The Garrett Watts Report Newsletter: January 12, 2010

You know how the Fed has been buying up so many Fannie, Freddie and Ginnie Mae MBS? We read that last year the Fed made up something like 83% of all purchases of all such purchases. We can’t find the article, and it may have been 73%, but either way, it’s a big number. It will be interesting to see what happens as they stop buying. The conventional wisdom is that it will cause rates to go up, but the conventional wisdom isn’t always right.

And while we’re talking about mortgages, we all know what an MBS is, right? It’s a mortgage backed security, singular. So when you’re talking about a bunch of them, plural, do you call it “a bunch of MBS” or is it “a bunch of MBS’s” or, maybe MBSs without the apostrophe? Do you pronounce the plural of MBS like Em-bee-ess-iz or is it more properly Em-bee-ess-uh-zuz? Would someone please call Lew Ranieri and ask him?

How do you handle volatility? From late 2007 to the 2009 lows, the Bank of America stock was down 94%. By year-end 2009, it was up 380%.

Thumbs down for Up in the Air. George Clooney’s character is empty, and while he has a certain charm, he has no friends, no family, no home, and no possessions. His acting is what we’ve come to expect from him, and while there are a few light moments, the overall theme is depressing.

We just read about call centers that pay their employees by the minute, but only for the time the person’s actually on the phone with customers. The one we read about pays $0.25 a minute, meaning that the most a person could make if they talked every second of every minute of every hour would be $15 an hour. It’s like the old days of piece work. It seems weird at first, but it actually seems to make sense. Sort of.

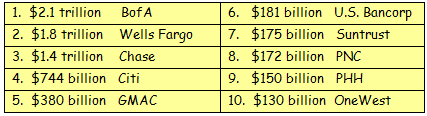

Remember when Lomas & Nettleton was the nation’s biggest servicer with about $20 billion?

Here are the top servicers today.

Number 10 OneWest is the new name for what used to be Indy Mac Bank. What kind of cash flow does $2 trillion throw off? Let’s assume 35 bps of servicing income, and if our math is right, the servicing fee is about $7 billion a year or $580 million a month of gross revenue.

Horizon Bank in Washington State with $1.3 billion of assets has failed, and the FDIC estimates that the cost will be approximately 41% of stated assets. It seems like only yesterday when the Northwest banks were doing so well. About 30% of Horizon’s portfolio was construction and land development, with another 34% in multi-family and commercial real estate. That 41% loss still seems shocking.

You always read about how the key to real estate investing is to use OPM, or Other People’s Money, and here’s an interesting example: Tishman Speyer paid $5.4 billion for a huge apartment complex in New York (Peter Cooper Village), and it’s now worth $1.8 billion. How much of that $3.6 billion loss did the Speyer family lose? They lost only $112 million, with the big losses being taken by their investors. This will knock your socks off, but one of their biggest investors in the deal was the Church of England.

The Dornbusch Law (named, imaginatively, after the late MIT professor of economics, Rudi Dornbusch) states that “In financial markets, things always take longer to happen than you expect – but once they happen, events unfold more quickly than you’d ever have imagined.” Think back on the financial crisis of 2008-2009. Isn’t this exactly how it unfolded?

Heavyweight boxer Mike Tyson once said that “everybody has a plan until they’re hit.” An interesting statement and one worth thinking about when you’re updating your strategic plan. The real message is to always have a Plan B.

No one’s going to ring a bell announcing that the refinance boom is over, but we were puzzled by the MBA refinance Index. It was 5,904 one year ago and this week it was 1,976. That’s a 67% drop over the past twelve months. Should mortgage lenders be worried? We’re not on the front lines with loan officers, but it sure seems like things could be cooling down, now or in the near future.

We mentioned last week that two banks raised their dividends twice last year, and some of you wanted to know which. They were 1st Source (SRCE) and Hudson City (HCBK). Pretty amazing, to raise the dividend not once but twice in such a tough year. Some more on 1st Source:

1st Source was founded in 1863 as First National Bank of South Bend (Indiana). It currently has 75 branches in Indiana and Michigan and $4.4 billion in assets. A few of their metrics aren’t all that great: A 0.57% ROA, 4.1% ROE, 3.1% net interest margin, and an efficiency ratio of 68%. What has really stood out for them, however, is that only 2.9% of their loans are non-performing. Credit quality always pays off in the end. We like this bank.

Okay, we’ll go along with the idea that keeping GMAC alive is somehow in our national interest and worthy of federal bailout money. But when are they going to start getting things turned around there? It’s hard to know how their auto-lending is doing, but Ally Bank will report a $1.3 billion loss and ResCap, not to be outdone, will report a $700 million loss. And finally, their international lending group didn’t want to be left out, so it will report a loss of $1.3. These are apparently due to re-classifying loans from held-for-investment to held-for-sale, but whatever. GMAC and ResCap have brought in some great people like Steve Abreu, so maybe we’ll start seeing a turnaround soon.

We get asked from time to time if we do recruiting. We’re not recruiters or head hunters, not by a long shot. However, we have done a number of select searches for clients, mostly in the areas of Secondary Marketing, Heads of Operations, and Finance. Our fee, by the way, is about a third of the typical recruitment firm.

Ladies, do you have one of those lower back tattoos? A study showed that if an epidural is pushed through the tattoo during child birth, there could be severe problems if the ink enters the spine. There may, however, now be a way to remove that tattoo someday: CHECK IT OUT

Well, that’s all for now. See you next week sometime.