Ever hear us say "mortgage rates rise much faster than they fall". This is a factor of extension risk and right now we're learning a painful lesson on what extension risk really means....

In the past 60 days we've seen FNCL 4.0s retrace four price handles. The production MBS coupon title belt has changed hands twice. 10 yr TSY note yields are almost 90bps higher. The 2s/10s curve is 45bps steeper. And the best 30 year fixed mortgage rates have risen about 75bps to 4.75%. It certainly didn't take long to unwind 6 months of positive progress did it?

Investopedia defines "Extension Risk" as...

Extension risk is mainly the result of rising interest rates and is generally associated with mortgage related securities. As interest rates rise, the likelihood of prepayment decreases. Since loans in a pool underlying a security are being prepaid at a slower rate, investors are unable to capitalize on higher interest rates because their investments are locked in at a lower rate for a longer period of time.

Plain and Simple: Prepayment speeds determine the timing of principal cash flows coming back to the MBS investor. The faster the prepayment rate, the quicker principal cash flows are returned to the bond investor, which shortens the life of the fixed income investment. Conversely, when prepay speeds slow down, the average life of MBS cash flows grows longer, or extend. Only the borrower has the option to pay off their mortgage debt. If a borrower's mortgage rate is below current market yields, they will be less likely to refinance. If an investor buys a mortgage-backed security with cash flows supported by borrowers that have mortgage rates near or below current market, and rates unexpectedly rise, that investor will be holding an MBS instrument that is unlikely to prepay because the borrowers who back it will have less incentive to refinance (because current market rates are higher). Thus the investor is stuck with an underperforming asset vs. current market benchmarks.

What is duration?

Duration is the sensitivity of a bond's price value to a change in

interest rates. What duration tells us is how much a bond's price will

fluctuate based on a given change in yield. An originator might view

duration as the sensitivity of their loan pricing to changes in MBS

yields. When the yield curve is "extending", the note rates closest to par are the most sensitive to rising benchmark yields. This is because the note rates closest to par are considered "current market". When that loan pricing falls below par, it is considered "below current market", thus borrowers who have closed on these quotes are less likely to refinance in the future which extends the expected life of their mortgage. This decreases investor demand for the MBS coupons that are built with those note rates.

Plain and Simple: From an originator's perspective, duration is the sensitivity of your loan pricing to changes in MBS and benchmark yields . It is important to know that note rates closest to par are the most sensitive to rising benchmark yields.

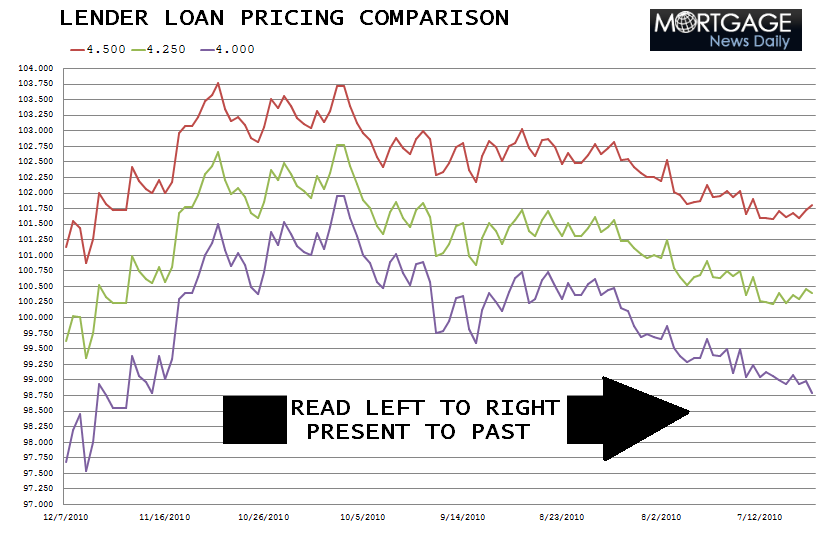

To apply this concept to the real world, over the past month the note rates closest to par have clearly taken the biggest beating on rate sheets. Those loans would have been securitized into 3.50 and 4.00 MBS coupons, but those quotes are now gone after the floor fell from under 3.50 and 4.00 MBS coupon prices....because of extension risk!

On average...

4.50 note rate pricing has declined 2.63 points. 4.25 note rate pricing has declined 3.03 points. 4.00 note rate pricing has declined a whopping 3.82 points. And that doesn't even include the massacre that played out yesterday.

SEE WHAT I MEAN BY "NOTE RATE PRICING CLOSEST TO PAR IS THE MOST SENSITIVE TO RISING INTEREST RATES" ?

I provided some big picture perspective on the bond market sell off last night. You should read this post if you haven't already: Brighter Outlooks or Year End Volatility? Watching the Bond Market Repeat History

The situation has deteriorated further this morning as Treasury prepares to sell $21 billion 10 year notes into a market that is lacking willing buyers (short covering and fast$ position squaring seen but mostly bid wanted!). Both FNCL 4.0s and 4.5s are down another point as accounts continue to shed extension risk. The 10yr note is up to 3.293% and the 2s/10s curve is another 6bps steeper at 267bps wide. It's hard to tell how much of this additional weakness is related to the pending 10 and 30 yr note auctions, but we have heard chatter that overseas real$ investors are trying to quietly liquidate some of their 10yr note longs. It's not surprising to hear those rumors given the massive back up in yields over the past two days. We'll get a better idea of foreign demand once the 10yr auction results are released at 1pm. I'd imagine some folks would be looking to cover short positions here....but don't think we'll see a huge recovery rally either.

Obviously rate sheets are worse.