A slow macroeconomic data calendar in the week ahead includes industrial production today and housing starts Tuesday, but more important may be the heavy line-up of Federal Reserve officials giving speeches around the country.

The speeches follow chairman Ben Bernanke’s talk on Friday in which the central bank chairman made a cautious case for renewed quantitative easing. Two comments stood out to MND...

"Given the Committee's objectives, there would appear--all else being equal--to be a case for further action. However, as I indicated earlier, one of the implications of a low-inflation environment is that policy is more likely to be constrained by the fact that nominal interest rates cannot be reduced below zero."

AND...

"However, possible costs must be weighed against the potential benefits of nonconventional policies. One disadvantage of asset purchases relative to conventional monetary policy is that we have much less experience in judging the economic effects of this policy instrument, which makes it challenging to determine the appropriate quantity and pace of purchases and to communicate this policy response to the public. These factors have dictated that the FOMC proceed with some caution in deciding whether to engage in further purchases of longer-term securities."

The entire marketplace remains on Quantitative Surveillance ahead of the November 3 FOMC meeting. In addition to data and speeches, Citigroup, Bank of America, Goldman Sachs, and Wells Fargo will each report Q3 earnings this week.

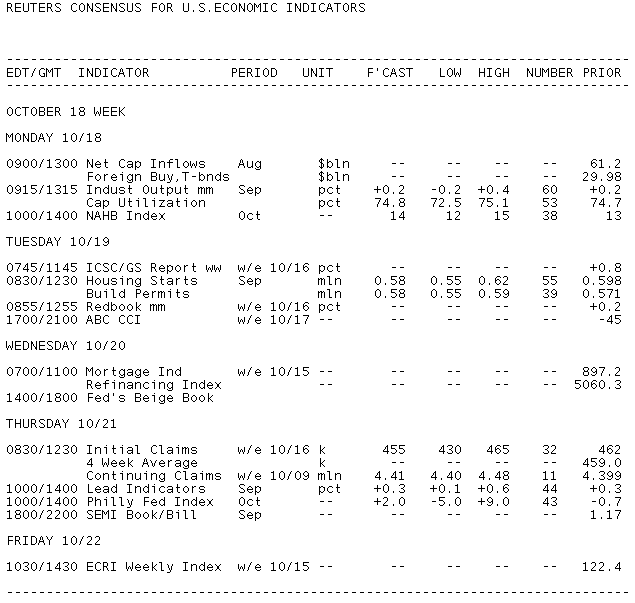

Key Events in the Week Ahead:

Monday:

9:00 ― The last Treasury International Capital flows report showed net capital inflows of $61.2 billion in July, including $30 billion in foreign purchases of Treasuries. That showed foreign investors continued to have great appetite for U.S. securities despite a slowing recovery. The investments purchased included corporate debt and equities – riskier investments as opposed to just flight-to-quality paper. Investors will be looking to see if those trends continue in the August report.

“Net foreign capital inflows into the US picked up in July, led by stronger demand for corporate bonds, equities and agency debt,” said economists at Nomura. “In contrast, flows into US Treasuries moderated further, and remained clearly below levels seen in the first half of the year.”

Economists at BMO added that market participants will be much more interested in the following month’s report, which will include the impact of Bank of Japan foreign exchange intervention “along with the pick up in FX intervention among other Asian central banks after the US$ weakened in the wake of the Fed’s September 21st announcement that it was moving a step closer to QE.”

9:15 ― Industrial Production, one of the key reports this week, is expected to rise 0.2% in September after a 0.2% gain in August. The modest gain would mark the 15th straight monthly increase, but levels this low aren’t encouraging. Motor vehicle production fell 5.0% in August and durable consumer goods declined 0.1%, indicating that not all sectors are growing consistently.

Economists at Deutsche Bank said industrial production, since bottoming in June 2009, is enjoying the strongest year-on-year rebound in nearly three decades. But they noted that a slow down would be consistent with the historical record.

“It is not unusual for manufacturing to slow temporarily at this stage of the recovery as the initial boost from inventory restocking fades,” they wrote. “This may be especially true of the auto makers, where production levels were up 35% and 42% year-on-year in Q1 and Q2 of this year — similar again to the 50% and 40% year-on-year gains in Q4 of 1983 and Q1 of 1984.”

Meanwhile, economists at Nomura look for a 0.4% advance.

“A number of leading indicators for industrial production deteriorated or were little changed during the month, including manufacturing employment and hours, the ISM production index and electricity output,” they wrote. “However, we estimate that seasonally-adjusted auto production picked up smartly after a 23% decline in the previous month. We therefore think industrial production growth could exceed consensus expectations.”

10:00 ― Housing Market Index, the NAHB’s survey of homebuilder sentiment, is anticipated to rise one point to 14 in October. Any score below 50 suggest pessimism, so slight movements carry little weight.

“In 14 of the last 18 months ― as well as the current month ― consensus forecasts have expected the NAHB homebuilder sentiment index to rise by 1 point. This recovery has failed to materialize, with the index languishing at low levels for around two years. Nevertheless, with the economy gradually recovering, we continue to expect the housing market and homebuilder sentiment to pickup at some point. We are therefore once again forecasting the index to rise by 1 point, to a level of 14.”

12:30 ― Dennis Lockhart, president of the Atlanta Federal Reserve, speaks on the economy in Savannah, Georgia. Q&A expected.

Monday is Class C Notification Day in the TBA MBS market. GNMA 30 year fixed MBS coupons begin the monthly settlement process. READ MORE ABOUT THE ROLL

EARNINGS RELEASES: Citigroup

Treasury Auctions:

- 11:30 ― 3-Month Bills

- 11:30 ― 6-Month Bills

Tuesday:

8:30 ― Housing Starts, which track new construction of single- and multi-family homes, are expected to fall to an annualized pace of 580,000 in September, down from 598,000 a month before. Building permits, which anticipate starts by a month or two, should also come in at 580,000, versus 571,000 in the month before.

