The idea that it is a good time to buy a home appears to be losing ground. The National Association of Realtors'® (NAR's) new fourth quarter Housing Opportunities and Market Experience (HOME) survey appears to confirm a gradual erosion in this sentiment that Fannie Mae's National Housing Survey has been reporting for months. Unlike Fannie's monthly survey, however, the NAR also found that households are less confident about the economy and their personal finances.

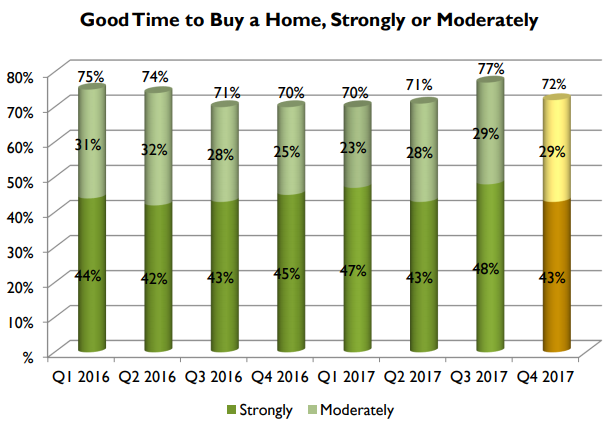

Seventy-two percent of the persons responding to the NAR survey said they surveyed considered it a good time to buy. For 43 percent it was a strong belief, down from 48 percent in the third quarter survey, and from 45 percent in the fourth quarter of 2016. Across all respondent groups only 28 percent didn't think it was a good time at all, with optimism fading the most among renters; only 60 percent viewing this as a good time, down from 62 percent in the last survey. Millennials and those who live in urban areas also had fewer positive responses. Of those who own, make more than $100,000 per year, are over age 65, or live in the Midwest, four out of five consider it a good time to buy.

NAR Chief Economist Lawrence Yun says this fall's pitiful supply levels and weaker affordability conditions are likely casting doubt about buying. "The trifecta of faster economic expansion, robust hiring and low mortgage rates should be generating a surge in optimism and home sales as 2017 winds down," he said. "Sadly, this is not the case. While overall demand remains high, it is not translating to meaningful sales gains. Too many prospective first-time buyers see few options within their budget and home prices that are rising much faster than their incomes."

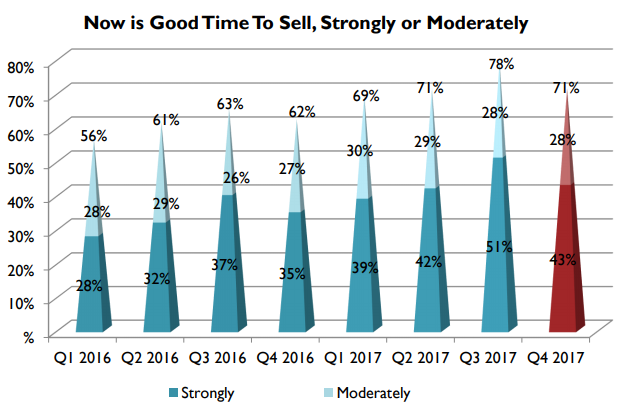

Selling a home didn't fare much better. The number of respondents who thought it was a good time to do so dropped from 78 percent in the third quarter to 71 percent, although that was substantially higher than a year earlier.

NAR included a few questions in the fourth quarter survey regarding the tax bill currently before Congress. Eighty-five percent of respondents said they would take both the existing mortgage interest deduction (MID) and the property tax deduction were they to buy a new home. Asked about the possible implications for homebuyers should bill pass with proposed limitations on those deductions, 48 percent said it would cause them financial strain and 30 percent said they would reconsider a move.

Even though the economy has expanded over the last two quarters and job gains are still strong, although down from last year, fewer households (52 percent) believed the economy is improving than did so in the two earlier periods, declines of 5 percentage points from Q3 and 2 points from Q4 2016. This lower confidence in the economy seemingly led to households turning a little negative about their own financial situation. NAR's index measuring confidence that personal finances will improve over the next six months fell from 62.0 in September to 59.1 in December. A year ago, the index was 59.8.

"The significant rise in home values and the stock market at record highs are why a majority of homeowners, as well as those with incomes above $100,000, are more optimistic about the economy than renters and those with lower incomes," added Yun. "The overall job market and economy are very healthy. If housing supply improves enough next year to boost the nation's homeownership rate, it's very likely more households will feel upbeat about their future."

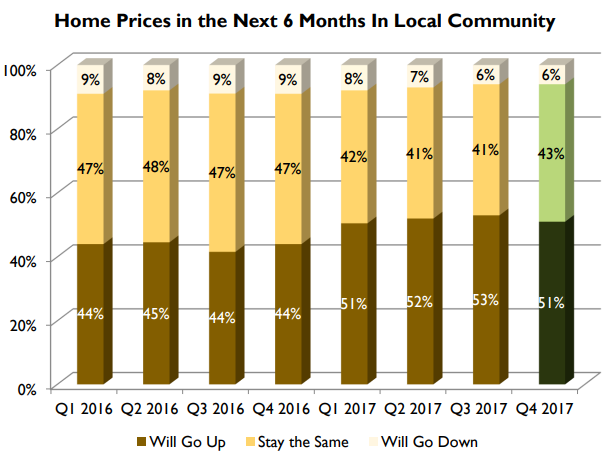

Sixty-four percent of people believe that home prices within their communities have risen in the last 12 months, relatively unchanged from the third quarter and an increase from 55 percent a year earlier. They don't necessarily agree this will continue; 43 percent don't expect further increases, and 6 percent think they will decline.

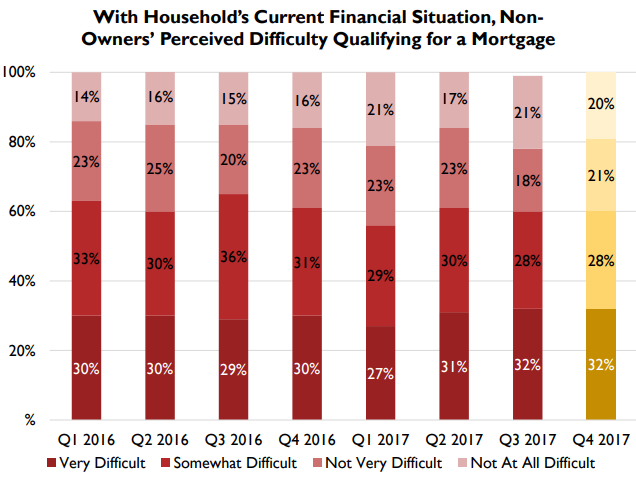

The percentage of non-homeowners who think they would have problems getting a mortgage increased from previous surveys. Thirty-two percent thought it would be very difficult compared to 30 percent a year earlier and 28 percent thought it would be somewhat difficult. Not surprisingly, the negative responses were higher among those with lower incomes.

NAR's HOME survey is conducted monthly by phone among approximately 900 respondents. The monthly data is then compiled into a quarterly report which, in the fourth quarter, represented 2,705 completed interviews.