Volatility has not been a friend to mortgage rates over the last 30 days, but in the last 36 hours, we've been good buddies!

Today put a nice bookend on a bond market correction that began yesterday around noon. This follows a painstaking selloff that played out relentlessly through the end of November all the way into Wednesday morning. Phew. It's about time! The mortgage-backed securities (MBS) that dictate your loan pricing gained much ground today. This allowed lenders to reprice for the better which helped mortgage rates move lower into the weekend.

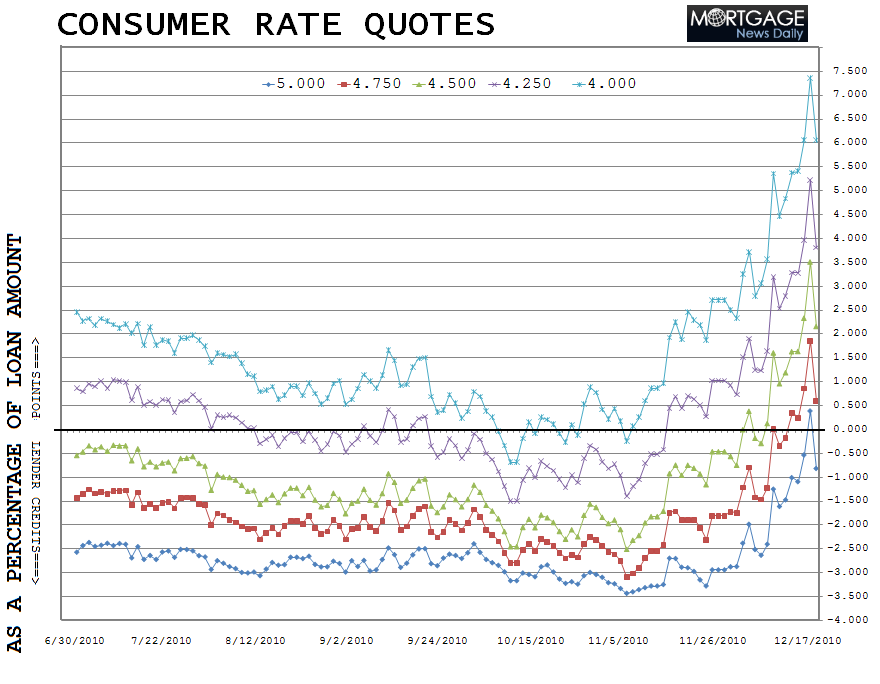

To illustrate the volatility we have created a mortgage rate chart using our loan pricing model. On this graph you will see five different colored lines. Each line represents a different 30 year fixed mortgage note rate. The numbers on the right vertical axis represent origination closing costs as a percentage of your loan amount. Also notice the dark black horizontal line at 0.00%. If the note rate graph is below the 0.00% marker, then the consumer should be expecting closing cost help from their lender in the form of a lender credit toward third party fees. If the note rate line is above the 0.00% marker, the consumer shouldn't be surprised if they are asked to pay additional points at the closing table to cover permanent buydown fees. These cost estimates were generated using average loan pricing quotes from the five major mortgage lenders.

As an example, 4.00% note rates would cost a borrower about 6 discount/origination points at the closing table, as a percentage of their loan amount. This is clearly not advisable nor is it attainable. A more relevant example is the 5.00% note rate. A very well-qualified consumer should be able to close on a 30 year fixed mortgage at 5.00% with no additional originator compensation related closing costs. They might even get some lender credits too! 4.75% is priced at 0.500% points paid by the borrower. This means, on average most consumers should not be expecting closing cost assistance from their lender (third party fees) at 4.75%. Instead they should be expecting to pay around 0.500% additional points at the closing table.

Plain and Simple: if the note rate line is moving up, the closing costs associated with that quote are rising. Thus, it should be obvious how mortgage rates have behaved over the past month. They've moved significantly higher. And fast. But you should notice a sharp decline over the last 24 hours.

Important Mortgage Rate Disclaimer: Loan originators will only be able to offer these rates on agency conforming loan amounts to borrowers who are have a middle FICO score over 740 and enough equity in their home to qualify for a refinance or a large enough savings to cover their down payment and closing costs. If the terms of your loan trigger any risk-based loan level pricing adjustments (LLPAs), your rate quote will be higher. If you do not fall into the "perfect borrower" category, make sure you ask your loan originator for an explanation of the characteristics that make your loan more expensive. "No point" loan doesn't mean "no cost" loan. The best 30 year fixed conventional/FHA/VA mortgage rates still include closing costs such as: third party fees + title charges + transfer and recordation + escrows (things like upfront MIP (if required), property taxes, homeowners insurance, accrued interest)

For folks who need to lock in their rate before the end of December, the default recommendation has been to take advantage of any upward swings in loan pricing, whenever possible. We got one of those upswings yesterday and another one today. This positive movement helped lead the best execution par 30 year fixed mortgage rate back down below 5.00% to 4.875%. Best execution on an FHA 30 year fixed loan is 4.75%.

It may not sound like much, but to go from 5.25% yesterday to 4.875% today is a big jump. From that point of view, if you were happy with 5.00% yesterday but couldn't attain that quote, it's back today. If you are looking for 4.75%, we do feel momentum is shifting in our favor. But again...make sure this is undertstood....the improvements we've enjoyed over the last 36 hours change NOTHING about our cautionary suggestions regarding volatility. This market is very fickle. Volatility can lead to large shifts in your monthly payment. Remember! Volatility goes both ways.

For anyone who is thinking of waiting this market out a bit more...

Yes we feel this sell off has been overdone and rates will likely decline in the future, but it will probably play out in a "fits and starts" manner. This means, if rates do rally, that consumers will face a series of tough decisions in the process. Take the improvements and move on or wait it out for lower rates? From that point of view....

What MUST be considered BEFORE one thinks about capitalizing on a rates recovery?

- WHAT DO YOU NEED? Rates might not recover as much as you want/need.

- WHEN DO YOU NEED IT BY? Rates might not recover as fast as you want/need.

- HOW DO YOU HANDLE STRESS? Are you ready for MORE VOLATILITY in the bond market.