Black Knight, (which has just rebranded itself, dropping "Financial Services from its name), has released an especially meaty Mortgage Monitor for December. Of particular interest following the weekend in which the Senate passed its tax reduction bill on a totally partisan basis, is Black Knight's assessment of the potential impact of the House and the Senate's versions on the mortgage and housing markets.

A couple of caveats here. First, while the version passed by the House has had a couple of weeks to age and for analysts for look at its potential impacts, the Senate's bill was literally hand written and few people seem sure (to the extent of even being able to decipher some of the handwriting) exactly what is in the bill. Clearly at odds are the various tax brackets and the taxes that will apply to them as well as last-minute inclusions meant to sway some reluctant senators to cast positive votes. Second, regardless of what is in each bill, they will have to be reconciled to be identical before the bill can be re-voted and sent to the White House. In other words, it's impossible to say exactly what the impact will be until we know exactly what the final bill looks like.

The company adds a further caution. "We've observed in the past that positive tax incentives can certainly impact home buying decisions - the Black Knight Home Price Index (HPI) showed clear evidence of this as a result of 2008's first-time homebuyer tax credit. However, limited data is available to examine the effects of removing an existing tax incentive on borrowers' purchase behavior."

That said, Black Knight has the following concerns about the legislation at the time its analysis was written.

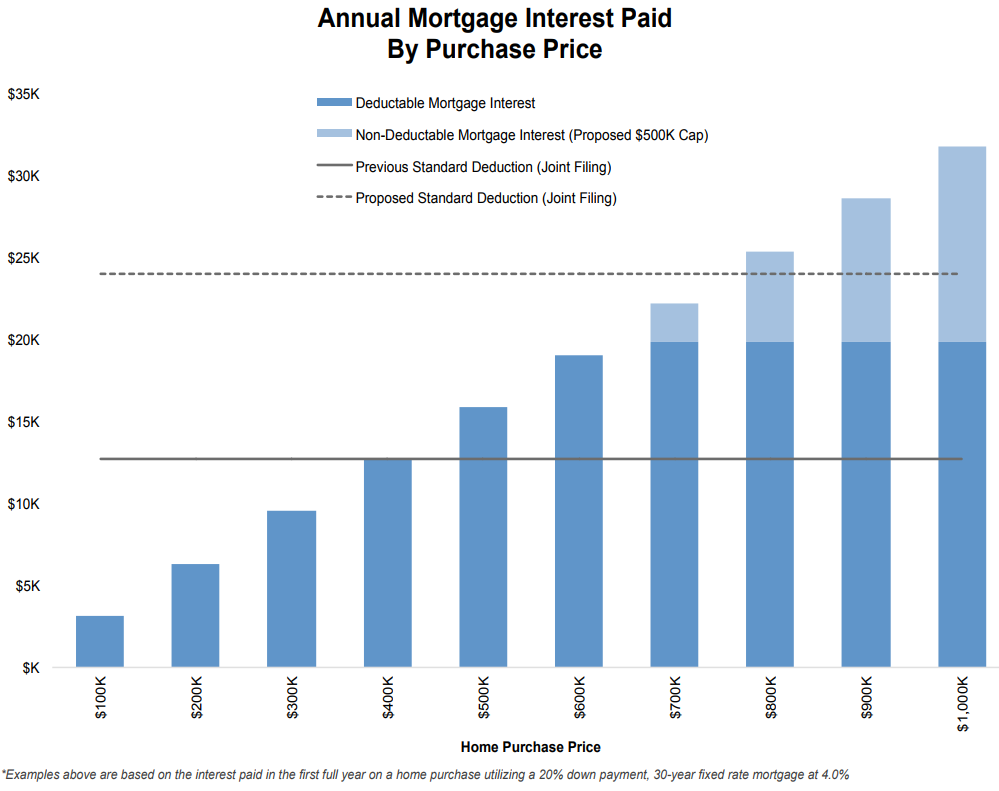

The House's legislation would both cap the mortgage interest deduction (MID) to annual interest paid on a $500 home (the current cap is $1 million), while both House and Senate would double the standard deduction for payers who do not itemize to 12,000 for a single payer and 24,000 for those filing jointly. Black Knight says that under current policy the interest payment on a $400,000 home by itself exceeds the standard deduction even without deducting property tax, medical expenses, or any other deductions to which the payer is entitled.

Under the proposed rule and with the $500,000 cap in place, the mortgage interest alone does not surpass the MID regardless of purchase price in today's interest rate environment. Homeowners who currently itemize, but will no longer do so because of the larger standard deduction, will receive a lesser net benefit than a similar renting family.

This, the company says, will have impacts in moderate and high-priced markets where the MID was previously heavily utilized, and will produce a net result of a reduced tax incentive to purchase a home and an overall devaluation of the MID. This could lead to a decision by some buyers to rent or buy a less expensive home, although the reverse could happen in slightly in higher priced areas if interest rates rise, pushing the MID above the standard deduction. But only if the cap remains at $1 million.

