A recent spate of positive news has allowed Fannie Mae to upgrade several pieces of its economic forecast this month. The approval of at least one COVID-19 vaccine, new hope for additional stimulus approval, and stronger than expected incoming data has pushed the company's economists to upgrade their outlook for real gross domestic product (GDP) to negative 2.2 percent for the full year 2020, up from a negative 2.5 percent in their November version. The change for 2021 is more substantial, from 3.3 percent to 4.5 percent. Growth in 2022 has been raised two-tenths of a point to 3.2 percent. The economists say, "We continue to believe that the conditions for a continued, strong recovery are present once the limiting factors of COVID-19 on consumer behavior are lifted."

The Q4 GDP forecast has also been revised upward, from 4.3 percent annualized to 5.4 percent, based almost entirely on activity in October. It reflects an expectation of only slight growth in consumer spending (PCE), which was unusually high in October, into November, then a modest decline in December. This weakness is expected to continue into the first month or two of 2021 prior to a rebound as spring approaches.

Growth in the next few months is likely to be weak, and uncertainty high as the economy navigates some obstacles. At this point, COVID-19 cases continue to rise, and hospitalization rates and daily fatalities are hitting record highs so local governments are increasingly implementing restrictions. Colder weather will probably put a damper on outdoor activities such as dining which did experience some earlier recoveries. It is also unclear how heavily holiday spending will be impacted.

Comparative weakness in labor market measures, namely a deceleration in employment growth in November to 245,000 jobs, down from 610,000 in October, as well as a recent bump up in unemployment claims, suggest that some softening is already underway.

