At this point, veteran MBS commentary readers are well aware of the events that unfold on "Notification Day". When the process I am about to describe occurs, we usually make a big fuss about it...sometimes we even issue an alert to scare the daylights out of everyone. Sorry but its kinda funny to us. While that humor comes at your expense, it serves a purpose.

If written the right way, an MBS ALERT can stick in your memory for months to come. Think back on the chaos that ensued on Black Wednesday. That alert got over 20,000 hits. Remember November 25, 2008? That is the day the Federal Reserve announced the MBS purchase program. BLACK WEDNESDAY's alert stuck in our memories because rate sheets lost up to 200 bps on that day. The November 25, 2008 alert resonates for the opposite reason...it marked the beginning of the Fed's era in the agency MBS market. It was the beginning of "IT THAT SHALL NOT BE NAMED"

The point is, sometimes MBS ALERTs are meant to grab your attention, some MBS ALERTs are suppose to stick with you down the road. While we refrained from causing chaos today....WE ARE STILL TRYING TO GRAB YOUR ATTENTION!!!!

If you haven't read the following description of the agency MBS settlement process...please dont skip over it as it may save you from having to change your pants when next month's settlement rolls around. If you have read it...go over it one more time just to make sure the underlying logic is clear.

The January FN 4.5 MBS coupon has begun the settlement process. Before the end of the day, the FN 4.5 price is going to fall from where it is currently priced at 100-09 to about 99-30.

WHY???

The MBS coupons that determine your rate sheet pricing are traded in the TBA MBS market...

TBA = To be Announced.

In the TBA MBS market, at the time a trade is made, buyers and sellers agree to a few specific terms like what coupon, the issuing agency (Fannie, Freddie, Ginnie), size of trade, and a buy/sell price....the actual pools of loans are NOT exchanged at the time of this commitment. Instead, the MBS buyer and the seller make an agreement to complete the transaction at a later date. In the MBS market this date is pre-determined....it is called SETTLEMENT DATE (clever name huh?). Agency MBS trading settles once a month. For instance we have been watching the January MBS coupon trade since December 11. As of tomorrow morning, we will be watching the February FN 4.5 MBS coupon until February 9, 2009. HERE IS THE CALENDAR

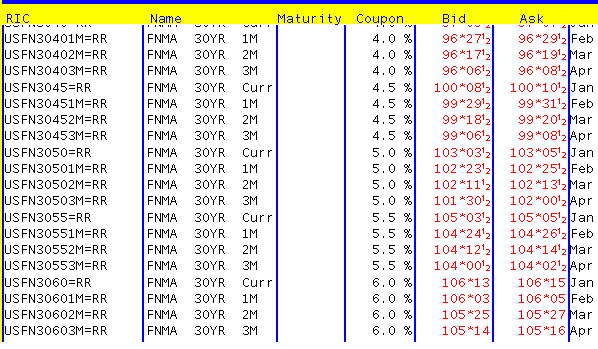

We can actually watch forward pricing as much as three months ahead...SEEEEEE:

Anyway...two days before the pre-scheduled settlement date, the MBS seller "notifies" the MBS buyer of the specific pools that they will deliver to satisfy the previously agreed upon terms of the trade. The MBS buyer then reviews the pool information to ensure that the seller is delivering loans that meet the agreed upon terms (which were determined at the time of the trade). Two days later, on settlement date, funds are wired and the trade is complete (it goes deeper...this is the outline of the trade).

But why do prices seemingly fall when the current delivery month comes to an end on notification day?

Prices dont really fall...we just start watching next month's MBS coupon because last month's coupon is settling. The forward month coupon price remains the same. Below is the current February settlement FN 4.5 MBS coupon...currently costing buyers 99-30 (if you bid with size). This is where prices will seem to fall later this afternoon.

I KNOW I KNOW...in your eyes prices are lower. Let me explain the reason why prices fall when we start watching the forward month coupon.

The main reason behind the price "DROP" is lost "time value of money".

Interest rates can be thought of in three ways..

1. Required Rate of Return: this is the minimum amount of return an investor is willing to receive when making an investment.

2. Discount Rate: the rate used to determine the present value of future cash flows. When you loan someone money with the intention of being paid back in the future, you must place a value on how much of a premium you are losing by not spending that money right now. The discount rate is essentially how much you are charging to delay repayment until a future date.

3. Opportunity Cost: the value an investor passes up when choosing an alternate investment. You must earn enough interest when you loan someone money to compensate for the loss of income that you could have been earning by investing elsewhere.

That said...would you rather have $1.00 today or $1.00 tomorrow?

You would rather have $1.00 today! If you have $1.00 today you can invest it today...the fact you are investing today vs. tomorrow implies you are giving the asset more time to appreciate.

Now to relate this concept to the MBS market...if you buy the JanuaryFN 4.5 coupon, then your returns will begin accruing on January 1. If you buy the February coupon...your returns dont start accruing until February 1.

Investing now puts money to work now. Waiting until February means the investor is missing out on accrued interest they could be earning right now. To compensate for the lost Time Value of Money you demand a higher yield....which means lower MBS price.

Note: to be clear, the previous owner has rights to the income (accrued interest) earned from while they owned the coupon. The price you pay to purchase the back month coupon includes the income the current owner has accrued while they owned the coupon. The buyer recovers the added premium when the coupon payment is deposited in their account. This is called the 'clean price'...its the same way Treasuries trade.

So hopefully, ignoring that last 'Note'.....a light bulb just went off in your head.

Plain and Simple: If you own the January MBS coupon, then you are entitled to the coupon clips (income) paid in January, this income is generated from the underlying loan's principal and interest (passed through from borrower to MBS investor). If you decided to wait until February to buy an MBS coupon...then you have to wait until February for your investment to start accruing income....so to compensate for the lost "time value of money" ..investors demand higher yields, which is why prices fall when delivery rolls forward to the next month.

And yes...there is the potential for rate sheets to reflect this price drop...but it theoretically shouldnt hurt pricing in the morning as most lenders have already accounted for "the drop".

Learn something new everyday and let your brain appreciate with time! - ME

Don't panic when you see prices fall off in the next hour...it's a normal function of the TBA MBS market.

{kind=link}