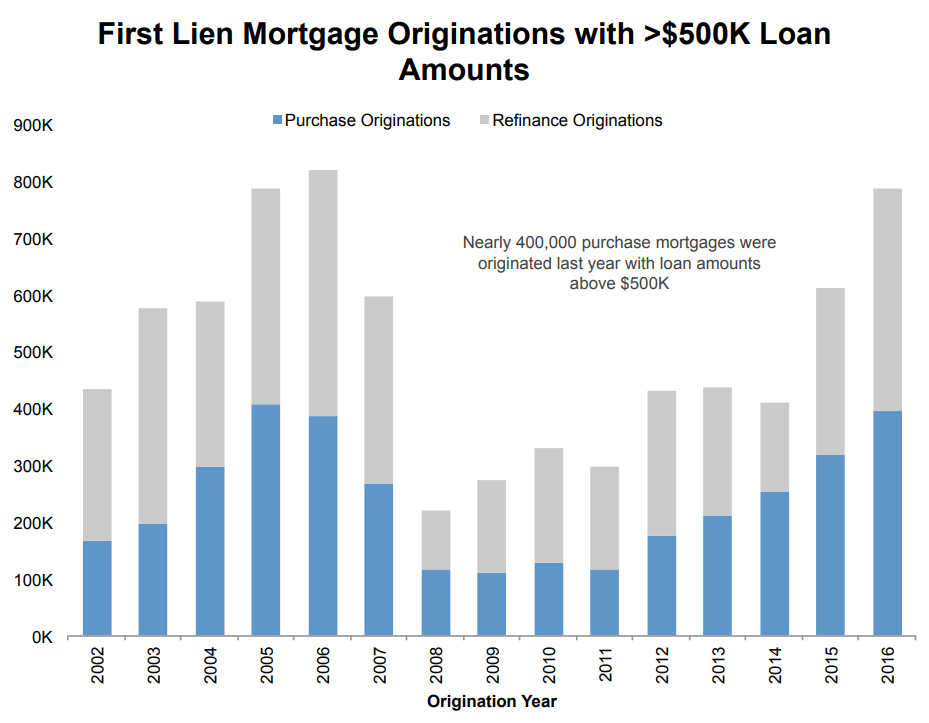

At present, 5.7 percent of outstanding first mortgages, 2.9 million in total, have original loan amounts (OLA) that exceed $500,000 and those homeowners are grandfathered into the $1 million cap even if the reduced House cap becomes law. This, according to Ben Graboske, Executive Vice President of Black Knight Data and Analytics, could be a disincentive for current homeowners to sell and give up their larger deduction.

Graboske says there are indicators that the market has already been constrained by "interest rate lock," that is homeowners with very low-rate loans not putting their homes on the market. He asks if the new regulations would add a "tax deduction lock" into the equation. If so, he says, new supply constraints will likely follow. He adds, "And we know that tight inventory has played a large role in driving home prices up (and up and up) to new peaks."

Referring to the May edition of its Monitor, Black Knight points out that housing turnover has become the primary driver of prepayment activity, and if the disincentive to sell is realized, it could impact prepayment activity on mortgages with OLA over $500,000. Portfolio loans would see the greatest impact, as one in five active portfolio loans has that level of balances, and loans held in private label securities would also be more heavily affected than the average. It is unclear how refinances, especially those with cash-out, would be handled under the new tax rule, but there could also be an impact on prepayment speeds from that direction.

The fact that lower-priced markets may see little impact from these changes (except in high-dollar neighborhoods, perhaps) may make some think this is a problem for the "rich." Graboske points out however, that Black Knight's HPI identifies 22 markets with median home prices above $500,000 and loan originations at or above that level have increased 350 percent since the bottom of the housing market. With annual home price gains continuing at a steady clip, the annual increase has been around 6.0 percent for the last six months, there could be about 480,000 new loans with OLAs above $500,000 next year and some 2.9 million in the first five years and 7.6 million over the ten years of the plan.

Even if interest rates stay at 4 percent, which Black Knight calls an unlikely scenario in the long term, the cap would cost the average homeowner with a mortgage larger than $500,000 an additional $2,600 to $4,200 per year, depending on their tax bracket. That is a 6 to 10 percent increase in net housing costs.

An additional feature of both the House and Senate versions, and one which has gathered little attention during the discussions, are new limits on the capital gains exemption on the sale of a home. The current tax code allows homeowners to exclude the first $250,000 ($500,000 for joint filers) from capital gains taxes if the home has been owner occupied during two of the five years preceding the sale. It is proposed that exemption will require continuous occupancy for a five-year period.

Black Knight says more than 15 percent of home sales over the past 24 months were by homeowners falling into that 2-5-year window, and who would no longer be exempt from capital gains taxation. The company estimates the proposed changes would affect approximately 750,000 home sellers per year under existing sales volumes. "That works out to about $60 billion in capital gains, with a worst-case scenario (taxing the full amount under the highest tax bracket) putting the cost to home sellers at approximately $23 billion."

"If these homeowners choose to forego or delay selling to avoid a tax liability...guess what? Even further tightening of housing inventory," the Monitor says.

The two branches of Congress are expected to begin conference proceedings to reconcile the two versions of the GOP tax proposal. Some legislators expect it to be on the President's desk by the end of this week.

The new edition of the Mortgage Monitor also provides additional information on rising delinquencies from the two hurricanes that hit the mainland in late summer and the first regarding the delinquency situation in Puerto Rico. We will briefly touch on this data in a separate article.