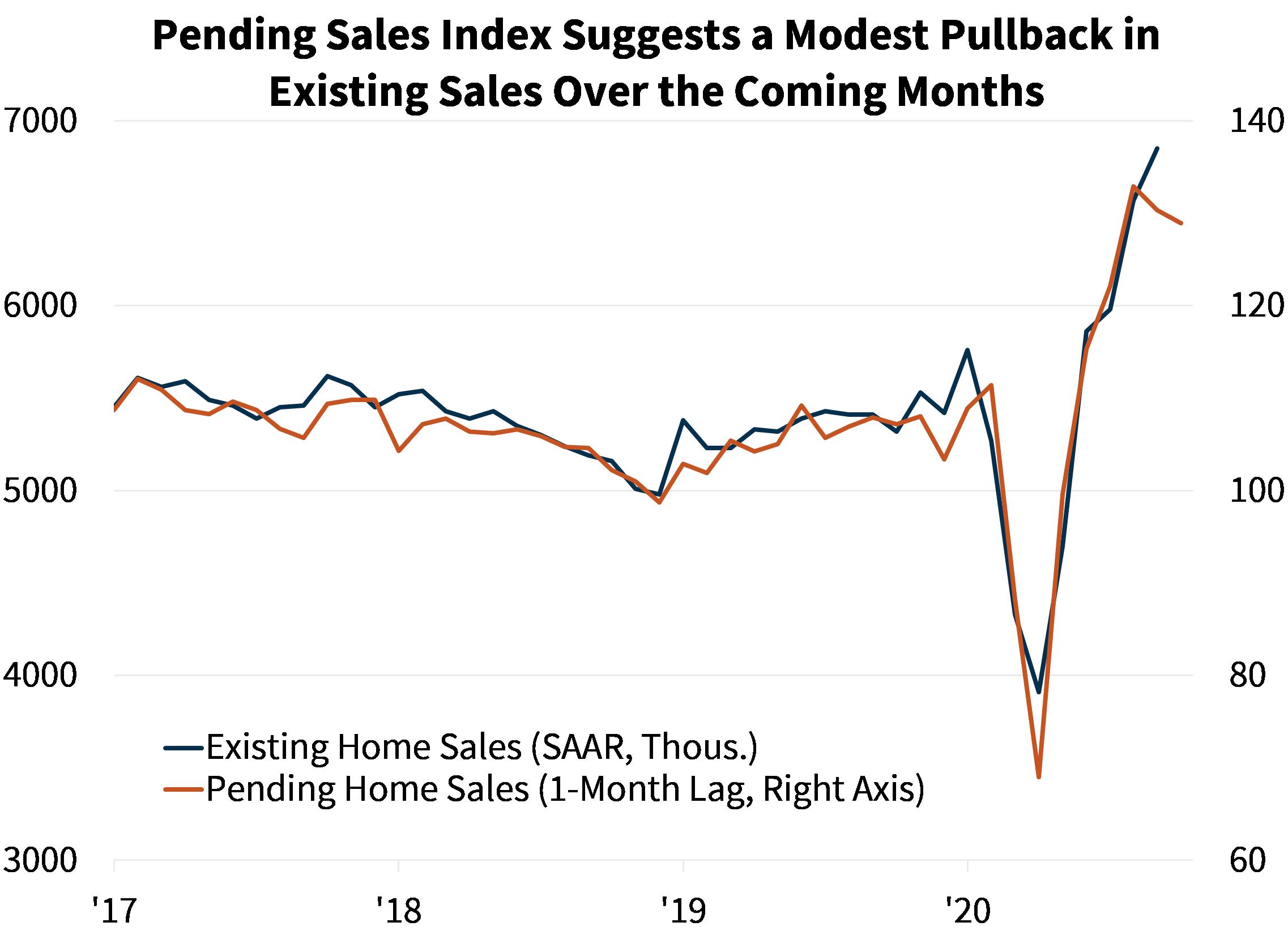

Home sales continued their recent trend of remarkable strength. Existing home sales again surprised to the upside, rising 4.3 percent in October to 6.85 million annualized units, compared to an expectation of a modest decline. This provoked an upgrade in the fourth quarter existing sales expectation to an annualized 6.62 million units from 6.22 million. The outlook for 2021 also changed. Fannie Mae still forecasts a strong pace of sales in the first quarter, a 12.1 percent gain from the first quarter of 2020, sales will probably pull back from its October pace. Inventories continue to be extremely tight, with the months of supply of existing homes for sale hitting 2.5 in October, the lowest on record and down from 2.7 months in September. Rapid home price appreciation has also eaten into the affordability gains from lower mortgage rates, with home prices up 7.3 percent in October from a year prior according to the CoreLogic National Home Price Index.

History suggests that the current sales pace for homes is not sustainable. October's sales were above the normal relationship with the prior month's pending sales index, which leads closings by 30-45 days. When these two series have diverged in the past, there is usually a convergence within a month or two. Further, the pending sales index dipped back 1.1 percent in October, and the Fannie Mae Home Purchase Sentiment Index pulled back 1.7 points in November, both of which suggest a modest cooling of home sales in the near term.

Fannie Mae doesn't believe the strong homebuyer demand is due entirely to low interest rates or residual pent-up demand from the spring lockdowns. Its mortgage application data continues to show an elevated rate of urban dwellers purchasing homes in lower density areas in November. Whether this is a permanent shift in homebuyer preferences or a temporary one related to social distancing, it does appear to be further driving elevated purchase demand and will probably continue to support sales until at least the spring.