Single-family housing permits declined for the fifth straight month in August, which points to a decline in single-family starts in September, said economists at IHS Global Insight. The forecasting firm said multifamily starts are also likely to drop after gaining 32% in August.

“Overall, we expect that housing starts dropped about 5.5% this month, to 565,000. We are expecting a small gain in permits, however, because the economy is growing and slowly adding jobs.”

Meanwhile, economists at BBVA predict housing starts will grow to 610,000 new units, marking a third consecutive advance. They noted that builders’ confidence is stable and new home inventory hit its lowest registered level recently, which could stimulate new activity. “The pick-up in housing starts in recent months points to recovery,” they added. “Nevertheless, economic conditions indicate that the recovery will be slow.”

9:40 ― Charles Evans, president of the Chicago Fed, speaks on the economic outlook to civic leaders in Evanston, IL.

12:30 ― Richard Fisher, president of the Dallas Fed, speaks to the New York Association for Business Economics in New York.

1:20 ― Narayana Kocherlakota, president of the Minnesota Fed, gives a luncheon speech on “The Tools of the FOMC” to business leaders in Fargo, North Dakota.

4:00 ― Ben Bernanke, chairman of the Federal Reserve, gives brief remarks before the Grand Opening of the Junior Achievement Finance Park in Fairfax, Va.

7:00pm: ― Elizabeth Duke, governor of the Fed, delivers a talk called “Come With Me to the FOMC” before a Money Marketeers of New York University dinner.

EARNINGS RELEASES: Bank of America, Goldman Sachs

Treasury Auctions:

- 11:30 ― 4-Week Bills

- 11:30 ― 52-Week Bills

Wednesday:

7:00 ― MBA Mortgage Applications continue to show that potential buyers haven’t yet responded to record low mortgage rates, although refinancings continue at high levels.

“Over the last several weeks the index of mortgage purchase applications has shown signs of stabilizing,” said economists at Nomura. “This may indicate that the post-tax credit bust in home sales is over and that volume will pickup in the next selling season.”

9:30 ― Jeffrey Lacker, president of the Atlanta Fed, delivers opening remarks to a “Economics Made Easy” journalism workshop at the University of Maryland.

12:45 ― Charles Plosser, president of the Philly Fed, speaks on incentives and regulation to the Union League in Philadelphia.

2:00 ― The Beige Book, an anecdotal summary of economic conditions across all 12 Federal Reserve districts, last indicated that auto sales and consumer spending increased in August, but that there “widespread signs of a deceleration compared with preceding periods.” Retail inventory was reported to be tight, shipping and transportation sectors expanded, and manufacturing was increasing. This report, which covers the six preceding weeks, is anticipated to report further deceleration.

“Businesses are reluctant to expand which negates their need for extensive commercial and industrial loans,” said analysts at BBVA. “We expect that the forthcoming Beige Book report will highlight ongoing weak recovery across the US.”

EARNINGS RELEASE: Morgan Stanley, Wells Fargo

Thursday:

8:30 ― Economists expect to see 455k Initial Jobless Claims in the week ending Oct. 16, down from a disappointingly high 462k in the previous week. The 4-week average is currently 459k, well down from the 487k average for August but not low enough to indicate robust job growth in the economy. Continuing claims ― the tally of all Americans receiving unemployment benefits (excluding emergency benefits) ― is expected rise to 4.41 million from 4.39 million.

“Overall recent claims reports suggest the trend is stable at around 455,000,” said economists at Nomura. “We believe this level is consistent with positive, but relatively low, private payroll growth.”

9:45 ― Thomas Hoenig, president of the Kansas City Federal Reserve, speaks in Albuquerque, New Mexico.

10:00 ― Leading Economic Indicators, a composite index credited with signalling changes 3 to 6 months out, is anticipated to repeat a +0.3 level in September. Some factors pointing to growth are higher stock prices, a steep yield curve, and a pickup in building permits.

Economists at BTMU say those reasons all point to government support rather than private recovery.

“The largest contributors to growth in September are expected to be the yield curve (the spread between the 10-Yr Treasury and the Federal Funds Rate) and the real money supply (M2),” they wrote. “Unfortunately, both are indicative of the incredible amount of support of the Federal Reserve to prop up the economy, rather than improvement in fundamental growth. In fact, since the recovery began in June 2009 the yield curve has accounted for more than 55% of the strength in the leading indicator.”

10:00 ― Philadelphia Fed Survey jumped seven points in September but remained in contraction at -0.7. This month, the increase is set to be smaller, but it should be be enough for the sector to see growth. The consensus forecast is +2.0.

“The Philadelphia Fed's business outlook index stabilized around zero last month after dropping sharply in August,” said economists at Nomura, who said a +2 score would be consistent with underlying growth in the economy of 1.5-2.0%. “The prices paid indexes may start to pickup due to higher global commodity prices.”

10:00 ― James Bullard, president of the St. Louis Fed, delivers opening remarks to the Annual Economic Policy Conference in St. Louis. His talk is “Frictions in Financial and Labor Markets.”

11:00 ― Treasury announces the terms of auctions to be held in the following week. Maturities to be offered include 2s/5s/7s and 5 year TIPS

Friday:

No significant data.

12:45 ― Charles Plosser, president of the Philly Fed, speaks on regulatory reform in closing remarks before the Regulatory Reform Media Seminar hosted by the Federal Reserve Bank of Philadelphia.