mean "no cost" loan. The best 30 year fixed

conventional/FHA/VA mortgage rates still include closing costs such as:

third party fees + title charges + transfer and recording.

As an example, 4.00% note rates would cost a borrower almost 4.50

discount/origination points at the closing table, as a percentage of

their loan amount. This is clearly not advisable nor is it attainable. A

more relevant example is the 4.75% note rate. A very well-qualified

consumer should be able to close on a 30 year fixed mortgage at 4.75%

with no additional originator compensation related closing costs. 4.75%

is very close to the 0.00% line. We don't see many borrowers getting a lender credit on that note rate right now though. If you are, congrats! That is a great quote.

Plain and Simple: if the note rate line is moving up, the closing costs associated with that quote are rising. Thus, it should be obvious how mortgage rates behaved in December. They moved quickly higher. It should also be obvious that mortgage rates are in a downtrend but running into resistance.

Notice when looking adjacently on the chart from current levels, the last time mortgage rates were this aggressive was early December/late November. Below that level is a large drop-off. This illustrates a major hurdle for mortgage rates, which move lower much faster than they move higher.

I guess some folks have a decision to make....

On conventional 30 year fixed loans Best Execution is split between 4.75% and 4.875%. The same can be said about FHA/VA 30 year fixed loans. The market is split between 4.625% and 4.75%. If you're shopping for a 15 year fixed mortgage rate, we see a sweet spot split between 4.125% and 4.25%. On 5-year ARMs, we've heard of very well qualified borrowers being quoted rates as low as 3.50%.

"Bext Execution" is the most efficient combination of note rate and points paid at closing. This note rate is determined based on the time it takes to recover the points you paid at closing (discount) vs. the monthly savings of permanently buying down your mortgage rate by 0.125%. When deciding on whether or not to pay points, the borrower must have an idea of how long they intend to keep their mortgage. For more info, ask you originator to explain the findings of their "breakeven analysis" on your permanent rate buydown costs.

Important Mortgage Rate Disclaimer: Loan originators will only be able to offer these rates on conforming loan amounts to very well-qualified borrowers who have a middle FICO score over 740 and enough equity in their home to qualify for a refinance or a large enough savings to cover their down payment and closing costs. If the terms of your loan trigger any risk-based loan level pricing adjustments (LLPAs), your rate quote will be higher. If you do not fall into the "perfect borrower" category, make sure you ask your loan originator for an explanation of the characteristics that make your loan more expensive. "No point" loan doesn't mean "no cost" loan. The best 30 year fixed conventional/FHA/VA mortgage rates still include closing costs such as: third party fees + title charges + transfer and recording. Don't forget the intense fiscal frisking that comes along with the underwriting process.