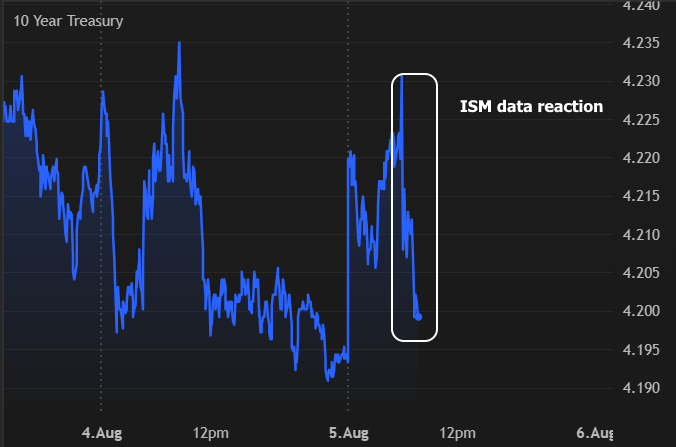

The ISM Services Index is/was easily this week's biggest ticket in terms of scheduled economic data. It was mostly OK for bonds with the growth-related components coming in slightly weaker. But the "prices paid" component remains problematic. At 69.9 vs 67.5 previously, the price component is at another new post-pandemic high for the 4th time this year. And of course, inflation is the biggest impediment to lower rates at the moment. Nonetheless, the remainder of the report was downbeat enough to offset the inflation implications, but just barely. Bonds are now just about unchanged after starting the day slightly weaker.