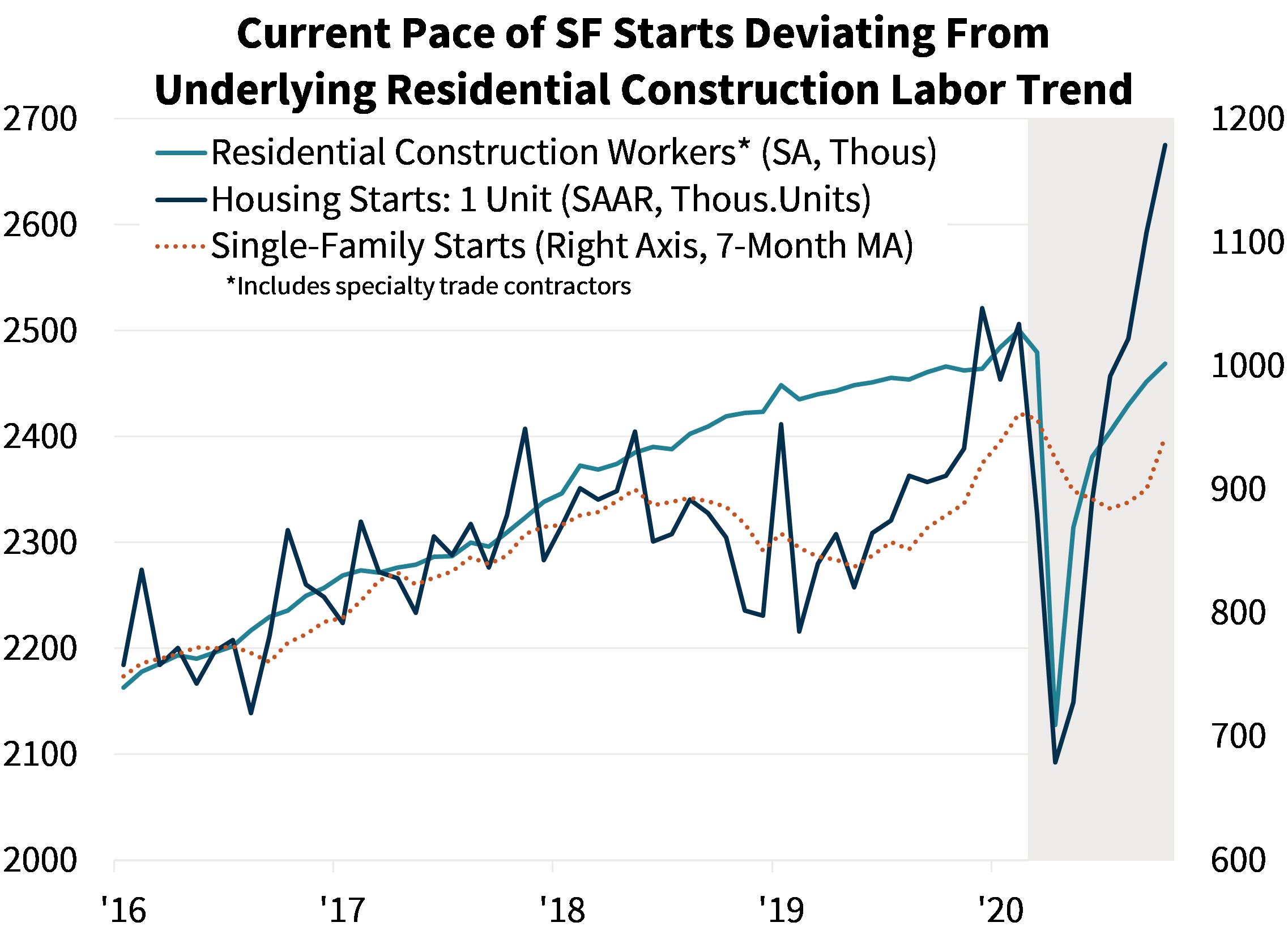

Low inventories of existing homes and increased buyer demand for more suburban and exurban locations continues to support new home construction. Single-family housing starts rose for the sixth time in October, up 6.4 percent to 1.18 million annualized units, the highest rate since 2007. Home sales have eclipsed their usual relationship to starts, so there is an abnormally high share of homes sold that have not yet been started. This probably means the current pace of new home sales is not sustainable, even as home construction remains strong.

That construction, however, may be reaching capacity constraints. For a decade, the seven-month rolling average of single-family starts, (seven months being the time it takes to build the average home) has correlated with residential construction employment. Employment, which represents builder capacity, has increased only modestly in recent months compared to the pace of starts which suggests starts will need to pull back to a more sustainable level until employment catches up.

Multifamily housing starts were flat in October, at 351,000 and Fannie Mae expects the sector to be weaker than single-family construction for the foreseeable future. Suburban multifamily demand is expected to hold up better, but the shift of some renters out of large metro areas and into homeownership, combined with continued remote working arrangements, will likely weaken demand for new projects in many areas.

