Long Bond Auction Poorly Subscribed. TSYs selling. MBS prices print new session lows.

REPRICES FOR WORSE LIKELY

UPDATED WITH CONTENT BELOW....

Treasury just tried to sell $13 billion 30 year bonds to a bunch of crickets.

The bid to cover ratio, a measure of auction demand, was 2.49 bids submitted for every 1 accepted by Treasury. This is below average and the lowest BTC ratio since the Feb.11 refunding.

The high yield was 3.852%. This is 2.2bps higher than the 1pm "When Issued Yield", indicating investors wanted nothing to do with this issue unless it was considerably cheaper. Yucky.

The street took down a whopping 58.6% or $7.61 billion in long bond inventory. This represents an above average 34.6% of what they bid on, which to me says dealers were covering shorts during the auction and ended up getting a little more debt than expected.

Directs were awarded 9.1% of the issue and 28.9% of what they bid. Both metrics are well below average. This is becoming a trend for directs.

Indirect bidders took home 32.4% of the competitive bid and 67.2% of what they bid on. This auction award is below average and the lowest turnout from indirecs since March. The above average hit rate (67.2%) implies indirects submitted passive bids at higher yields and let the market come to them, which it did because no one else showed up to support the fundraiser.

Plain and Simple: just like the long bond auction last month, this one was brutal. It seems like the bond market is telling the Fed to make a move doesn't it? QE or no QE? What part of the curve are they gonna buy?

Market Reaction...

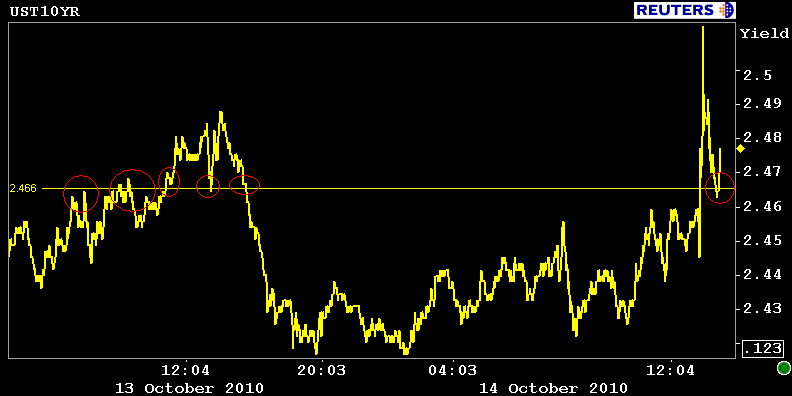

10s shot up almost 8bps to 2.513% before more short covering and modest real money buying helped lead yields back down to our 2.46% inflection point. This is a key pivot, 10s gotta break back below here or we might be moving higher over the next few days. In the short term we should continue to consolidate around this yield/price level before stored energy is released directionally.

Rate sheet influential MBS are at session lows but we're actually holding up quite well vs. TSYs. The December FNCL 3.5 is -0-01 at 100-30 after being bid as high as 101-02. The FNCL 4.0 is -0-01 at 103-03.

What are "rate sheet influential" MBS holding up so well?

Lock desks have plenty of pipeline coverage after selling forward about $5.5 billion in loan supply over the past two days. That left dealers long yesterday into lower prices but a barrage of duration and fast$ basis buyers seems to have leveled out that position to the point where dealers are now short on MBS inventory...which is one explanation of why offers are getting lifted today (plus slow flows in general) and prices are holding up well against benchmarks.

Still, until 10s drift back below 2.46% support, we will remain on high "reprice for the worse" alert.

Make your next move Federal Reserve....