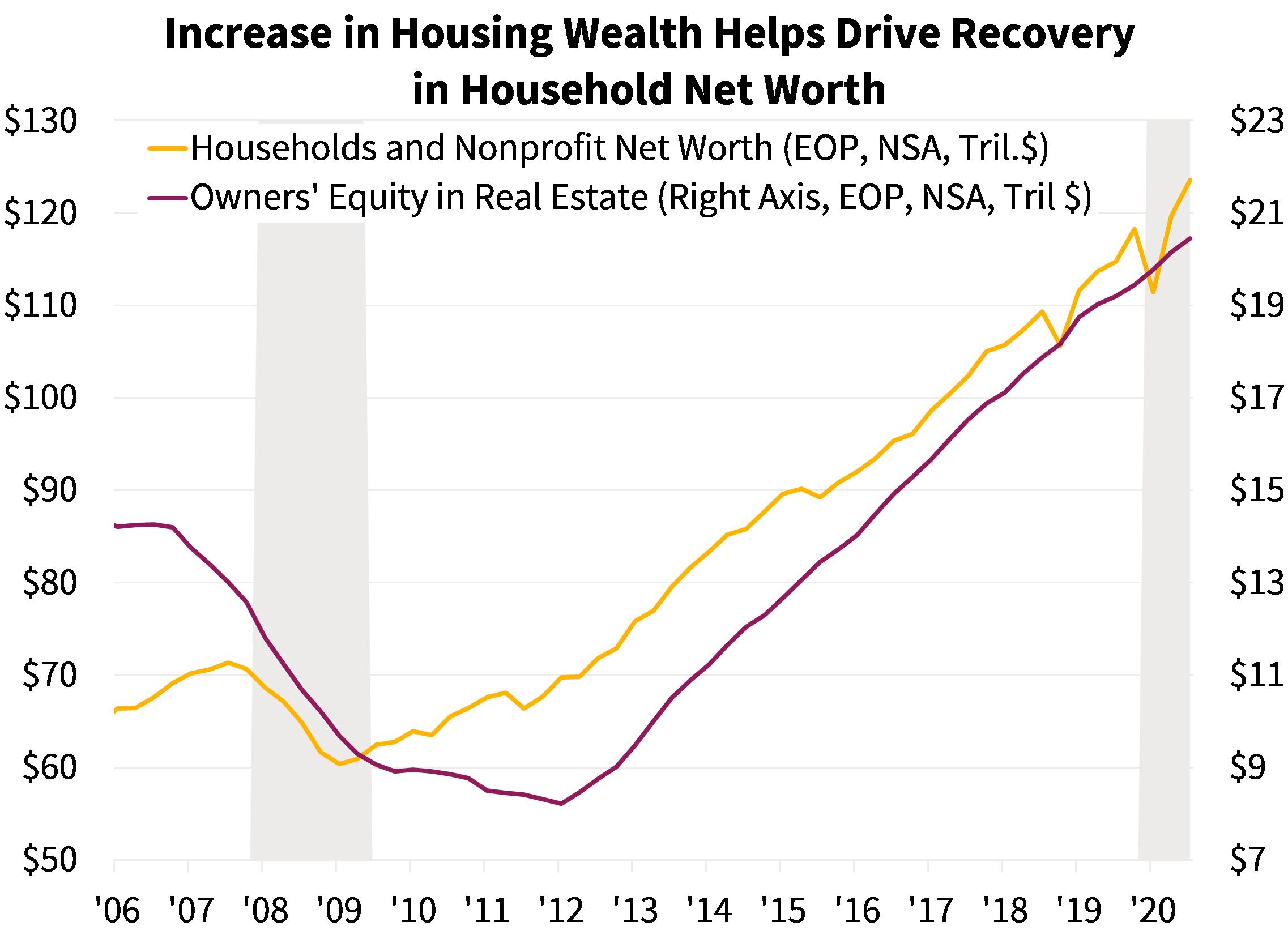

The financial system appears to be in much better shape than it was following the 2008 recession and the strong housing sector, an element missing back then, is helping lead the recovery. The recoveries from the prior three recessions all included a substantial period of an increased savings rate as households tried to repair their balance sheets after asset bubbles deflated and those savings dragged on recovery. In those recessions without asset bubbles, saving tended to decline more quickly and recoveries were brisker. Fannie Mae things the latter will be the dynamic this time.

Since February, households have saved an aggregate of about $1.6 trillion more than at the pre-COVID rate. This, combined with rising equity and home prices, has led to a substantial increase in household net wealth. At the end of Q3 2020, net wealth was 4.4 percent higher than in the same quarter in 2019, a stark contrast to the downturn of 15.4 percent in the Great Recession. This provides a large amount of consumer spending power that was not present back then.

There are, of course, downside risks to all of the forecasts. Will vaccine distribution be fast and efficient and acceptance adequate? Might the vaccine create overconfidence and riskier behavior that results in additional infection waves and lockdowns? It is unknown to what extent permanent structural damage has occurred to business sectors and geographies, and if debt defaults and bankruptcies will drag the economy down. If growth does begin to accelerate, so might inflationary expectations, causing a significant jump in longer-term interest rates. This could quickly dampen the housing and other sectors of the economy that have benefited from the current low-rate environment.

Fannie Mae has also upgraded its forecast for mortgage originations. Its purchase mortgage predictions, it says, are in line with the upgraded outlook for housing, as well as continued recent strength in incoming acquisition and securitization data. Purchase volumes are now expected to total $1.6 trillion in 2020, about $26 billion higher than last month's forecast. Those volumes will grow another 7 percent to nearly $1.7 trillion in 2021, an upgrade of $68 billion from the November forecast.

Refinance originations are expected to reach $2.7 trillion this year, a $142 billion increase from last month's forecast and surpassing the historical peak in 2003. This momentum is expected to continue through 2021, given the continued low-rate environment and Fannie Mae's estimate that nearly 70 percent of outstanding mortgage balances have at least a half-percentage point incentive to refinance. The volume for 2021 refinances was revised upward significantly to $1.8 trillion, although that represents a decline from 2020's peak.

Total originations are now projected at $4.29 trillion this year, an upward revision of $169 billion. The 2021 forecast has been raised by $745 billion to $3.47 trillion. For 2022 total originations are forecast at $2.84 trillion.